Learning How to Effectively Use Praise and Criticism is the Primary Task of a Manager: We need praise, because it inspires us to do better. You do not want to criticize for something you did or didn’t do. We often do not like criticism. No one wins friends without praise. Using both praise and criticism is the most effective. You should praise the small, and large, never miss an opportunity, and remember people’s names. Nothing is sweeter to another person, than to hear their own name. You should always acknowledge an idea, then provide counter-examples.

Learning How to Effectively Use Praise and Criticism is the Primary Task of a Manager: We need praise, because it inspires us to do better. You do not want to criticize for something you did or didn’t do. We often do not like criticism. No one wins friends without praise. Using both praise and criticism is the most effective. You should praise the small, and large, never miss an opportunity, and remember people’s names. Nothing is sweeter to another person, than to hear their own name. You should always acknowledge an idea, then provide counter-examples.

PRAISE the person, CRITICISE the category: your should be quick to praise, an individual banker, but you should blame the banker indirectly.

How To Win An Argument: To win an argument, you sometimes have to lose. The best way to argue is to ensure that the others do not lose face. It is better to agree with someone, and then have that person listen to your ideas. You need to reduce conflict. Benjamin Franklin’s business and life philosophy is powerful. You should avoid arguments. You should not use words that are certain, but do not contradict them abruptly. You should modestly position your views. Avoiding arguments is a way of accepting other people’s opinions.

Henry Ford said that if there is one secret of success it is to see things from other people’s position. You should seek out what people want. Connect their wants with your goals.

Encourage Others To Come Up with the Right Idea: Warren likes to set their own goals and standards, employees will set the standards higher. Warren’s silence, drives their performance. No one likes to be ordered about. If it is your own idea, then you will act on something with conviction. Instead of saying “don’t swim in the lake” you should illustrate the matter “If you swim in the lake, you will be eaten by a shark.” You should ask what your subordinates want from you. Then ask what you would expect from them.

Encourage Others To Come Up with the Right Idea: Warren likes to set their own goals and standards, employees will set the standards higher. Warren’s silence, drives their performance. No one likes to be ordered about. If it is your own idea, then you will act on something with conviction. Instead of saying “don’t swim in the lake” you should illustrate the matter “If you swim in the lake, you will be eaten by a shark.” You should ask what your subordinates want from you. Then ask what you would expect from them.

Ask Questions Instead of Direct Orders: asking questions makes you more palatable. It’s better to let people figure something out themselves. Warren Buffet peppers his managers with tough questions, they are direct orders that have been masked.

“This is not the way to do it.” versus “Is there a better way to do that?”

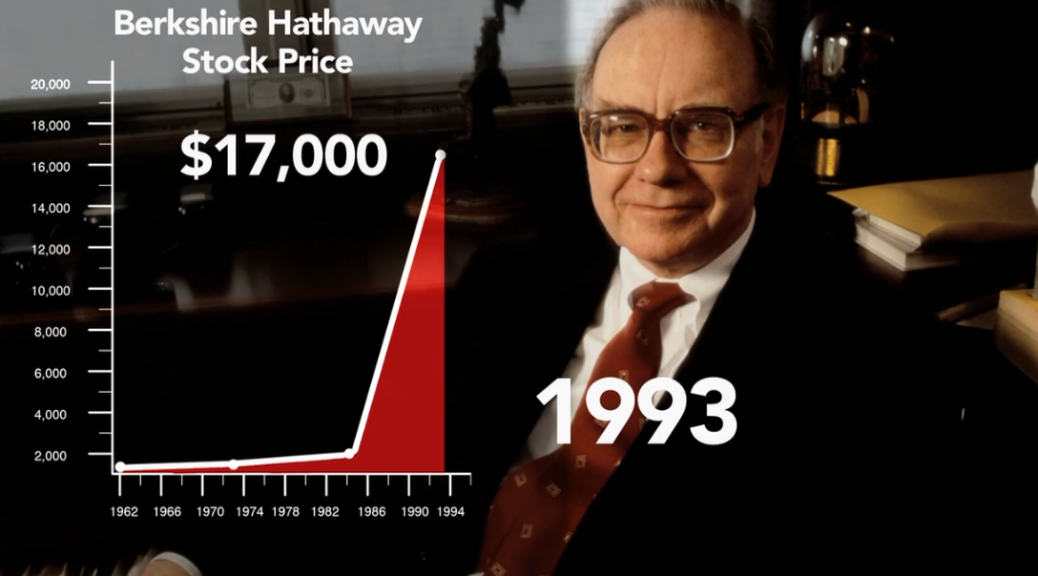

When you are wrong you should admit it: no one can stand someone who won’t admit that they are wrong. Managers who don’t admit that they are wrong which causes a festering. Warren is upfront about mistakes made. People respect honesty. Warren wins the trust of his shareholders.