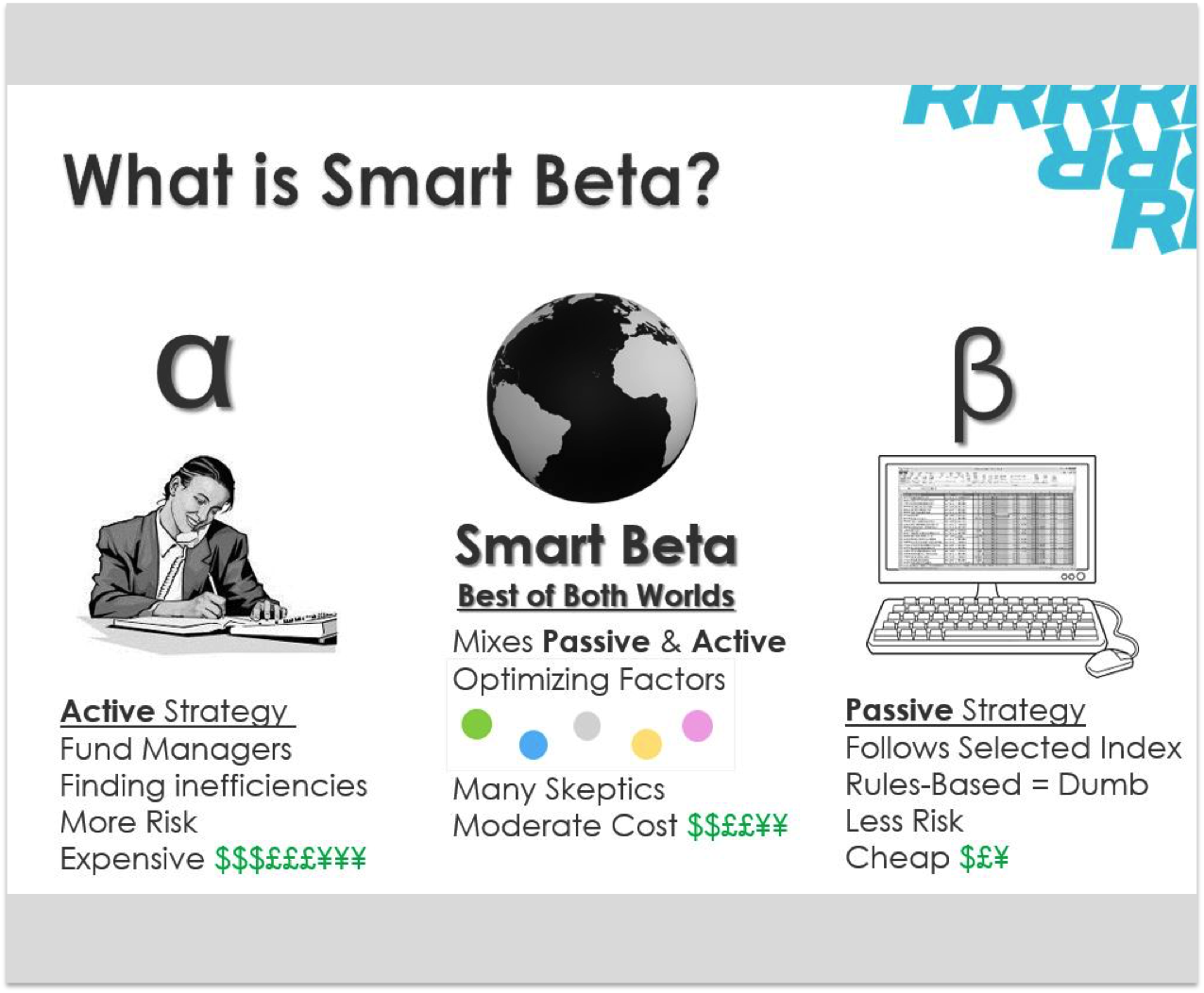

Matt: What is smart beta? Well, a really simple answer is it’s a combination of alpha and beta. It’s a combination of active strategy and passive strategy. What does that actually mean? Let’s boil it down a bit further. You’ve got, on the alpha side, alpha chasers who are fund managers. They’re trying to find that market inefficiency… They allow the risk. And they’re quite expensive. On the other side you’ve got this more automated approach with beta. It’s a computerized model that follows a selected set of index stocks. And you, your stock selections, move alongside the market.

So, overall, in the long run you’ll benefit as the market improves. You’ll get a modest return but you’ll definitely get a return. So the thing about that is it’s definitely less risk and it’s cheap, excellent. But it’s pretty dumb in the sense that it focuses and overweighs large-cap stocks, the large companies, and undervalues the critical small-cap opportunities that someone like the alpha would…the alpha investor would highlight.

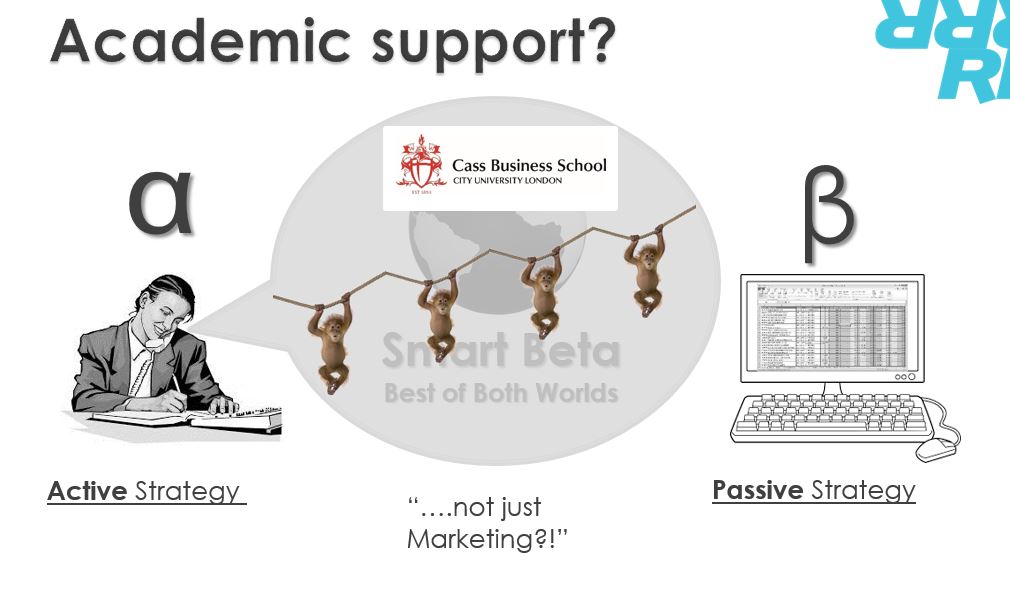

So why don’t we combine the two and find some kind of happy medium here? And that’s what smart beta is. It’s the best of both worlds. It mixes passive and active at some ratio. And it’s really about optimizing the beta factors. Of course, there’s many skeptics, however, and the really great benefit is obviously its moderate cost.

So moving on now, we’ll talk a little bit more in depth regarding smart beta.

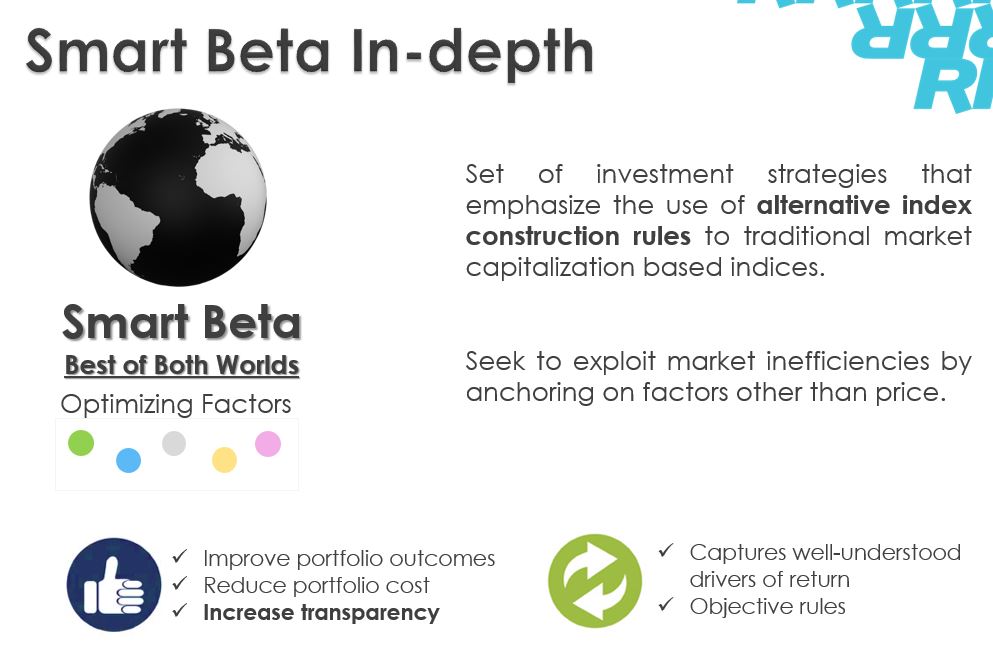

Juliana: So smart beta is a rule-based portfolio process. The idea is it’s a set of investment strategies that emphasize the use of alternative construction rules rather to the traditional. The smart beta expert says that the market is not always efficient so sometimes the prices show a what is going on in the market. So the idea is to find new factors to analyze and to make better decisions about the stocks that you want to invest and how much to invest.

So the idea is to seek and exploit market inefficiencies and by anchoring on factors other than price. That’s the idea, look for factors than price. So some of the benefits that a smart beta [inaudible 00:02:40] say that this thing have, for example, improved portfolio outcomes, reduced portfolio costs because it’s in the middle of the active and passive management, increased transparency because the rules are [inaudible 00:02:54]. You can’t change the rules or the factors in the middle of something. At the beginning, you know the factors that you are gonna use and then [inaudible 00:03:07] rules and factors [inaudible 00:03:09].

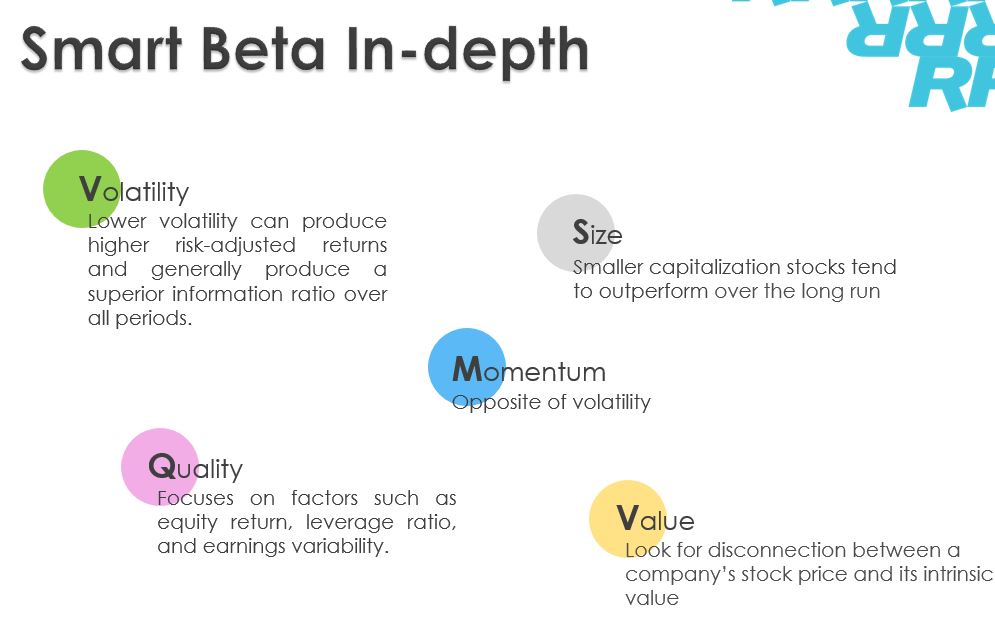

Some of the factors [inaudible 00:03:14] single ones are those. For example, value and quality are pretty interesting. For example, quality focus on factors such as [inaudible 00:03:24] ratio [inaudible 00:03:26] and this factor is one of the innovations of smart beta because, as you see, introduce maybe some things created with the quality of the balance sheets of the company. This is something different than the traditional investment. And also the value [inaudible 00:03:44] the disconnection between company stock price and its intrinsic value, something that we try to do in our class, so this is one of the factors that you can use.

Some of the factors [inaudible 00:03:14] single ones are those. For example, value and quality are pretty interesting. For example, quality focus on factors such as [inaudible 00:03:24] ratio [inaudible 00:03:26] and this factor is one of the innovations of smart beta because, as you see, introduce maybe some things created with the quality of the balance sheets of the company. This is something different than the traditional investment. And also the value [inaudible 00:03:44] the disconnection between company stock price and its intrinsic value, something that we try to do in our class, so this is one of the factors that you can use.

To understand better what smart beta is, it’s important to go to the roots of smart beta. It’s actually the factor investments concept, an old concept up to 1960. And the idea of the concept is to define the factors that drive [inaudible 00:04:14]. And to explain to you a better way, we just have here an example. Nutrients are for food what the factors are for the assets. So if you are a healthy person, you want to choose the nutrients that are better for your health. So you analyze not only the kind of food, for example, I don’t know what, fish? You analyze also the kind of nutrients that a fish can give you, to your health. It’s the same thing for factors, and the idea is that factors are fundamentally the building blocks of the investment [inaudible 00:01:48] and you can be sure the factors that you are going to use.

So Devon will tell you about some of the strategies about smart beta.

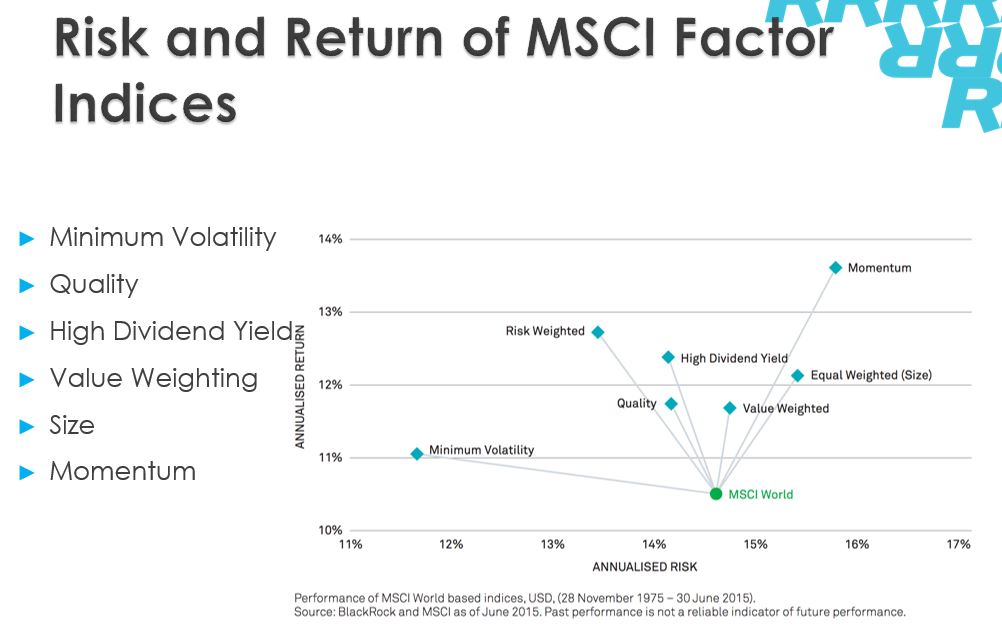

Devon: So investors are able to choose which factors they want to invest in. One of the ways that they might choose between certain factors is to look at the risk and return of factors. So MSCI is a [inaudible 00:05:16] fixing common hedge fund stock market index provider. And these are some of the factor indexes that they provide. So as you’d expect, the minimum volatility factor delivers the lowest annualized risk, and we can also see that the momentum factor delivers the highest risk but also the highest return. So another characteristic that investors might look for is past performance of factors. So although factor returns are highly cyclical, there typically have been trends in how they perform in the past.

So, typically, value, momentum and size factors have outperformed in strong macroeconomic environments, while high-dividend, quality, and minimum-volatility factors have outperformed in weak macroeconomic environments. So one specific strategy that I came across when I was researching this is a strategy dubbed “betting against beta.” So according to the CAPM, risk and return are related to beta and supposedly the higher beta you have, the higher return you will have. Although we’ve learned that there’s weak empirical evidence to support this theory, and, in fact, high-beta portfolios do not perform any better than low-beta portfolios, as you can see from my slide. The relationship between beta and returns is actually relatively flat. So this is one of the inefficiencies of the CAPM.

So AQR is a hedge fund, a large hedge fund, that employs the “betting against beta” strategy. And they seek to take advantage of other inefficiencies with the CAPM model. So their basic strategy is…one of the basic strategies is to short-sell stocks with a high beta and to buy stocks or take a long-position stock with a low beta. So their reasoning is that because institutional investors and because individuals are constrained in the amount of leverage they can take, which means they have to resort to other means to get high levels of return on their investments, what they…what there’s a tendency to do is they’ll invest in high-beta stocks in order to increase their potential return. And this leads to an overweight in high-beta stocks. So to take advantage of this…or what this means for AQR, if they’re correct, is that high-beta assets will be overpriced and low-beta assets will be underpriced. And so that’s why they short-sell the high-betas and buy stocks with a low beta. So we will talk about how other big players use factors to invest.

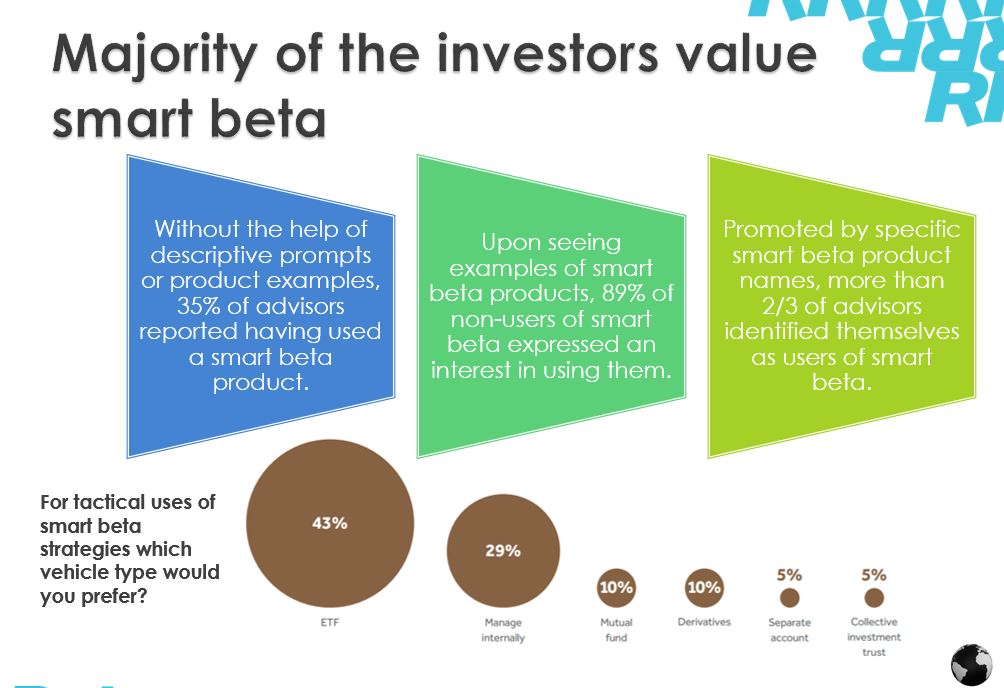

Leah: So smart beta products are becoming very popular for investors. And about 89% of the nine [SP] users have expressed interest of using them in the near future, and then 35% of the investors are actually using them in their investment. Smart beta has been most frequently implemented in the ETF, and then the next most frequent use is in internal risk or control and [inaudible 00:08:28]. So because technically anybody can use smart beta, but then because of the complexity of populating it, the investors who have been using smart beta in their investments are mostly from the top investment firms such as the Black Rock and Vanguard, and the…thank [SP] you, the company that we just mentioned earlier.

And then the rest of the investors, they either choose to consider or value the smart beta but not necessarily use it, or the other just show a strong interest in wanting to learn and educate before they actually use it. And then according to a survey that was done by T.S. Russell, [inaudible 00:09:15] about 40%, 42% of the investors actually don’t use smart beta because they don’t feel that they know enough about it. And then the next 35% of people actually think that they don’t use it because there’s not enough historical data or any record for them to analyze.

And then Uday will talk about the growth in smart beta strategies.

Uday: So to analyze the growth in smart beta strategies, we look at the amount of investments that are coming into smart beta assets. So just some quick facts: the number of smart beta global providers grew from 54 in 2012 to 92 in 2015. So that’s approximately a 70% drive in growth [inaudible 00:10:02]. Also, 112 of all the investments coming to assets have been through smart beta strategies. So, [inaudible 00:10:09] the demand that’s coming in but let’s see like how that goes.

So this is a breakdown of all the smart beta assets based on the different type of factors. So as you can see, the minimum qualitative [SP] factor that has had the highest annual asset growth [inaudible 00:10:28] at 21%. But as for all the other type of factors, it has an average of 40%. That’s [inaudible 00:10:35] volatility in the market. The markets are… They’re gonna be more volatile, and then people expecting to invest in something that is more safe and less volatile, that is more predictable. So a detail into this, based on the countries, we did an analysis of U.S. versus Canada. So if we look at the minimum volatility factor, then Canada made a lot of investment into minimum volatility smart beta portfolios as compared to the U.S. so that’s, again, representative [SP] of the risk-averse nature of the Canadian investments.

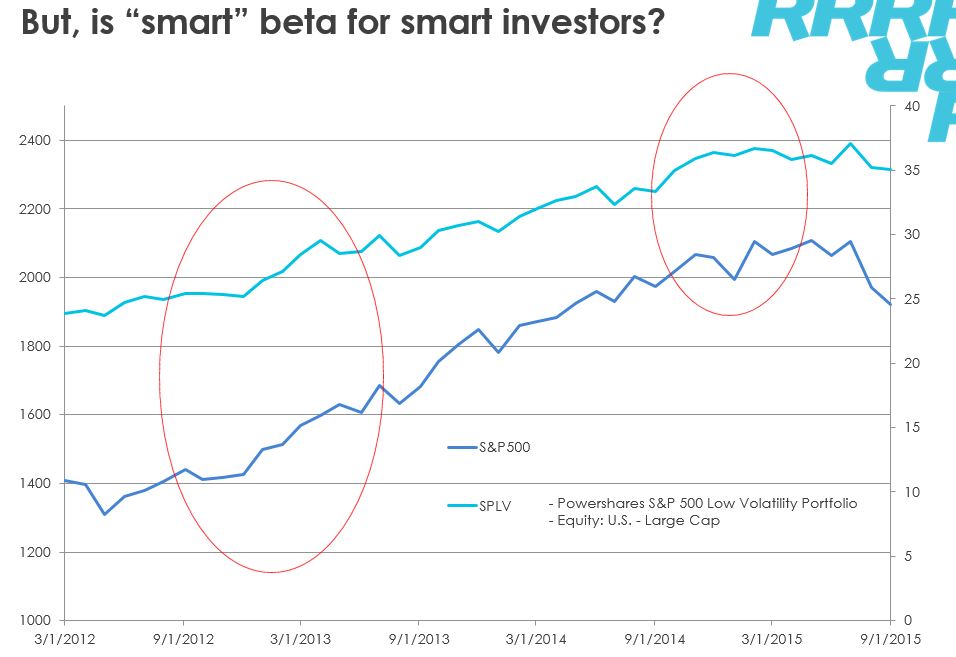

But the question that we need to ask is, is smart beta really smart? Should a smart investor be investing in the smart beta portfolios? So we did a small analysis based on an S&P 500 low-volatility portfolio and we compared it against S&P 500. So these two regions, I mean, if you look at it overall, it appears to be moving in the same way. But these are the two reasons where it sort of differed. The second reason here is basically went… So the lower end is the S&P 500. The upper line is the portfolio that we chose.

So, you can see, in the second reason when S&P 500 dipped, that is the point when this minimum-volatility portfolio… It stayed constant or slightly increased. That is where you gain. But the flip side is, the first part, when S&P 500 grew at a larger rate, then to this minimum-volatility portfolio, it stayed constant, right? So it’s like you’re gaining at one point and then losing at the other. So this is what we think about it. The S&P 500, it’s an average of all the factors. And we are then focused on just one factor. And we will in the long run. So how smart is it?

So these are certain concerns that became [inaudible 00:12:33]. It might represent a false alpha [inaudible 00:12:37] it’s a new thing that has come up. So it might have the newbie advantage. Then you can have [inaudible 00:12:43].

Man 1: So where does that leave us? What do we do with this now, basically? The alpha fund manager will come to you and pitch the idea that, “I alone will beat the market. I’ll achieve market… I’ll find market inefficiencies.” But in the real world of 2008 and other instances, it doesn’t quite work out for that fund manager. And so the investors then shift their energies and idea of their money over to the passive strategy because they’re cheaper and they basically get similar outcomes in that case. So enthusiasm shifts over to the passive beta side. But they, as the fund manager, of course, they’re in the business of making money, so they want you to come back. Why? “You know, we didn’t beat the market, but still I want to help you out. Why not try something called smart beta?”

And we’ll have some data as we have shown as well, the Guggenheim 2003 smart beta portfolio strategy. It’s produced 11.5% per year, whereas the cap-weighted got 8.4%. “So, clearly,” he would say, or she, “This is a great opportunity for you. You should get into smart beta.” And even on the academic level, Cass Business School says that this can work. They did a study. They got 10,000 monkeys… No. They got 10,000 portfolio stocks and basically took that, randomly selecting them, and applied a smart beta formula to that set of stocks for those separate incidents [SP], those separate fund managers, as it were, and the outcome was that it did perform…outperform the cap-weighted average. So it clearly works.

So, in conclusion, there is a lot of debate. And I don’t think it works, in my opinion. We’ve got a little bit of a debate on it. But in essence, there’s a lot of people who have an opinion about this. The President-elect of the United States actually tweeted about this. So a couple nights ago, in fact, at about 4:00 a.m., Donald Trump tweeted this: “Smart beta is for dummies, big league, like that totally failed former host of “The View,” Rosie O’Donnell. Failed investor. Sad. #dumbbeta.”

And, Rosie O’Donnell, she was up at four in the morning as well, and she followed up with this response: “Wow, actual President-elect is at it again, this time criticizing my investment strategy. Smart beta works for me. I hate fund managers, almost as much as talking pumpkins. Get real, Donald Trump.” So there’s a lot of debate. There’s a lot of anger around this issue and we’ll leave it for questions.

Instructor: Questions.

Questioner 1: So, if I understood this correctly, [inaudible 00:15:55] right [inaudible 00:16:03] in the beginning?

Devon: Yeah, you look at the factors to inform your investments.

Questioner 1: The second part of [inaudible 00:16:09] actively readjust your portfolio based on the [inaudible 00:16:14] or changes in these funds.

Devon: So, I believe… The way I understand that is there’s different ways to implement the strategy. One way, what you have to do is when you purchase these factors, they’re gonna change over time, so I think there will be readjustments if necessary.

Questioner 1: So my question actually is how is it any different from active investing?

Devon: Well, with active investing, you have people that are doing research into these…into different investments or different stocks because, as I see it, with smart beta, I don’t think it involves the same level of research. I think that the rebalancing is like it doesn’t… I don’t think it involves the same level of effort and output and research as the active stock-picking does.

Uday: And so, just the way how you pick stocks, so in that active stock model [SP] you’re just like picking up stocks that you think are performing well, right? In smart beta, what we’re trying to do is, we’re trying to actually put factors in each of those stocks and see what factors weighs most in each of those stocks. And then we want to choose factors. So we pick stocks based on those factors. So it’s like, if I want a minimum-volatility, right, I would not look at the total breakdown [SP], but I would look at the stock that represents minimum-volatility because I believe that that is the factor that will get me highest return in the long run. That’s… I guess that’s one of the other differences in addition to what he just said.

Questioner 2: I understand how it works now. But, for example, is there a way for you to [inaudible 00:17:50] how relevant each factor should be? Or is it completely subjective?

Devon: So I think the idea behind factors, especially the size factor and the value factor, is they arise because of economic anomalies or behavioral differences. And it’s not always understood, like I don’t think it’s really understood why size and value give the different returns that they do. I think that’s the case for the other [inaudible 00:18:19] quality, and, like volatility. I don’t really… I don’t know if it’s completely understood why they act the way they do. But, historically, they have performed consistently, and I think that that is one of the criteria for these factors, is it has to be historical. It has to be robust, and it has to be consistent, like the size and value factors.

Instructor: All right, thank you guys.