Your first idea for how 2 fix a writers block is rarely ever the best. Think about how you can engineer your story to maximize the fun…

You have to find the piece of the story that we can connect with. Drinking stories and vacation stories are not good because they are a series of ANDs…I did this and this….us But & Therefore, Cause/Effect.

Your story should be tell-able at a dinner party: KISS = keep it simple, smartie-pants.

You should practice telling your canned stories at said dinner party. But never in front of a mirror that’s not how you’ll tell it in the wild.

Rule #2: Harvest the Mundane & Audiences will Connect

People want to engage by seeing themselves in that story. Just say no to jumping out of an airplane, epic adventure and say yes to arguing with your spouse about the dishwasher! Make your story little.

Create a spreadsheet called the Homework4Life™: column 1: date, column 2: write a snippet about the most eventful part of your day.

Write down snippets from your live memories when they pop into your mind so that you can harvest later.

Self-discovery requires the reflection habit to form which means taking 15 minutes a day. It takes time to hone in on your stories. §Harvest in your daily life and you will find other memories.

Rule #3: Homework4Life™ Is Better Than Anything

Use stream of consciousness to populate your Homework4Life™ spreadsheet on a daily.

Forget what the education system has taught you: ie. to have a main message (thesis) and your arguments to back that thesis. This approach is deeply alienating. §Use a pen/keyboard or speech-to-text into your phone so that there are no pauses.

If you have pauses/writers block start listing colours until a new memory is triggered based on association. §Storytellers needs to selfishly guard their time: that means early morning or a locked door.

Rule #4: Unearth Stories with First / Last / Best / Worst

Create a spreadsheet called the First/Last/Best/Worst™:

Scan your memories based on these 4 questions.

What was your first ____? What was your last ______? §What was you best ____? What was your worst _____?

Rule #5: Five Second Moment i.e. Jurassic Park is not a dinosaur movie

The reason you put pen to paper is you had a 5 second moment of profound realization and you think others should know about it.

Profound realization = a moment that changes your life fundamentally

“I love this woman but she wants kids. I hate kids. Then after saving two kids I realize I do like kids. And my sweetheart and I ride into the sunset.” – Dr. Grant from Jurassic Park §Realization should be the polar opposite of the start of the story.

Rule #6: Find Your Beginning (the Opposite of the End)

Your story should end with the five second moment of realization.

Your beginning should start at the extreme opposite: start afraid end fearless, start happy end sad, start uncertain end confident, start hopeful end not, start angry end grateful. The opposite can be good or bad, just make sure it is the opposite of the end to maximize the story.

Every good film starts with the main character moving to the opposite by the end of the story. In other words, the main character has an arch.

Rule #7: Create High Stakes, Why is the Best Question

Why is the best question you can get your audience to ask (engage!)

A) The Elephant: An elephant is the thing that everyone in the room can see: it is the need the want, the problem, the peril the mystery. It signifies where the story is headed.

Elephants can change colour: it can flip to create more surprise.

B) Backpacks: increase the stakes by increasing audience anticipation of what is next because you laid out the plan and now we are watching with you as you execute. Ocean’s 11 has a plan that ratchets up.

C) Breadcrumbs: leave little hints for future events but only enough to keep the audience guessing (engage). Find a breadcrumb that maximizes the number of guesses the audience can make. Of course, the completely unexpected is the most effective story.

D) Hourglasses: take the audience to the brink of the big reveal but then provide insane detail. What is the story teller gonna do next? Please get to the punch line! This is hurting my brain!

E) Crystal balls: audiences want to run ahead often. Here the storyteller creates a false prediction of what is going to happen next. We are programmed prediction machines. Get your audience to engage your story. The storyteller’s prediction is strategic.

Rule #8: Don’t Be A Dufus (public speaking rules)

Do not praise yourself: no one wants this amazing AND awesome person.

Be self deprecating: no one likes a know it all.

Don’t ask rhetorical questions: it derails the cinema of the mind.

Offer one granular bit of unique value, one 5 second moment. A small memorable and useful idea for the graduates: if you’re valedictorians.

Don’t cater any part of your speech to the parents of the graduates.

Make your audience laugh: the comic triple, sarcasm, irony, intentionally miss.

Do not talk about the weather if it’s hot everyone knows it…

Do not be formal in your speech be casual like you’re speaking to a friend.

Be excited, hopeful and enthusiastic: the audience wants a Yes, Ladder.

Don’t describe the world the graduates will be entering because you actually don’t know the world, you only have your perspective on the world even with modest data.

Don’t define terms based on the Webster dictionary: it’s just lame.

Don’t use a quote that you’ve heard someone use in a previous commencement address. You’re goal is to provide new insight that’s why you’re getting this degree.

End your speech in less than the allotted time: brevity is the soul of wit, “If I had more time, I would have written a shorter letter.” – Blaise Pascal

Rule #9: Permissible Lying in Storytelling from Your Life

Lie 1# Omissions: if there was a third person who is not relevant simply don’t distract the reader with their presence since that’s distracting.

Lie 2# Compression: if it took 5 days then compress into in an afternoon if credible. Every film compresses time into a 24 hour story almost always. It creates pace & urgency.

Rule #10 Create the Cinema of the Mind, Visuals

Storytelling must put the audience in a location that they can imagine on their own. Every moment must be situated in a physical location the audience can create in their own mind thus engaging them fully.

Never open a story with a philosophical point, a thesis.

If you need to explain something philosophical, then the audience in the classroom w your teach or judge’s chambers with the lawyers or the stock exchange or where ever that idea can be credibly expected to be discussed. §

Rule #11: Use “But” and “Therefore”

Cause & Effect causes the human brain to release dopamine. §DO NOT CONNECT sentences with the word AND. AND kills.

“But” and “Therefore” are the ligaments of storytelling. §“But” = although, however, nevertheless, still, though, yet, on the other hand.

“Therefore” = so, then, thus, consequently, for, and so, hence, since, to that end, on account of, on the ground.

The story is a chain of cause and effect events…destination is the five second moment of realization.

Rule #12: Surprises Elicit Emotional Responses

Paint a rosie picture of scenic day and then suddenly WAM!

Never present the thesis statement before your surprise.

Never say what this story is actually about, let the audience ride.

Always hide critical information in clutter or innocuous details.

A laugh line is a good spot to hide a key piece of information.

Save the last big laugh for the end. Do not blow the joke early.

The Baby Blender rule is that two things that don’t go together are smashed together, typically humour ensues.

Rule #13: The Present Tense Is King

Part of the Cinema of the Mind is to make it happen right now.

Using the present tense always is very effective for keeping readers in the moment itself. Get your audience to time travel with you to now, this story is happening. Let the audience create the vision of the events as they unfold.

Rule #14: A Hero Must Start the Story the Opposite

Failure is fare more engaging than success from the start.

Marginalize your accomplishments: know you aren’t perfect. Be the underdog in the story. We love underdogs!

Malign yourself: tell the story of a small success.

Rule #15: When Performing

Get your audience to laugh in the first 30 seconds of your story.

Don’t memorize every word of your speech. Instead:

Always start strong: the first few sentences should be memorized.

Always end strong: the last few sentences should be memorized.

Know the scenes of your story: MAXIMUM 7 Scenes to remember, memorize the colour which indicates mood of the scene.

Make eye contact with three people in the audience. One on the left, one on the right and one person in the centre to move back and forth between.

Control your emotions as the moment of intense emotion arrived, change the perspective from your vantage point to 3rd person so that you don’t cry on stage.

“What’s your favourite movie, ice cream, meal?” Instead, use stream of consciousness, free associations, connections based on particular nouns/topics discussed.

Tool 2: Canned Invitations Questions

Q: How are you? A: “I’m swinging in an hammock!” Q: How was your weekend? A: “[describe something funny]” Q: Where’d you go to school? A: “[partying 80% studying 20%]” Q: Where are you from? A: “[the prairie skies…minus 40.]” Q: Do you have siblings? A: “[one sis, two bros..lot-a-sharing]” Q: What do you do? A: “[I help financial traders click better]” Q: What did you study? A: “[people, places and beers]”

Tool 3: Double Answers

Step 1 – provide a layman’s answer that is short, unique and fun. “I pack and send wallets for a living!” “This weekend I sailed my parents sailboat chanting limericks and avoiding siblings.” Step 2 – provide the expert answer. “I’m the CEO of a men’s apparel company.” “Sailing since I was 12, like riding a bike.”

IMPORTANT NOTES

Don’t want to appear too knowledgeable or elitist in Step 2

The Basics Part II

Tool 4: Always Stay Positive

Lead with: “Yes!”, “Agreed!”, “Totally!”, “Awesome!” Avoid: “Nope!”, “Yeah But!”, “Wrong!”, “The opposite!” Compliment things that the person can control: clothing, hairstyle, accessories, world view, their ideas, how they solve/tackle a problem, weight loss….. Do not compliment eyes, ears, face, body as the person cannot really control those things, (also inappropriate). Flattery can quickly become ham fisted and lame, avoid it.

Tool 5: Pay Attention to how they want to be perceived

Call out when some one has put in a lot of effort. “You kept working on that project, we love it!”

SUMMARY OF THE BASICS

Don’t use absolutes, use generalizations…no right answers.

Reactions are important, mirror the emotions that the other person is expressing, this brings them onside.

Use free associations in the conversation; keywords!

Double answer: layman answer and expert answer.

Give people complements on the things they control.

Witty Banter Part I

Tool 1: Don’t Be Too Literal

So the idea here is to be more playful in your conversation, less literal and less serious. Use conversation as a way to have fun with people rather than share information or facts.

Something that is noteworthy and gets their attention is more valuable than a straightforward answer, in most circumstances.

Make sure you actually answer the question so that you’re humorous and informative.

Tool 2: Witty Comeback

When you come back should be done with an indifferent tone, in the way that perhaps James Bond might use, after just defeating a villain. “Positively shocking!”

Focus on specific words that the person uses. And exploit those words. Re-interpret them in a new way. Intentionally mis-interpret their statements.

For example, Statement: you’re as slow as a glacier….could be interpreted as. Comeback: you mean I’m strong and cool under pressure?

Tool 3: Amplify the Statement to a ridiculous degree

“You look like a girl” Can be responded with “Am I a charming girl?”

Witty Banter Part II

Tool 3: Banter Chain

The key is to stop taking things at face value and start intentionally misinterpreting the statement for goofy results.

The best way to break the mold in small talk is to play dumb and misconstrue what the other person’s point was.

You can achieve quite a lot in your banter by agreeing and then going beyond and amplifying what they had said to create a banter chain. For example, Statement: I love the colour of that cat. Reply: “so you think that cat is sexy huh?” Answer: “Yeah, I think that cat sexy I can go on a date with that cat.” Question: “where would you take the cat?” Answer: “I’d take that cat dancing all night, cats are nocturnal after all.”

Tool 4: Exaggeration Is an Effective Technique

For example if you say I’m really hungry I could eat this whole meal myself, the other person could reply oh I could eat a horse;

Make sure the exaggeration is extreme: “I’ll call you when you get home.” A: “Well, I don’t know how I don’t know if they have phones on the moon….”

Play In Conversation Part I

Tool 1: Break the Fourth Wall

Commenting on the conversation itself.

Acknowledge something about the conversation. Full meta!

“This conversation just took a fun turn…”

“I apologize for talking so much about this topic…”

Be positive: “Franky, I don’t know where this conversation is going but I like it!”

Us against the World: “Have you noticed something…?”

Tool 2: Fall Back Stories

Fall back stories should be universal. Never use absolutes…..

Four distinct parts

The bridging sentence “You know what I heard yesterday…”

The story “One of my friends proposed to her boyfriend, didn’t want to wait…”

Your opinion of the story “I thought, well, it’s 2021…”

What their opinion of the story “Would you accept a proposal like that?”

Just transition from a dead convo: “Want to know something interesting that happened yesterday?” or “You won’t believe what happened?”

Story points out some basic emotions, story telling. It’s not even about the story…what is the primary emotion and point!!!

My opinion: “You want to have a positive interpretation.” It’s key to be positive…

Opinion: “Would I do that?” You need multiple questions to prime the conversation.

Play In Conversation Part II

Tool 3: Role Play

Get the creative mind flowing, how would you proceed with this story?

Make a judgement about someone, that contrasts with you. “You are great at navigating”

Give them a label in a statement made. “Chris Columbus of Round Lake.”

Start playing the role: the modern Chris Columbus. Then you play out the role conversationally.

Then continue with the fake set of questions…Chris Columbus would you travel to the moon?

SUMMARY OF PLAY IN CONVERSATIONS:

Breaking the fourth wall;

Use against the world technique;

Short fall back stories to test how they would react;

Role playing….take on generic roles and then follow up the role play.

Funny on Command

Tool 1: The Comic Triple

List two things that are positive (negative) and then one negative (positive).

Audiences expect the third to align with the other. This surprise causes laughter

[good things], [good thing] and [bad things].

Greeks gave us science, democracy and little cubes of charred meat that taste like sweat. – Big Bang Theory

Tool 2: Misdirection

Stating something in the first part and then the true sentiment in the second part. I love dogs except seeing, hearing or touching them.

Tool 3: Sarcasm

Usually to exaggerate the situation to the absurd…

Make sure you do this dead pan…

Oh that would be the end of the world…

Tool 4: Irony

The opposite of what was intended. Observing contrasts.

Ironic Simile: “As a sad as a dog with a bone.”

“As flexible as a brick.”

Captivating Stories

Tool 1: The Power of Three

We have an innate desire to hear things in threes the human brain is drawn to patterns of three, the three little pigs, the three bears, the holy Trinity and the three branches of government. Etc etc.

Tool 2: MiniStory

You have to recognize them in our daily stories. Storytelling is telling someone what happened. We must draw and tell stories from our daily lives.

Tool 3: The Story Spine – 8 Elements

“Once upon a time there was _.” You lay out the characters…

“Every day, _.” You lay out their world…

“One day _.” dilemma one….

“Because of that, _.” dilemma two….

Because of that, _. (and so on) dilemma three…

“So….” dilemma four….

“Until finally _.” Climax

And every day after that _. You provide the moral of the story at the end which signals you’re done telling the story The High Point of a conversation could be referenced at a future point in the conversation which creates an inside angle between you and the person you’re talking with Asking the right questions in a conversation is critical by asking the right questions you’re able to elicit storytelling so frame your question as though it requires a story and you’ll get more out of your partner. One ask for a story to be brought as to what you were asking give them multiple prompts Ask them for an emotional angle.

First of all, we tell stories to keep the wolves from the door, mortality, according to Ken Burns. Life is short. There is no solution to learning other than to go and do, which is the best way to learn. There are no rules about films. Ken Burns has been doing it for 46 years, and he does not believe in formulas in documentary films, there is no formula. The only formula is Doing + Learning = Growing.

The Renaissance of Documentary from the 1980s to Present

There are so many documentaries that have emerged in the last few decade that has put the genre on the map. And notice that there is no orthodoxy. Errol Morris, Michael Moore, Al Gore and Werner Hertzog all doing their own things in this genre. Again, no formula. Ken Burns does not do his own narration and / or ask questions on camera.

The Brooklyn Bridge

He felt that biography of Washington Roebling for the Brooklyn Bridge was important. It was emotional. You have to have faith in yourself. That project was Ken Burn’s first in 1981. He had a shoestring budget to make it happen. And a Ken Burns documentary takes especially long, hence he left New York to finish the film and moved to New Hampshire where the cost of living was much more reasonable.

Know Your Creative Goals

Is this what you want to do?

No one is going to give me the budget, you have to beg, borrow and steal!

Transcend: film-making is industrial anxiety, there are 100s of things that can go wrong. You need to welcome the unanticipated problems. You need to have patience.

Be a Jack of All Trades

Writer, sound designer, fundraiser, marketing, and you will give your spiritual life to be a good film maker. Don’t let it be one single skill that you possess: be well-rounded, inquisitive.

Documentary filmmaking is highly collaborative. You need a good cinematographer and a good writer. A film project cannot be a one person program. You have to make your own career path, what are you willing to do for your art go commercial or go public funding, it will still be your art.

Research Everything, Even While You Build the Story

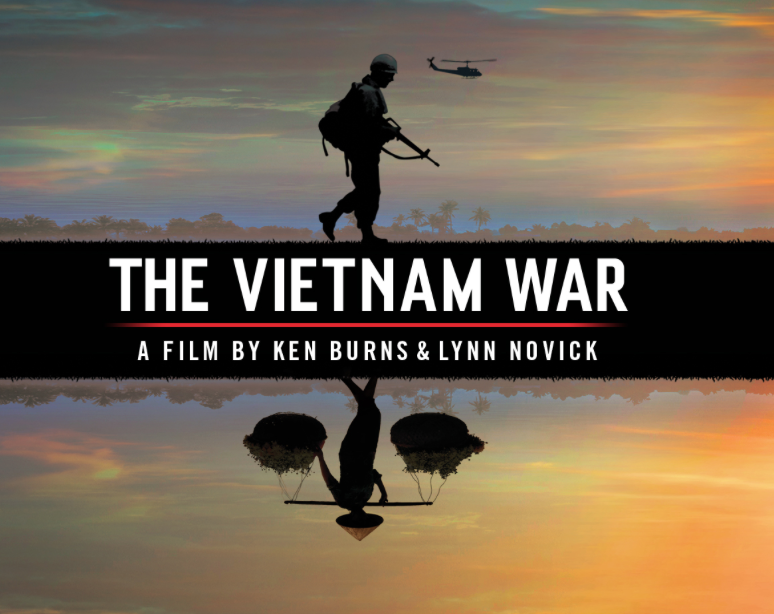

Your model / filter of past is going to be challenged. The opposite view is possible. The Vietnam War ($30M budget) humiliated Ken Burns with new facts. Conventional wisdom is harmful to truth. You have to tell the true story of the Vietnam War which is more nuanced then Ken Burns realized in the outset…same with his audience. That particularly documentary being probably the most important since the Civil War.

The Drama of the Truth

How far can you go with art before you mess with the truth? What have I done in the service of cinema in order to tell the truth? Inclusion and exclusion are both part of the story. There has to be a human act of faith in selecting what is included.

There is no such thing as objectivity. There are a completely different realities and you then have to average things out, according to Burns. Human experience is human experiences (plural) and as you gather them you can more clearly understand that moment. You need to take a certain license, however. The truth is you have may be challenged by a lack of evidence whether it be photographic or otherwise.

The TED Radio Hour: Manipulation

Manipulation is Part of Art

Contradiction is very common in reality. Be manipulative in your story telling. You shouldn’t see manipulation as evil. You need to be manipulative. How do you get along? Manipulation gets the shooting done. If you aren’t manipulative then you are deceiving yourself first and everyone else second.

The Civil War Script

Proposal script for the Civil War had certain sections pre-written before production. You need to write a treatment of your story. You then need to lay out the parameters.

Money is the most governing thing: money is very important.

government,

individual funders,

corporate funding.

You could also develop a bankable story. You need to make the audience no longer understand. Ken Burns’ team writes a lot of proposals.

You have to be realistic budget: how much does it cost for the sound people, editing, you have to pay yourself. Push through: the made a good food, Ken Burns is fundraising and being told 1500 times and 15 times told yes. So Ken Burns is a sales guy in effect.

Structuring the Document Narrative

You want to know how it can be told. We are under the powers of story telling.

Archival information is critical to historical documentary: you need to follow leads.

You shouldn’t look at the great men of history; look at the bottom up and the top down. You should look for the home movies, for example in Vietnam. For example, in The Vietnam War documentary a solider sends home videos back home from the front and the towns people.

Shaping Nonfiction Characters

Liberate the characters of the heroes and villains model. Abe Lincoln, he attacked the US constitution. The Civil War is morally complex.

Layered Characters Drive Narrative

It’s most effective if your audience thinks the character should make other decisions than the ones they make.

Many light bulbs drawn on colorful sticky notes.

Visualize Your Story Boards

He had the episode of using the post it; then they do these different modes in the story.

Balance Larger Themes with Individuals

Good writing is easier building blocks for a better story, you have to have good writing to back the rest of the experience.

Narration is based on 3rd person in Ken Burns films. Ken Burns did not invent narration in documentary film. Do not be afraid of narratives. The word and imagine together are more powerful than the sum of their parts.

The 3rd Person Narrative

Words are not set in stone. There will be many drafts. and then you do a blind session. Does the structure makes sense. Then you do a blind assemblies of the voice over and then the visuals.

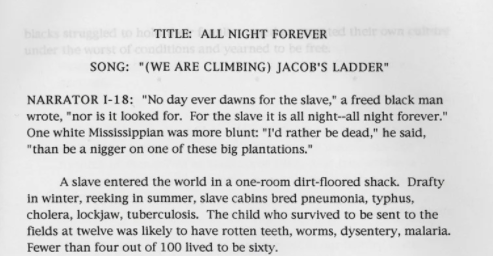

Using caveats which is “may have been” qualifications. Slavery was abhorrent, but the statistics are abstract. 4 out 100 lived passed the age of 60. Born in a shed, most children died before age 12, if they did survive they would work in the fields.

Ken Burns Loves Still Photos

Trust the audience to be more engaged. I will invest those limitations. Ken Burns is an effect is not about giving people a slideshow. The psychological response to a picture.

Imaginative Symbolism

Word and Image is (1 + 1 = 3): Mirror illustration, have the words and the picture talk to each other. We look for the obvious but try to find the dissonant and different because you will find new meaning in it

Jack Johnson Unforgivable Blackness. These past moments rhyme perfectly, for Ken Burns, with what is going on right now in the US.

Selective Interview Subjects: Burns interviewed 1,000 interviewees and got only 100 interviews. Some people don’t want to have stumbling, some people clam up.

Be Honest and Persistent: being completely transparent.

Conducting an Interview

Stay Open to Possibilities: you don’t know what is going to

Conducting an Interview: be very nervous in the interview, be humble. If it doesn’t work, then take the blame and or say we moved in another direction. Ken Burns asks the subject to insert the question into their answer so that editing-wise his voice never has to appear in any of the films. You want to break down the wall and get them to drop their barriers.

Honour your interview subject: you should conduct an interview like you planned to meet him.

Stories Greater Than Facts: The facts aren’t as important as the story about the curiosities. About the stories in the war.

Ken Burns, does not treat his interviewees as transactional. Use your own imagination to effect emotional connection to the audience.

Ken Burns uses live cinematography that are still shots. The magic hour is the sun setting light.

Steal Shots: Sometimes you have to steal the shot if you can’t get access to the a certain area.

Lighting an Interview: make sure that you have eye line, don’t include anything other than the subject. Focus in on the face of the person.

Shoot Interviews with A Light Crew…just easier.

Music is the Quickest to Feeling Art: music should not be an afterthought. Start to use particular themes in the key moments of the film. Get most favoured nation deals for the music. Ashokan Funeralwas actually write in the 1980s but the instruments were of that area.

Editing Process: Trust your editors….Ken Burns actually doesn’t edit his own films these days.

Blind Assembly: worked on the narration, then you just hear a radio play. So you can then start to add the picture.

Messy Full Research Document: The first assembly, it should be very messy. There should be a daunting task to make the film to make it an actual film. Take it piece by piece.

Authenticity: You need to make sure that you convince the audience that this is another new thing, not a summary of someone else’s story.

Private Viewing: You need to follow up with the historical advisors. And then have a lot of bodies there to review the film before launch. Take very particular negative feedback and fix it, don’t give them scripts for the film or they will read that rather than watch the film.

Editing: A Process

It is the principles: You want to be able to edit your answer on how was your day. Tell a story. Not all 1,440 minutes of it.

Tempo In Art: You need to triage the quality of the film, it’s not about imposing yourself. Documentary film making is absolutely a tempo on the screen on musical notation, a film must be rhythmic.

The Vietnam War Introductory: The blind assembly is key, you have the dramatic structure. Scratch narration (use your own voice) until you have the best voice in town Peter Coyote..

It’s the personal story and intimacy of the character that people remember.

The Recording and Using Voice Over: the most important narrator has to be confident. Peter Coyote has to inhabit the non-journalist voice. You do not want to have the dramatic voice be done by a celebrity unless the content is able to flip the audience over so that they are in the scene, and can’t recognize the voiceover as a result. You want the front row lens in.

Rank the Quality of Performance in Real-Time: Give the narrator the script and then circle the narration runs that you liked in rank order.

Never Record the Voice Over to the Pictures: record to the words.

Sound Design: there is a lot of video footage without sound so Ken Burns has to create that. There are 175 recorded sounds in the Tet Offensive sequence of The Vietnam War.

The Artist’s Responsibility: it is the artists responsibility to lead the audience to hell but also to led them out.

Allow Moral Dissonance to Occur: interesting people populated most people. You should not self-select away. It’s not one thing or the other. There are strong divisions in the United States because it is such a vast country.

Decide Your Outlet: Distribution is needed. You want the most number of the people. Ken Burns learned that you give the film to PBS and it gets scale.

Evangelize the Film / Aspiration to Action

Allow the audience to assign their own meaning. You want the audience to have a conversation with you and they are continuing a conversation that they are having that conversation with you.

You need to go out there, nothing happens unless you start. You need to make the phone call to make sure you find that support. You need to jump over the chasm from aspiration to action. Don’t let your mind crush the idea, do something to get started.

Video games Wright has designed: Raid on Bungeling Bay (1984) SimCity (1989) SimEarth (1990) SimAnt (1991) SimLife (1992) SimCity 2000 (1993) SimCopter (1996) The Sims (2000), Spores (2008). Will Wright is the game designer behind wildly success simulation games / non-zero sum games. SimCity was one of the first truly viral single player zero-sum games on the market in early the 90s. He went onto develop SimEarth, SimAnt and SimFarm to name a few. He then developed The Sims which was another massive hit. He also create Spore and is currently working on Proxi….below are notes from his Masterclass as well as interviews over the years. Enjoy!

The Fundamentals of Game Design

You should understand that games are a vehicle that helps us derive an alternative perspective on reality. We observe reality only through our own perspective, games enlighten us by providing another perspective. As a game designer, you are really just building a toy. It is when the players plays with the discrete toy that it turns into a game.

Psychology of the Players, Designers and Co-workers

A major part of game design is to understand how to use game mechanics to try to predict how people will play the game.

Real world simulation is Will Wrights focus. Games are toys. Games have basically borrowed from many other design fields such as:

film,

mathematics,

interior design,

architecture,

theatre,

books,

journalism,

radio,

TV,

cognitive psychology,

fine art,

product design,

engineering,

data science

and other video games.

In order to be great game designer, you need to be well-rounded. You should expose yourself to design fields; how does a designer work? Always think about how to communicate your design basically. Design a game on a piece of paper and you are better off developing on a simple piece of paper then spending a lot time building up a grand design. Share your ideas with others. Same with story telling really.

Your team needs to understand the total vision for this product. You also want to prune your ideas like a tree. Test different avenues to figure out what is working what is not.

Already read up on ‘user centred-design’

Embrace Constraint

Without constraint there is no design. Know the constraints that you have. The constraint can be what are the user constraints or computer constraints.

Design Beyond Zero-Sum Game

Both people can win! It doesn’t have to be violent to be fun. Will Wright was never really interested in zero sum. You don’t have to build the largest city. Certain players are just trying to build fun cities where their imagination can be invested. We are able to externalize imaginary world.

Game Ideas

Once you have a game idea, it’s more emotional = more important to you. Game designer can do any product area and it’s cool. Find your palette for exploration. Ant colonies are very intelligent. So take this into an approachable game because it has the potential to be very emotional.

Research Without Limitations

You had to go to the library. For SimCity, Will Wright had actually started from another game idea which was an helicopter bombing game. Then he researched systems thinking and urban systems to support SimCity. You shouldn’t really look at the real world but rather other research that attempts to understand and describe that world.

The Sims looked at how we spend our lives. How do we improve ourselves. By delivering a speech in front of a mirror, by reading lots of books, your Sim improves their standing in the world. So the game reflects reality but is not a full simulation, it is a still very much a game.

Thinking in Systems: A Primer, Donella H. Meadows. Chelsea Green Publishing, 2008.

A Pattern Language, Christopher Alexander et al. Oxford University Press, 1977.

Flow: The Psychology of Optimal Experience, Mihaly Csikszentmihalyi. Harper Collins, 2009.

Urban Dynamics, Jay W. Forrester. Pegasus Communications, 1969.

Maps of the Mind: Charts and Concepts of the Mind and its Labyrinths, Charles Hampden-Turner. Collier/Macmillan, 1982.

The Ants, Bert Hölldobler and Edward O. Wilson. Belknap Press, 1990.

Gaia: A New Look at Life on Earth, James Lovelock. Oxford University

Press, 1979.

The Ages of Gaia, James Lovelock. Oxford University Press, 1988.

Reality Is Broken: Why Games Make Us Better and How They Can Change the World, Jane McGonigal. Penguin, 2011.

The Medium Is the Massage: An Inventory of Effects, Marshall McLuhan. Gingko Press, 2001. The Society of Mind, Marvin Minsky. Simon & Schuster, 1988.

Blood, Sweat, and Pixels, Jason Schreier. HarperCollins, 2017.

Zero In on A Concept

Look at the components, look at the concepts. How do we think about perspectives. 2 or 3 ideas will gain tractions. Start designing your model. Once you have a general subject for a game you will need to look at different perspectives: for example if you interested in a stock trader, you might want to explore how a stock trader lives and works.

For difficult design choices you will have to trust you gut. Will Wright was not sure about the appeal of The Sims but he knew it was interesting to him. Trust your gut. You should take any experience and should be able to find the interactive and interesting.

Coming Up with Ideas: Randomizer

Want to come up with a creative idea really quickly? Go on Wikipedia an click on the “random article” button. Read the articles that you find interesting…

Build A Tangible Model

Find the fun in the game. Then try to figure out what are the parts that are fun. And build a compass in order to navigate the kind of tree.

You should be prototyping the game at this stage. Turn the concept into the game. Prototype is a way to ask the interaction question: you might have a visualization or graphics question. You need to answer and interact with this and then talk to others.

Figure out Where are the Failure States. How much difficulty is there with using this product.

Answer specific questions for your user testers.

Keeping an open mind is essential, read this story aboutOjiro “Moppin”

The Interactive Process of Research > Simulation Prototypes (Paper or PPT or Graphical) > Game Play Prototypes

We have our own little models of the world. And this influences our behaviour. It’s not really enough to build effective models of the world. Other methods:

You have the toy experiences and other people’s experiences. We are able to build a better model of reality with the addition of new play and new stories.

Cool stories you can deconstruct the universe and then play in them. Games with agency are very different. Will Wright believes you should enable users to tell the story: we fundamentally want to capturing. People want to express themselves through play.

Design Player-Centred Experiences

PT Barnum said “no entrepreneur went broke overestimating the intelligence of the American public.“

You should try to build a mental model of your players head, according to Will Wright.. A magician plays with the mental model of his/her audience. When they use slight of hand to misdirect the audience.

Human behaviour is derived from mental models / filters

I imagine what they think of me. They think of who they are from my perspective, often. We collect data through our senses. We identify patterns. We apply schema to organize experiences and predict outcomes. We are You observe what the hypothesis is and experiment and understand. All our models are played in the schemas (expectations, categorizations), and the model and the behaviour.

Allow your Mental Model to Diverge from Reality

SimCity doesn’t match reality. What is correct, versus what is entertaining? As an entertainment designer, a real city is much more political and not something fun. The real world of municipal government is not a game for Will Wright.

Motivate Your Player, Then Get Out of Their Way

If you can get players motivated. You follow your own games. Once you get motivated, then get out of the way. The most fun people have is when they can draw a cause effect with their actions and the outcome in the game.

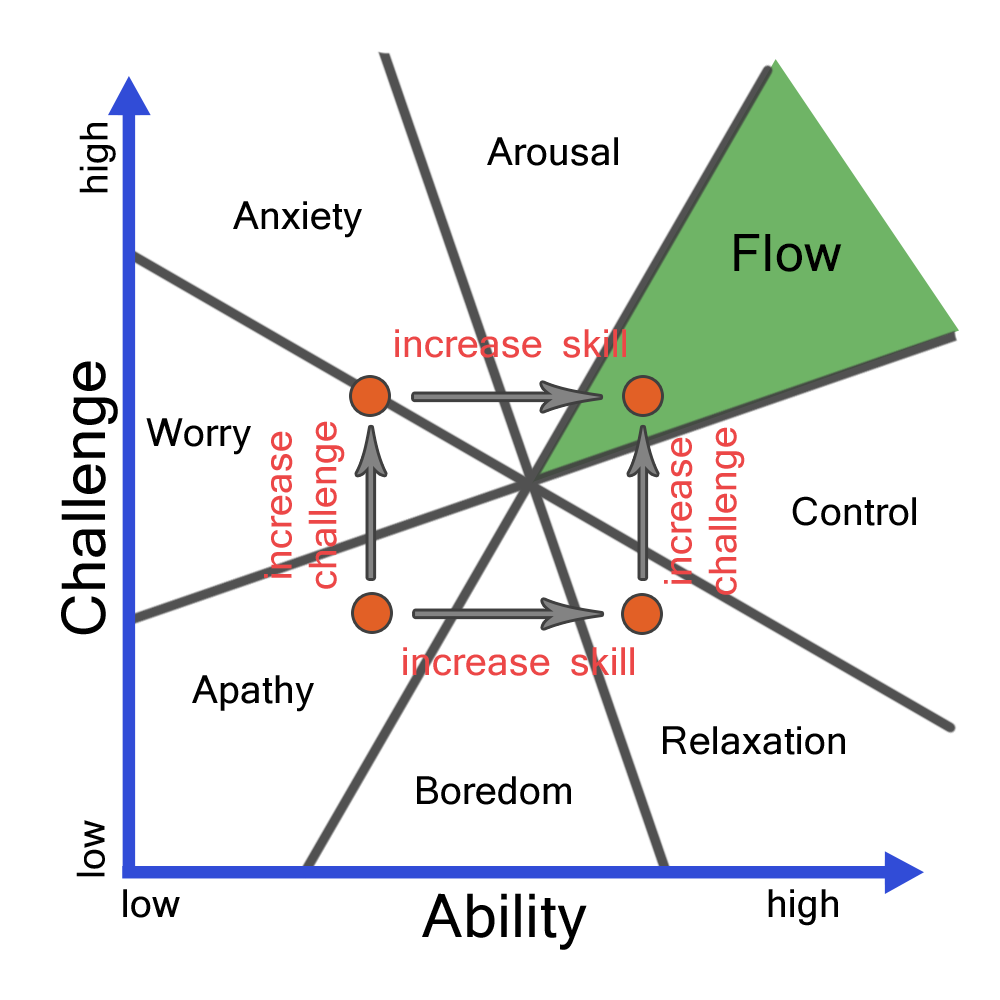

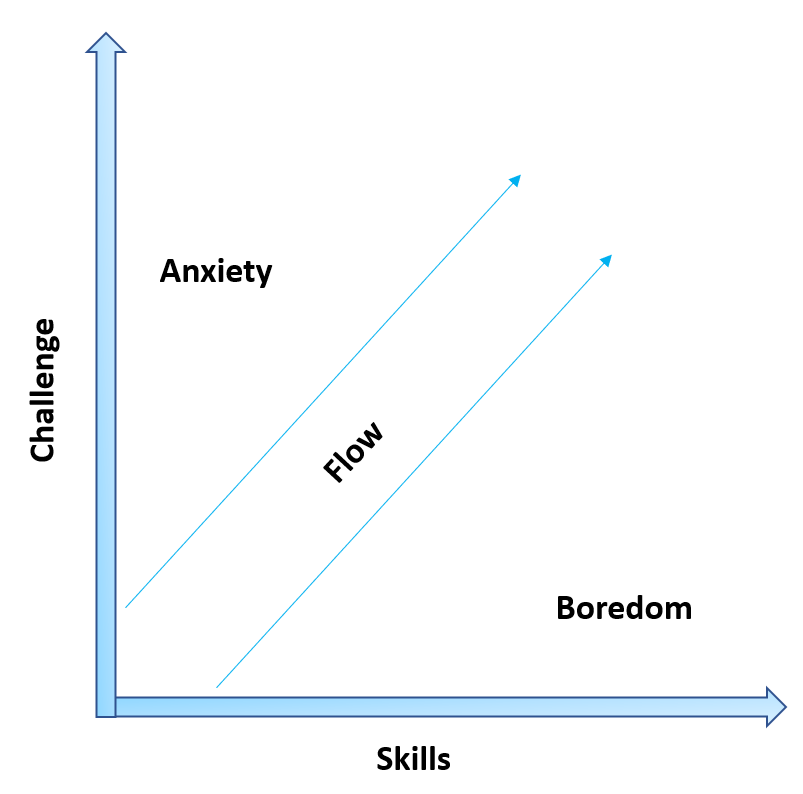

Enable a Flow State

Your game can’t be anxiety inducing and not too boring as well. You want to make meet a flow state: a state of complete absorption in a task, characterized by a slowing of time and a loss of time.

To get your players in the flow state you need to balance the difficulty of your game against the maximum ability of your ;layers. If there are fail states, they should be quick, make sense and factored into the next game loop.

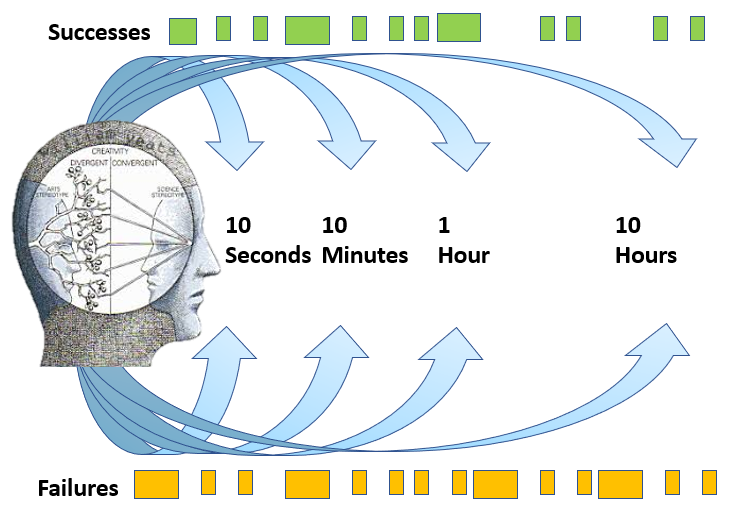

Failure Is Helpful

There was a pottery class where one half of the class was told that their final grade would be determined by the quality of their best pottery. The other half of the class, their grade would be determined by how many pots they made. Of course the more pots you make the better you get at pottery. So the students that were graded by how many pottery projects they finished also tended to have the best quality pottery.Failure as long as it’s entertaining.

Design Nested Loops

You have success and failure. Learn from that longer loops of success and failure in the game. You want to understand the success and failure here. So then you have to have these success and failure loops. There is an orthogonal game loop; this is where some players actually build their own goals in the game.

Make Failure Fun

Will Wright always tries to have a lot of humour in the failure that the player experiences in his games. Make Failure Funny or at least somehwat Fun. That the accident is funny. Will Wright suggests that it is critical that you understand how the system actually works.

The player can choose the goal state. There are sloops of achievement peaks. You want to catch the metrics on testing.

Develop the Games Language

Don’t be afraid to use common metaphors and references to traditional games here.

Use the language of your game to influence players behaviour.

Develop a Game Language: the magic circle they are building a temporary community of games. Are you playing or not?

Rewards and Incentives

There were weird easter eggs in your game? Good.

Reference Real World

Use metaphors:

The Sims is a doll house.

SimCity is a train city.

The metaphor of the trainset.

Designing a Visual Aesthetic

The visual aesthetic is going to define the effect of the game. Look at fine art. Will Wright likes the toy-like feel and more playful and touch able. This is a toy like model like.

Looking at the style of the 1950s comic book covers: the games of Spore was all about being fun.

What can we do to have more involvement and where it is more fun. Art director should try to give you choice; think about the alternatives.

Game Mechanics

What is the locked door, what direction do you need to take to engage in the game. You should have a leaderboard or scoring system, you can add more difficulty to that process.

There are overt rules. Control the player, your encounter the world.

There are hidden rules: SimCity is actually really simple; The Sims don’t speak normal.

The user actually creates a causal; the players are imagining the simulation is better than they think.

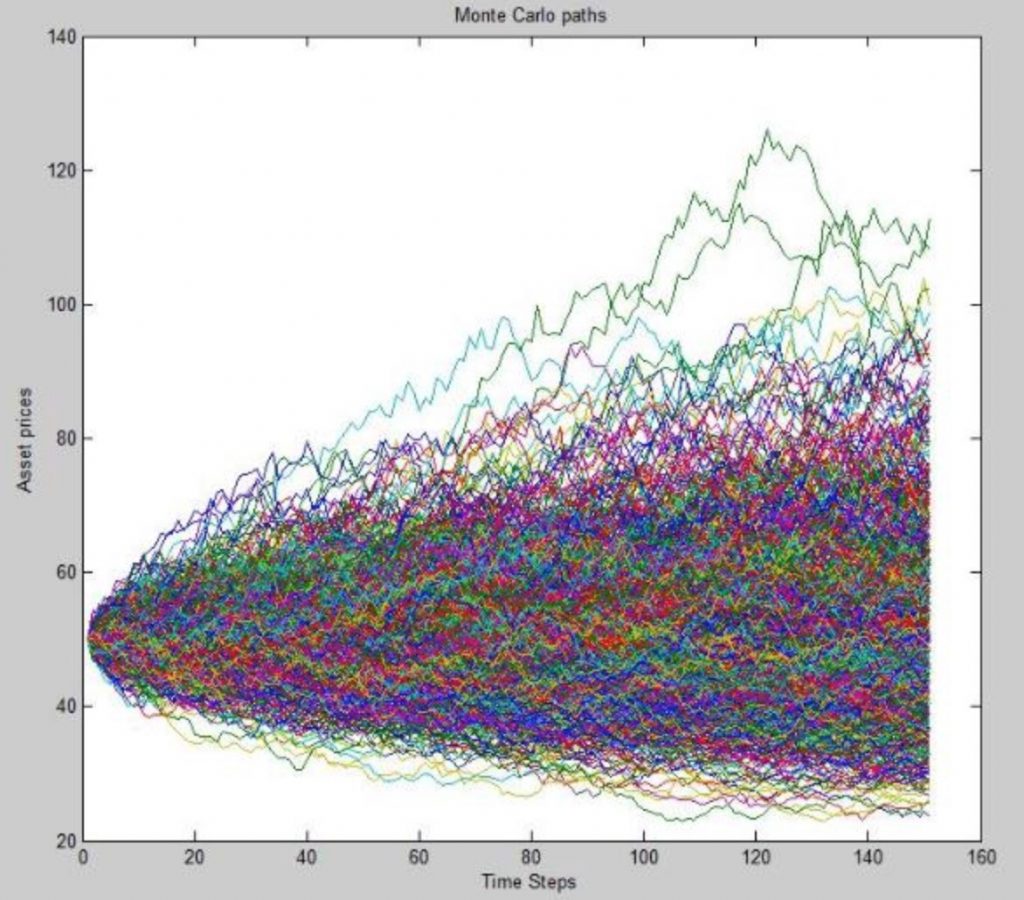

Monte Carlo Method as a Shorthand for Statistics

You throw darts on a board and see where they land. If you throw 100 darts then you will have a breakdown of where they land that can be statistically accurate. This can serve as an alternative to complex pixel counting.

You want to ensure the player experience the signal, not the noise. The player should always want to feel that it is their fault if they win or lose; agency is essential. The lack of agency in democracy is astounding.

Humour is absolutely essential to effective change in people’s minds. The only way to win an argument is to make people laugh.

Iteration and Scoping

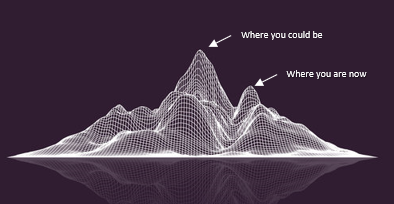

You should recognize when you’ve reached the summit of your local maxima of your design. You need to push to overcome that local maxima by making a dramatic change to find the better design elsewhere.

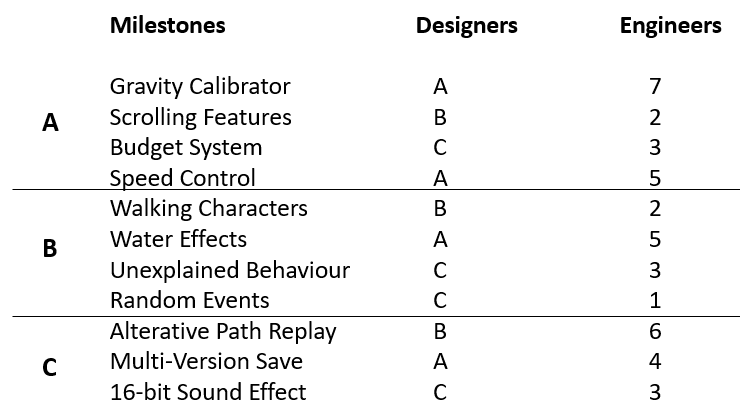

Conduct ‘feature triage’ where your designers assign a priority value to a feature and then your engineers assign effort costs indicating the amount of time it will take to execute such a feature.You should be continually attacking the highest risk. You can then mitigate these different risk. You should try to prune the design tree.

You need to explore really good games; There is this challenge where you have reached the maxima where if we move it slightly it will be worse. You want to find a slope.

When in doubt, double it

If you double it sometimes the idea that is prototype that you are building, you need to recognize failure and the move forward and Will Wright was working on a helicopter bombing game and was designing cities to bomb when suddenly he realized he was having more fun designing the cities. The cities that he was designing turned out to be the most interesting part hence the creation of SimCity.

Playtesting / Kleenex Testing

You start UAT testing of the game. The user might come up with how something fix. Try “Kleenex Testing” just watch two people try to play your game. They will talk to each other about the game. They do not have any assumptions about the game… Find out how they play why they are not pressing the right button. They will explain what they think about the game. These types of testers are helpful, you have no intention of having they play again hence they are Kleenex testers. The model or filter can actually be very different from what I was thinking. Then you need to attack the risks of the user experience.

Steps in Playtesting

Get your prototype to a point where the players can interact wit it without your impacting them by begin directly involved;

Next, invite 3 groups to test. Gamers, non-gamer whatever.

Group the players into demographic groups;

Set up three copies of the game in the same room, have beverages and snacks ready;

Offer a brief introduction;

Rotate through the room with the designers, taking notes. Have the group puzzle through the game. Focus on their frustrations;

Study the notes;

Can that behaviour be used to enhance the game or not?

How can your future designs maximize the feedback from this playtesting?

What patterns did we observe?

What fun was had and what frustration was expressed?

Did we observe unexpected behaviours?

Early Testing versus User Testing

Decipher Underlying Problems: you need to do option of X, Y and Z.

Signal versus the Noise

You want to see what all the problems that these users are having in common. If all these designers can see then:

“Your garden is not complete until there is nothing else you can remove.” Japanese Proverb.

If a player is playing until 5am then you know they love that game.

You can capture metrics for player.

SimEarth, SimAnt and SimFarm

You could adjust the model, Will Wright got caught up in creating the perfectly complex models and saw that they didn’t really like that complexity. The Sims was simply fun because you could mess with the people. You should revisit the assumptions with the way people are interpreting what you have done.

Focus Group Testing Is Bunk

Focus group testing s something that is kind of useless. It’s a big mistake to basically try to get your audience to design your game. They will frequently say what they think the interviewer wants them to say.

Sound Design is very powerful. Players will imagine that the game has better graphics because of the sound design. Film score music is incredibly powerful in effecting player perceiption. And it is a lot easier to prototype music than any other art so getting that right is both critical and very possible.

Fall back on humour. Humour can make any error easier.

Miyamoto and Will Wright

Pitch Early, Pitch Often

The first game you design is your pitch.

Explain your game to people, frequently. You should try to evolve the pitch by watching how people respond. You should try to refine the pitch as you progress. Verbally describe the game. You can pencil out a few details. You should try to pitch in your head. But also with the Sims, the Dollhouse didn’t make sense. You have to rethink, you have to learn to pitch for the consumer. People will start playing the game that you have described in their head as you describe it.

Always Pitch the Feeling, how can I make them feel the best about the direction.

Pitching – Reference the Topic

Here’s why it’s cool to build a city. Talk about this is where YOU can do X. It makes this more interesting.

Pitching – Anticipating Questions

Why is that going to fun. People will try put you into a landscape of games this is just like X game. You can take this into a totally different direction by anticipating their questions. And reshaping their perception.

Pitching Tips

Everything is going to build on it’s own merits. You have to be careful about talking about something that it is not trending. Do not try to catch the latest trend.

There is no one-size fits all pitch. Your investors want to know that this will make them money.

The potential team want to hear about something they would be interested in building it.

Game journalists will want to hear about why your game is exciting and different.

Refine your language based on your audience.

Pitch from the perspective of the player.

Master your log line, make sure your one line description of the game is spot on: Hotline Miami (Devolver Digital, 2012) “Hotline Miami is a high-octane action game overflowing with raw brutality, hard boiled gunplay, and skull-crushing close combat”

Common Mistakes

Never talk about the genre. They tend to provide to much information.

Don’t Fill In the Blanks: important to let the participant fill in the blanks themselves.

The Platform

Technology, the demographic and the type of gamer is critical in console development. Understand your game in relation to the types of platforms that most make sense.

The iOS App Store and Steam has made innovation in gaming more easy;

Player types have different expectations for what you are building and what they are willing to play;

Don’t really on the hardware features of your platform of choice since you don’t want to be locked into one other the other.

The Free to Play model only works if you have millions of players downloading your game since the conversion rate is about 5% to paying users. Whenever you encounter a micro-transactions in a game decide if you enjoy that or find it exploitative.

Consider the Economics

You have to fundamentally think about something cool and only then choose to monetize it. Some people are uncomfortable with that. Do not lead with monetization, always lead with value creation first.

Leadership: you should try to instill the design team to the team. You should try to find talent on the team.

You don’t want to be wasting too much on meetings: group memory.

Look for Outspoken Collaborators

You want to have constructive meetings, you would have a cannery in the coal when someone asks a pointed question. You should stop the meeting at somepoint. Arbitrary time frames like 1 hour should be avoided just stop the meeting.

Be comfortable with criticism

Seek insights from your entire team

Use a game design document to keep track of your project

AI could Fundamentally Craft the Game

Neil Stephenson Diamond Age: the computer is customizing the game around you to make it more interesting and then have people that have a shared vision meeting each other.

Game Ideas – Be Open Minded

Take a board game and add or subtract a few rules to see how it works.

Think in systems…

You will need to be open-minded to design the future. The best way to predict the future is to invent it.

This publication is dedicated to finance, politics and history