Dollarama: Looking at their Industry leadership in Canada and Earnings Management 101

- competing on price

- cost leadership

- cheap product retailer

Dollarama IPOed in 2009 and become a Canadian darling trading as TSX:DOL. Then in June 2014 which is the first quarter of their 2015 financial year (fillings standard), they changed the useful life of all their stores & additional fixed assets from 10 years to 15 years. So what? Well, this spreads the rate of depreciation over a longer life time. Assets stay on the balance sheet longer and that means that Dollarama has a lower amount of depreciation expense per year. Since depreciation expense take away net income, the effect is that: in Dollarama’s case:

- they gained $0.04 per share increase by in effect tweaking the depreciation rates of their stores.

- David Milstead of the Globe and Mail said the reasoning behind this is that “Dollarama needed to keep the P/E at 21 versus 16.”

What Milstead is arguing is that Dollarama had to hit analyst expectations. Gross margin was down in the first quarter so how was that going happen?

You can imagine the C-suite discussion: “We wanted to maintain a premium valuation.” What’s a bit shocking is that adjustments on the depreciation rate of their stores made up for exactly the short-fall. Weird right? Although Dollarama could legitimately set depreciation for their stores at 15 years; it is plausible deniability. The kind of activity that draws similar behaviour in both corporate and political decision-making. Only through a premium valuation can Dollarama maintain its $21 Price over Earnings ratio. However in the long term, this C-suite decision would have a future impact on CAPEX. Cost leadership by gross margins were down and trending lower. They can’t increase prices; they have nothing to divest. They have few receivables (i.e. beyond gift cards). They could delay paying suppliers? Or they could only fiddle with depreciation. What’s the future impact on depreciation? The net income goes down in future years!

Depreciation as Form of Earnings Management

Depreciation as Form of Earnings Management

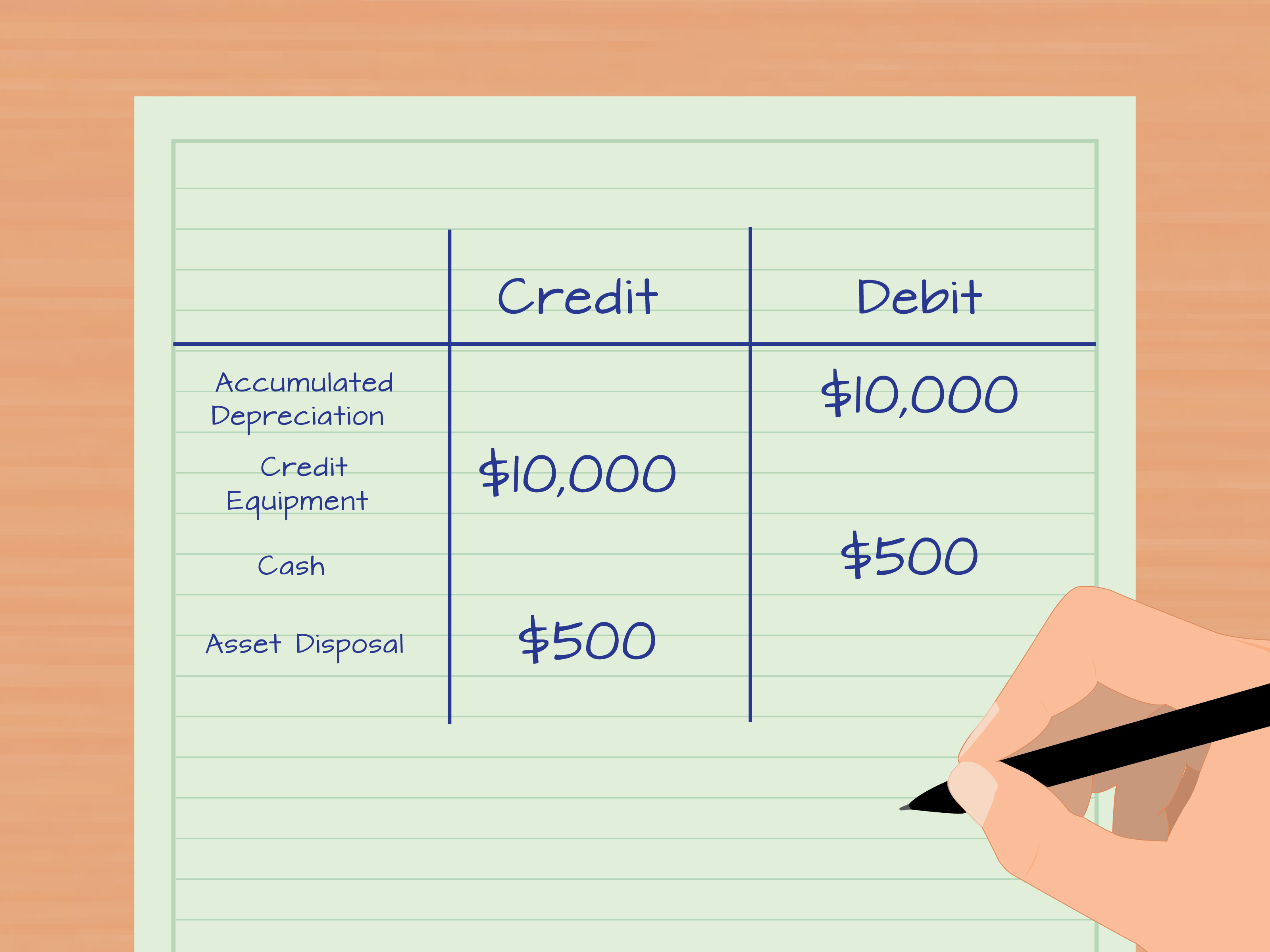

Recall that Depreciation is used to explain how much of an Asset’s value is used up. And then it is matched the expenses of an asset against the income that asset earns. Depreciation is used for income tax purposes to degrade assets thus reducing the tax burden on a business.

A straight-line depreciation would have a tangible asset worth $500K with a 5-year useful life. Every accounting year, the firm expenses $100K which is matched with the money that the tangible asset creates each year. Therefore, when you change the Depreciation from $500K over 5 years to 10 years, that means you would expense $50K per year rather than $100K which means the asset stays on the books for longer.

Depreciation sits on the balance sheet as a reduction from the total gross amount of a company’s long-term Property, Plant and Equipment PP&E. In other words, if you keep the PP&E longer on the balance sheet, it will benefit the earnings / net income. When an asset is retired or sold, the total amount of the accumulate depreciation associated with that asset is reversed, completely removing all record of the asset from a company’s books.

Depreciation sits on the balance sheet as a reduction from the total gross amount of a company’s long-term Property, Plant and Equipment PP&E. In other words, if you keep the PP&E longer on the balance sheet, it will benefit the earnings / net income. When an asset is retired or sold, the total amount of the accumulate depreciation associated with that asset is reversed, completely removing all record of the asset from a company’s books.

Depreciation expense is a non-cash expense because the monthly charge on a company’s income statement is made by a monthly recurring depreciation entry. A depreciation expense on a company’s income statement is debited and a company’s accumulate depreciation expense is credited on its balance sheet. If you reduce the depreciation expense over a specific period, it is the depreciation expense itself that reduces the earnings as a non-cash charge on a company’s income statement.

Off-Balance Sheet Assets: Leasing – Capital vs Operating

Operating lease is off the balance sheet only appearing in the Income Statement.

A true lease

Capital Leases: the lessor transfers ownership of the asset to the lessee who gets the depreciation for the asset. The lessee has to list the capital lease and gets the depreciation from that asset.

Operating Leases: are where the lessor owns the asset and all the costs and benefits (depreciation) associated with it. The lessee merely rents out the asset and pays a lease fee. The tangible asset is off the balance sheet.

Knife-edge criteria e.g. – under US GAAP, a lease is a capital lease if any one of these four hold:

- Length of Lease extends to >= 75% of Useful Life

- Ownership is transferred of title at end of the lease

- Bargain Basement clause at the end of the lease

- PV(Payments) @ “appropriate” discount rate >= 90% of Fair Value

Firms will often structure leases to ‘just’ avoid capital lease. i.e. Many Operating Leases be a Capital Lease in disguise.

Operating Lease:

Debit Rent Expense

Credit Cash

You have no application on the balance sheet:

Capital Lease:

Debit Asset

Credit Liability

Plausible deniability: you have a plausible justification that masks (convincingly!) another objective. Create your own schedule, flexibility, aim for the highest support, money. The true economic reality of a firm and what is presented in the financial statements: The role of financial statements in valuation does not rely solely on reported profit.

Operating Lease versus Capitalized Lease

Operating lease: the transaction appears on the Income Statement. >= 75% of it’s useful life. Ratios are better: Return on Assets (sales are not in Operating Lease). Fewer journal entries. ROA is Return on Assets = Net Income / Average Total Assets. Capitalized Lease is BS + IS

- Debit Rent Expense

- Capitalized Lease; the transaction appears on the Balance Sheet and Income Statement.

- Debit into Expenses

- Debit Liability

- Credit Cash

Who is Fooled?

Banks can observe this activity as well. They are not fooled.

Off Balance Sheet Finance

Debit Covenant: when a company is given a target performance range by investors that they must follow.

Ebit/Int

Off Balance Sheet Finance

But

Ebit/Int+Rent

Moody’s Agencies: {Not Fooled Either} Air Canada – standard metrics + Moody’s standard adjustments. 8.3 billion adjust to long term debt. Balance Sheet: -> present value of Capital Lease

Air Canada Case

You need to get the present value of capital leases. Air Canada added Cap Leases. Investors trade on heuristics: so yes, Investors can be FOOLED. Take Operating Lease for the next 5 years. Cost of Debt 7.32% You can almost double the debt load. If you capitalize your Operating Leases the firm looks totally screwed. Take all the debt to the end of 2004

Intangible Asset (Off the Balance Sheet)

- Intangible assets include intellectual property, brand equity and goodwill.

- Intangible assets are categorized into two categories;

1) those that appear on the financial statement and;

2) those that do not appear on the financial statement.

R&D Expenses are almost always expensed. There are some expections; software firms where accounting standard allow for the capitalization of development expenses after product feasibility has been demonstrated. This rule applies for internally generated intangibles.

If the pharmaceutical firm develops a patent, that patent is not recognized on the balance sheet.

If the pharmaceutical firm purchases patents form other: the value of the patent appears on the balance sheet. It is difficult to determine the value of intangibles. Spending money on R&D or advertising does not guarantee a benefit to the firm. However, when assets are acquired there is an explicit or implicit valuation for the acquired intangible asset.

Is R&D an Asset?

In the US all R&D is expensed. On the balance sheet; there is a liability. There matching entry is on the shareholders’ equity and deferred taxes.

What about Advertising: Energizer Bunny didn’t improve Duracell’s sale

Goodwill | <- Intangible

|

Net Assets |

|

Valeant Case R&D is expensed in the US but R&D is Goodwill and Intangibles.

What are the future benefits of its assets?

Goodwill: I can’t sell that much.

Intangible assets are massive: you can put the intangibles in the Goodwill and not in Net Assets. ROA (return on assets) was low 1.2% organically

The telltale signs of distortion on in the ROE, firms with intangible industries will have ROEs much higher than firms in other industries and also much higher than their costs of equity.

ROE = Net Income / Total Shareholder’s Equity

ROA = Net Income / Total Assets

You have R&D of $10 billion as Intel. But your balance sheet shows under $5 billion of identifiable intangible assets. Intel R&D using a three year straight line amortization period; what this means is that you don’t expense R&D as incurred but capitalize it and amortize it over a three year period.

Intel is close to steady state which means the impact is more muted.

You only grow Goodwill by acquisition.

- 13 Billion Down

- 2 Billion

- ROA 8.4%

ROA inflates if the most important assets isn’t in the denominator. You are growing by acquisition. Synergies: not tangible, you can’t give to another firm. 11 Billion out 13 billion means you have negative equity.

On Balance Sheet – Intangible Assets

Why On Balance Sheet distorted?

In this case, the intangible assets are overstated on the balance sheet.

Two types of intangible assets:

- Amortization period not appropriate (for finite lived intangibles): these are patents which expire after a set duration. Finite lived intangible assets are amortized over their useful life.

- Impairment not taken (indefinite life intangibles): these are goodwill or trademarks. Indefinite duration assets are typically evaluated periodically for impairment.

Where Crucial

In addition to I.P. intensive industries, also M&A intensive firms/industries. HP and CGI for example.

Telltale Signs

Others taking impairments, especially for goodwill while this firm is not taking impairments.

Firms hate to take goodwill impairments as these are a tacit admission that the acquisition was a failure: goodwill will reflect overpayment.

Remember that Goodwill impairments are not tax deductible while fixed asset impairments are! Therefore with Goodwill impairments, the impact will be felt in Net Income and Correspondlu in Shareholder’s equity.

![]()

Hewlett Packard | Autonomy

The HP acquisition of Autonomy: ‘Get Rid of Goodwill?

You need to do an Impairment Test (for your information) there are 4 steps.

PV = FCF/(r-g)

The g will massively impact your PV, so in terms of financials you can massively miscalculated the PV.

Valeant doesn’t tell you about the inputs into the Goodwill impairment and we get wildly different results. HP had a 9 billion 2012 impacted due to the Autonomy situation.

Autonomy $9 billion, they paid a premium of 65% over the target’s trading price. HP recorded a $6.9 billion goodwill and $4.3 billion of other intangible assets. HP overpaid and they had to write down $8.8 billion. $5.7 billion was written off goodwill, while $3.1 billion was written off the intangible assets.

On the Income Statement you see charges for both these impairments; The balance sheet, impairments of $8.8 billion totally towards goodwill and other intangibles and an entire impact of $8.8 billion on equity as these impairments are non-deductible.

- flexibility of write downs

+

- Poor profitability

Therefore, it’s possible that there was a Big Bath: Autonomy founder suggests as much: it’s a write off quickly. Write off over 10 years versus write it all down now.

They choose to write it down NOW, indicating a Big Bath.

HP’s Big Bath

https://en.wikipedia.org/wiki/HP_Autonomy

Liability Distortions

RRSP and 401K are Defined Contribution Plans:

Remember: Conservative Accounting Versus Aggressive Accounting

- Being conservative is Asset DOWN Income DOWN

- Being aggressive Assets UP and Income UP

Deferred Revenue

Why do deferred revenues get distorted? Deferred revenues can get distorted when firms manipulate the criteria for revenue recognition. If a firm is aggressive, it may choose to recognize revenue prematurely, increasing revenue and thereby income, and lowering the deferred revenue liability.

Where it matters?

Deferred revenues are important in businesses where the operating cycles are long; where project often span multiple years and where there is a mismatch between the receipts of payments from customers and provision of goods/services.

Example, Microstrategy was accused of aggressive revenue recognition. Essentially, had multi-period contracts for software service Instead of deferring the revenue and recognixing it over the life of the contract. For the year 1999, Microstrategy admitted to overstating approxiametaly $50 million in revenue.

Deferred Revenue

- Instead they should treat it as deferred revenue

- When firms get paid, before they provide a good/service, they should not treat it as revenue.

- In the future year, they recognize revenue (cr.) and remove the deferred revenue (dr.)

- Often firms are aggressive and prematurely recognize revenue

- Adjustments are similar to channel stuffing with an increase in liability (deferred revenue) instead of decrease in an asset (accounts receivable).

- Micro-strategy example – prematurely recognized 50 million of revenue (and 2 million of associated cost)

Reserves

Reserves

When you recognize the impact of the expenditures before the expenditures actually occur.

- Warranty Expenses Debt $5 million

- Warranty Reserves Credit $5 million

Reserves can be distorted at both times either at origination or at the time when then the expense is incurred. You can have expenses diverted to reserves instead of the income statement.

Where Might This Be Crucial?

In industries where warranties are crucial. Restructuring reserves are crucial as often the ‘turnaround that has been shown by the new management can be a fiction of the accounting treatments.

Telltale Signs:

Unexpected improvement in cost ratios on the income statement, along with a corresponding decline in reservices.

Pensions

Defined Contribution Plans:

Defined Contribution Plans:

- You have Assets and Liabilities which are equal to each other.

- These plans tie you to a given company for example:

- GM: $50 BILLION liability because they had a contribution plan.

- Car company: $2500 per car went to cover Post Retirement Healthcare costs.

- The risk is with the employee.

- Contribution Plans are portable?

https://en.wikipedia.org/wiki/Defined_contribution_plan

Defined Benefit Plans:

- Risk is to the employer.

- The present value of the future payments to be made to the pension plan is the PBO (projected benefit obligation). If the Net Assets of a pension exceed the PBO, the pension plan is adequately funded.

- If the Net Asses are lower than the PBO, then the pension is underfunded.

- This is a portable plan which you can take with you anywhere you like.

https://en.wikipedia.org/wiki/Individual_Pension_Plan

Pension Plan sits under the COGS, SG&A or some other expense category. Pension Expense has three components: a) service cost, b) interest cost and c) return on plan.

Distortion in Pension Accounting:

Some because of the complexity of the standard and some because of the manipulation.

Where might this be crucial? Pension related issues are important in labour intensive and unionized industries, usually more so in older legacy companies.

How old are my fixed assets: accumulated breakdown: Apple outsources to Foxconn. Apple has Operating leases for their Apple Stores.

Discontinued Operation

Discontinued Operation

When firms discontinue a line of business, the results are then restated for past periods: usuall past 3 income statements and last 2 balance sheets….

They want to prevent firms from disposing of entire lines of businesses in order to improve net income. Amy gains and losses will be reported separately. The Net Assets from discontinued operations: this represents the assets less liabilities of the discontinue operations.

Changed in Accounting Principles

You could change accounting principles regularly in order to confuse Equity Researchers.

Cumulative Effect of Accounting with Pro-Forma Disclosure

- Say a company changes from one method of depreciation to another.

Governments love depreciating assets;

- New assets get depreciated well before new investment.

- Citizens hate to see reinvestment in older infrastructure.

- The government only wants to invest in older infrastructure when it really really needs to be fixed.

- They have to issue debt or raise taxes to get more revenue.

Grss PP&E Acc Dep

_______________ _____________________

11billion Credit 4billion

10.7bilion Credit .700billion

Net PP&E

7 |

BA versus Luftansa:

- BA’s long-haul planes depreciate at a lower rate because they have fewer take offs and landings.

- Luft has less turnaround times, smaller planes therefore higher rates of depreciation.

British Airways

Gross PP&E Depreciation Assets

Layer useful left high

18 to 25 years for their assets

Lufthansa

- When you balance those two together you get

- 12 years for their assets.

Lufthansa has smaller planed, depreciation is much fast, more takes and landings. Gross PP&E/Useful Life = Depreciation Expense. 12 years depreciation with a 15% salvage value.

Average Gross PP&E

- Useful Life

BA .60 .61

Luft .63 .64

Gross PP&E Acc Dept

Dr. | | Cr.

$23.2B | |$12.6B

Net PP&E

Dr. |

19.6B |

So if you were to use the same depreciation. Equity increases when you depreciate faster…