Your first idea for how 2 fix a writers block is rarely ever the best. Think about how you can engineer your story to maximize the fun…

You have to find the piece of the story that we can connect with. Drinking stories and vacation stories are not good because they are a series of ANDs…I did this and this….us But & Therefore, Cause/Effect.

Your story should be tell-able at a dinner party: KISS = keep it simple, smartie-pants.

You should practice telling your canned stories at said dinner party. But never in front of a mirror that’s not how you’ll tell it in the wild.

Rule #2: Harvest the Mundane & Audiences will Connect

People want to engage by seeing themselves in that story. Just say no to jumping out of an airplane, epic adventure and say yes to arguing with your spouse about the dishwasher! Make your story little.

Create a spreadsheet called the Homework4Life™: column 1: date, column 2: write a snippet about the most eventful part of your day.

Write down snippets from your live memories when they pop into your mind so that you can harvest later.

Self-discovery requires the reflection habit to form which means taking 15 minutes a day. It takes time to hone in on your stories. §Harvest in your daily life and you will find other memories.

Rule #3: Homework4Life™ Is Better Than Anything

Use stream of consciousness to populate your Homework4Life™ spreadsheet on a daily.

Forget what the education system has taught you: ie. to have a main message (thesis) and your arguments to back that thesis. This approach is deeply alienating. §Use a pen/keyboard or speech-to-text into your phone so that there are no pauses.

If you have pauses/writers block start listing colours until a new memory is triggered based on association. §Storytellers needs to selfishly guard their time: that means early morning or a locked door.

Rule #4: Unearth Stories with First / Last / Best / Worst

Create a spreadsheet called the First/Last/Best/Worst™:

Scan your memories based on these 4 questions.

What was your first ____? What was your last ______? §What was you best ____? What was your worst _____?

Rule #5: Five Second Moment i.e. Jurassic Park is not a dinosaur movie

The reason you put pen to paper is you had a 5 second moment of profound realization and you think others should know about it.

Profound realization = a moment that changes your life fundamentally

“I love this woman but she wants kids. I hate kids. Then after saving two kids I realize I do like kids. And my sweetheart and I ride into the sunset.” – Dr. Grant from Jurassic Park §Realization should be the polar opposite of the start of the story.

Rule #6: Find Your Beginning (the Opposite of the End)

Your story should end with the five second moment of realization.

Your beginning should start at the extreme opposite: start afraid end fearless, start happy end sad, start uncertain end confident, start hopeful end not, start angry end grateful. The opposite can be good or bad, just make sure it is the opposite of the end to maximize the story.

Every good film starts with the main character moving to the opposite by the end of the story. In other words, the main character has an arch.

Rule #7: Create High Stakes, Why is the Best Question

Why is the best question you can get your audience to ask (engage!)

A) The Elephant: An elephant is the thing that everyone in the room can see: it is the need the want, the problem, the peril the mystery. It signifies where the story is headed.

Elephants can change colour: it can flip to create more surprise.

B) Backpacks: increase the stakes by increasing audience anticipation of what is next because you laid out the plan and now we are watching with you as you execute. Ocean’s 11 has a plan that ratchets up.

C) Breadcrumbs: leave little hints for future events but only enough to keep the audience guessing (engage). Find a breadcrumb that maximizes the number of guesses the audience can make. Of course, the completely unexpected is the most effective story.

D) Hourglasses: take the audience to the brink of the big reveal but then provide insane detail. What is the story teller gonna do next? Please get to the punch line! This is hurting my brain!

E) Crystal balls: audiences want to run ahead often. Here the storyteller creates a false prediction of what is going to happen next. We are programmed prediction machines. Get your audience to engage your story. The storyteller’s prediction is strategic.

Rule #8: Don’t Be A Dufus (public speaking rules)

Do not praise yourself: no one wants this amazing AND awesome person.

Be self deprecating: no one likes a know it all.

Don’t ask rhetorical questions: it derails the cinema of the mind.

Offer one granular bit of unique value, one 5 second moment. A small memorable and useful idea for the graduates: if you’re valedictorians.

Don’t cater any part of your speech to the parents of the graduates.

Make your audience laugh: the comic triple, sarcasm, irony, intentionally miss.

Do not talk about the weather if it’s hot everyone knows it…

Do not be formal in your speech be casual like you’re speaking to a friend.

Be excited, hopeful and enthusiastic: the audience wants a Yes, Ladder.

Don’t describe the world the graduates will be entering because you actually don’t know the world, you only have your perspective on the world even with modest data.

Don’t define terms based on the Webster dictionary: it’s just lame.

Don’t use a quote that you’ve heard someone use in a previous commencement address. You’re goal is to provide new insight that’s why you’re getting this degree.

End your speech in less than the allotted time: brevity is the soul of wit, “If I had more time, I would have written a shorter letter.” – Blaise Pascal

Rule #9: Permissible Lying in Storytelling from Your Life

Lie 1# Omissions: if there was a third person who is not relevant simply don’t distract the reader with their presence since that’s distracting.

Lie 2# Compression: if it took 5 days then compress into in an afternoon if credible. Every film compresses time into a 24 hour story almost always. It creates pace & urgency.

Rule #10 Create the Cinema of the Mind, Visuals

Storytelling must put the audience in a location that they can imagine on their own. Every moment must be situated in a physical location the audience can create in their own mind thus engaging them fully.

Never open a story with a philosophical point, a thesis.

If you need to explain something philosophical, then the audience in the classroom w your teach or judge’s chambers with the lawyers or the stock exchange or where ever that idea can be credibly expected to be discussed. §

Rule #11: Use “But” and “Therefore”

Cause & Effect causes the human brain to release dopamine. §DO NOT CONNECT sentences with the word AND. AND kills.

“But” and “Therefore” are the ligaments of storytelling. §“But” = although, however, nevertheless, still, though, yet, on the other hand.

“Therefore” = so, then, thus, consequently, for, and so, hence, since, to that end, on account of, on the ground.

The story is a chain of cause and effect events…destination is the five second moment of realization.

Rule #12: Surprises Elicit Emotional Responses

Paint a rosie picture of scenic day and then suddenly WAM!

Never present the thesis statement before your surprise.

Never say what this story is actually about, let the audience ride.

Always hide critical information in clutter or innocuous details.

A laugh line is a good spot to hide a key piece of information.

Save the last big laugh for the end. Do not blow the joke early.

The Baby Blender rule is that two things that don’t go together are smashed together, typically humour ensues.

Rule #13: The Present Tense Is King

Part of the Cinema of the Mind is to make it happen right now.

Using the present tense always is very effective for keeping readers in the moment itself. Get your audience to time travel with you to now, this story is happening. Let the audience create the vision of the events as they unfold.

Rule #14: A Hero Must Start the Story the Opposite

Failure is fare more engaging than success from the start.

Marginalize your accomplishments: know you aren’t perfect. Be the underdog in the story. We love underdogs!

Malign yourself: tell the story of a small success.

Rule #15: When Performing

Get your audience to laugh in the first 30 seconds of your story.

Don’t memorize every word of your speech. Instead:

Always start strong: the first few sentences should be memorized.

Always end strong: the last few sentences should be memorized.

Know the scenes of your story: MAXIMUM 7 Scenes to remember, memorize the colour which indicates mood of the scene.

Make eye contact with three people in the audience. One on the left, one on the right and one person in the centre to move back and forth between.

Control your emotions as the moment of intense emotion arrived, change the perspective from your vantage point to 3rd person so that you don’t cry on stage.

Notes are from a combination of Matt A, Alex H and others at McGill in 2006.

• Compact theory of Canadian confederation

Compact theory is the view that the constitution is a political agreement (or compact) between the country’s 4 colonies entities (Upper and Lower Canada + New Brunswick and Nova Scotia). And as such, Nova Scotia and New Brunswick should have massive influence today regardless of the demographic, economic influence of those two provinces today. “It was what was negotiated to even create the country, so we need to continue upholding what created the country in the negotiation.”

o a pact between provinces to respect the provincial jurisdictions o an agreement between the British and French people in Canada

• George Stanley’s 1956 paper o compact of cultures rather than of provinces o Quebec represented French/Catholic culture and Ontario represents the English/Protestant culture o this compact of cultures evolved into a compact of provinces as time passed, but this wasn’t the original intention of confederation o distinction between founding provinces and those that were born out of the federation (Alberta and Saskatchewan) o Stanley argues that Quebec continued to subscribe to the idea of a cultural compact

• FACTORS THAT LED TO CONFEDERATION

o American Imperialism o Fear of westward expansion of United States o Need to improved railway communications o Political impasse in Canada this was due to demographic changes • Gradually, Canada West (Upper Canada) began growing very quickly • when Upper Canada realized the demographic situation they were in (they were in the numeric majority) they wanted representation by population • English speaking Protestant part of Canada wanted a more centralized union

George Etienne Cartier, George Brown and John A MacDonald

o this was the view of Sir John A and George Brown the French wanted to ensure that they kept what they were keeping what they were already given by the British government “only federalism would permit the two distinct cultures to coexist side-by-side within a single state…but not a fuzzy one, but rather one that is more clearly stated” a new Union would be federal in character…that the power of the federal government would be national and the power of the provincial would be local • education is split between the federal and provincial government the residual powers would be given to the central government • ROC = Rest of Canada • the constitution lets the federal Parliament and Senate to legislate for the “peace, order, and good government” of the nation • Section 91 of BNA Act gives federal powers • Section 92 gives provincial powers o there has been a shift towards more powers for Section 92 • Quebec would argue that here HAS NOT been more powers shifted towards the provinces, and would argue for MORE provincial powers

• Siegan report deals with the ideal of “Fiscal Imbalance” o argues the federal government assumed a large burden in 1867 o because of the powers that it assumed, it required heavier financial “passing” o constitution of 1867 empowered the fed government to levy taxes by any means while it attributed to the province’s field of direct taxation, …, …, … o the fed government was allowed to levy excise tax and custom’s duties

o DIRECT TAX VS INDIRECT TAX

direct: like the GST indirect: more of a hidden tax (tobacco) • giving the provinces the power of indirect taxation was NOT a large gift because they hare HEAVILY unpopular with the public and could result in being held politically accountable (during a provincial election) o by giving up the indirect tax (excise tax), they gained in exchange a per capita subsidy

-asymmetry lets some provinces have more powers than others

Twentieth Century Debates in Federal-Provincial Relations

-1884 J G Robins (treasurer of Quebec) pressed for four demands 1) Compensation paid to Quebec by federal government for the expenses associated with railway construction 2) Increase on per capita subsidy, above what was provided in the BNA Act -provided based upon the 1861 census -increase in subsidy would change the amount that was being given in 1861 3) The interest of Quebec’s share of the surplus debt -by joining confederation, Quebec began with an economic clean slate 4) Relieved of the cost of the administration of justice -cost increased annually as the population increased

-188* Ontario treasurer (S C William) -since Ontarians were responsible for half of the federal income, the potential buyout of the Montreal buyout would cost Ontarians millions. Therefore, Quebec had to find its own way to resolve its financial plight. This is because he blamed their issues on bad spending habits.

Quebec was in financial straits early on in Confederation

Quebec believed that confederation was the cause for this economic trouble Ontario believed that it is not a problem based on the rise of confederation; it is Quebec’s own making that caused the problem

1930 study by James Maxwell -argues that the growing difficulty that Quebec encountered in meeting its debt payments was the principle reason for the reevaluation for the 1867 confederation settlement -when the debt settlement in 1873, the general settlement (t granting of one favor) simply led to the wanting of another

Political reasons for this disagreement:

-Liberals were in power in Ontario between 1872 till -Conservative government in Quebec -Ontario’s lack of sympathy isn’t for no reason…they were conflicting governments in power

Cultural reasons for this disagreement:

-the cultural and religious differences were seen to be significant

Claude Ryan talks about the idea of “concerted action by the provinces” -the father of inter-provincial relations was Honore Mercier

Ontario 1887, Honore Mercier convened the first inter-provincial minister conference -premier of NB, NS, and BC didn’t join -discussed issues relating to federal government subsidies -discussed outstanding issues between Quebec and Ontario -Treasurer of Ontario decided to also take extra subsidy if Quebec gets more….if Quebec gets more, then Ontario will too….but Ontario doesn’t want anyone to get more “-if Quebec gets relied from its financial embarrassment, Ontario should receive the same”

-the proponents of subsidy increase argued that the federal excise and customs duties (which the provinces gave up to the federal government, rose significantly since 1867), therefore the provinces deserved more

Provincial and Regional Identities

Brownsey & Howlett, “The Provincial State in Canada” in PROVINCIAL STATE

-cultures as equated to ideology -philosophy of liberal/conservative thought

-political economy standpoint: -these (cultural) ideologies interact with economic forces

-formative events or founding moments in provincial history -e.g. founding -Seymour Lipsan: provinces are the products of a single, formative event -the American Revolution is that event formative events are subject to four subjects (events along the way that might change a culture): 1) Stress 2) Periodic assault 3) Possible modification 4) Cracking

-Newfoundland could not be forced to adopt responsible government or confederation -this formative event is significant to Newfoundland’s political culture

Jedwab’s 5 Points:

1) Geography 2) Economy 3) Demographic pattern -who settles there, what customs did they bring with them? 4) Perceived distance from the center -distance from decision making area 5) Perceived or real dependence on the state

Inducement for the Maritimes to join Confederation:

-the promise of railways to capture the Canadian market, that induced that area to join confederation -the expulsion of the Acadians was the founding/formative event for the Maritimes (Weisman) because it ensured that there would not be a dual future for both languages in NS and PEI -NB was an exception, because the Acadians escaped to New England -outside NB, there was a more “elite”, “conservative” culture -the American Revolution helped populate the Maritimes -and the region was more liberal than Newfoundland, but the Maritimes did not have the other formative event that took place in upper and lower Canada (rebellions in late 1830s)

-Newfoundland was rattled by political scandals -they couldn’t turn to Ottawa, so they turned towards the British government -1949 was Newfoundland’s founding event

Louis Hart’s Fragment Theory

-Hart’s idea that the politics of new societies are shaped by the older societies from which they originated

-the 19th century belonged to the Conservatives -Laurier proclaimed that the 20th century would belong to Canada (not the case…but he probably meant the Liberal Party)

Manitoba’s Fragments

-Manitoba’s founding moments were the Riel rebellion and the completion of the CPR -Winnipeg General Strike

Saskatchewan’s Fragments

-Saskatchewan’s formative event was both the CPR and the squashing of the rebellion and hanging of Riel -Saskatchewan’s boom/bust cycle, in addition to its one crop dependency (wheat) -this led to more cooperatives in the province (and the founding of CCF)

Alberta’s Fragments

-Alberta’s formative event is the “last best west”…end of the new frontier -Alberta found itself with a lot of Nebraskans, Dakotans, etc -this led to the UFA (united farmers of Alberta) -the importation of ideas from the USA (monetary reform, and issues of direct democracy) -emergence of oil wealth in the late 1940s

BC’s Fragments

-British Columbia’s formative event has to do with it’s distance from the center -the founding event is the “last spike” for the CPR

Hartz:

-Gad Horowitz elaborated Hartz’ theory into a Canadian model -Canada’s relative flirtation with social democracy and America’s fanatical rejection of it, was connected to Canada’s ideological diversity, tolerance, and toryism -from a Hartz’ian perspective, Canada had dual cultural fragments -the older society is rooted in pre-revolutionary, pre-liberal France -the second, and newer, English Canadian fragment rejected and fled the American Revolution but was infected with a rationalist, egalitarian ideology -contradictions: -social democracy has been strongest where toryism is the weakest -the inverse is true as well -the Hartz/Horowitz theory is the truest in Alberta

-in 1995, Ontario, BC, Saskatchewan, and Quebec…there were provincial governments that called themselves Social Democrat

-Canadian provincial culture has been affected by waves of immigration -eastern Europe (working class) -they shared the more social democratic expression

How strong is the sense of attachment to a Province vs. Canada? -PEI has the strongest sense of attachment to Canada -NS is second -Quebec has 35% support for attachment to Canada

-Newfoundland has the strongest attachment to their province -then comes Quebec and Alberta

-the sense of belonging to Canada, by age group -15-35yrs, 45% feel attached to Canada -35-64yrs, 53% feel attached to Canada -65+yrs had almost 70% attachment to Canada

Culture of Democracy:

-sum total of political values, beliefs, attitudes, orientations, and opinions of people of a given province

-how do we measure changes in political culture? -historical evolution -founding events -democracy -voter turnout -other forms of political participation

-1963 study by Eomen and Verba -3 types of political culture 1) A parochial political culture -citizens are unaware of the political system which they are part of 2) Subject political culture -citizens are aware of the political system -they inform themselves about its operations -they realize that it has an impact on their lives, but they do little to influence it 3) Participant political culture -citizens are aware of the political system -actively attempt to influence it -generally, Canadians are “participant” political culture, although the argument for both parochial and subject political culture can be true -to what extent is low voter turnout compared to what is known

-Nowell (clientelism) -practice of patronage 1) (Associated with pre-confederation period) local official and his clients offer political support in return for individual favors (such as government jobs) 2) (Post-confederation to WWII) emergence of political parties -relationships between the elected official and the client, becomes less personal because of the involvement of political brokers or intermediaries -with the emergence of the parties, government jobs and contract were awarded on a partisan basis -the party emerges as the patron 3) (Post WWII, expanding government activity) -patronage could no longer be relied upon as a basis for staffing the public service -the patron-client relationship became bureaucratized -the bureaucracy emerged as the patron, at the expense of the political official or party because the bureaucracy had the discretion to license, regulate, and distribute massive amounts of public funds through grants, concessions, and incentives -there is a struggle between the bureaucracy and the elected officials

Political Parties

-how many, and what type of parties make up the system? -2, 3, or multi-party system -One party dominance occurs when parts are NOT evenly matched, and do not alternate frequently in power -Two party system occurs when two parties capture the bulk of the vote between them -three party system occurs when three parties capture 20-25% of the vote -two plus system is where the third party results in 10-15% of the vote -concentrate on the origins of the party

John Wilson

-influence of social class to the evolution of the party system -after 1900, the Liberals and Conservatives were the two main parties, but they had to contend with the newly franchised working class

-agricultureism, anti-stateism, and clericalism were the three modes of thinking during the pre-1960s Quebec

-in political systems where the emerging working class had a greater impact, one of two party systems emerged 1) CCF (cooperative commonwealth federation) 2) The modification of the established parties, to respond to the newly established working class

-in related class ideology to party support, there are two thoughts in political science -looks at the extent to which ideology motivates political activity -the degree of ideological difference between parties -once in power, all parties are reasonable similar and are influenced by the corporate elites -the system’s structure is such that the party has to have a broker to respond to the diverse Canadian constituencies -another school finds a slight difference of approach at the federal level, but a significant variation at the provincial level -e.g. unlike the federal level, there are NDP govs at the provincial level -the Liberal party has two main factions (business and reform group) -traditionally the Conservatives are composed of a higher share of Business Liberals, they are generally more to the right of Liberals of individualism and inequality…but it is the progressive wing of the party that has moved it away from the right

-are ideological differences reflected in provincial government policies?

Province by Province

Newfoundland

-1974-1975 voter turnout was 57% for federal election and 73% provincially -1993 voter turnouts was 55% federally, and provincial turnout was 86% -from 1949-72, Joey Smallwood (Liberal)…1972-1989 the Conservatives dominated Newfoundland politics

PEI

-1972 turnout was 80% in both federal and provincial -1993 turnout in federal was

Nova Scotia

-greater provincial participation in the early 1970s -1980s it reverted to be more federally -recently, provincial participation is greater

New Brunswick

-consistent of 10% difference between provincial and federal turnout, in favor of the province

Quebec

-15% gap between federal and provincial participation….in favor of the province -Quebecers believe that 51% of issues of greatest importance are provincial, but only 25% say that federal government

Ontario

-participate in federal more than provincial elections

Manitoba

-55% of Manitobans argue that the federal government represents the issues of greatest importance -1970s, greater participation in provincial rather than federal -now, participation in each is equal

Saskatchewan

-participation provincially is greater than federal (10-15% gap)

Alberta

-higher participation federally rather than provincially, but they view the greatest issues of importance to be in the province

British Columbia

-70s larger participation in federal -recently, greater participation in provincial rather than federal -1975-91 Social Credit -1991- NDP -Liberals elected in

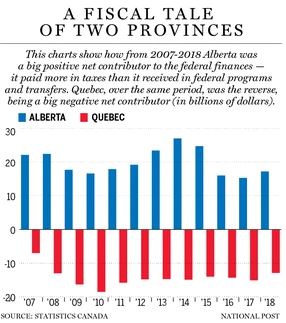

The Fiscal Imbalance

Fiscal Imbalance in Canada (Seguin Report) http://www.desequilibrefiscal.gouv.qc.ca/en/pdf/historique_en.pdf Department of Finance, Government of Canada ‘The Fiscal Balance in Canada’, October 2004 www.fin.gc.ca/facts/fbcfacts9_e.html

Fiscal Imbalance:

-vertical and horizontal fiscal imbalance -vertical -flows top down -most FI deals with vertical FI -horizontal -between the provinces themselves -Alberta vs. NS -fiscal imbalance arises out of the following 1) If the fiscal gap between provinces own source revenue and their direct spending is too great -because such a differences threatens to subordinate the provinces in relation to the federal government -traditionally, this has been solved through transfers from the federal to provincial government -when the transfers are insufficient to offset the own source revenue of the province to meet its responsibilities, then there is an imbalance 2) Even if the final balance is zero (the transfers offset the gap), an imbalance can still exist if the economy of the province is impaired 3) Can exist when the federal government evokes a spending power to intervene within the province’s field of jurisdiction -insodoing, it has a direct influence on the level of provincial government spending

how to satisfy these problems to create a fiscal balance

1) sources of own source revenue are allocated to each government that allow an equitable division of tax deals committing sufficient financing and accountability in the respective field of jurisdiction within each province -money provided for certain tasks or department -Tremblay Commissions under Duplessi -began based on transfers to universities -in a federal state, the constituent parties must obtain through taxation the needed financial resources to exercise their respective powers 2) Total revenue plus own source revenue plus transfers must enable each order of government to effectively cover its expenditures…but without conditions that may impair its economy 3) Transfers from the fed government to the provinces should not limit the decision making and budgetary decision of the provinces UNLESS the members of the federation have validly agreed to conditional transfers

Regionalism and Asymmetry in the Canadian Federalism

Robin Boadway, ‘Should the Canadian Federation be Rebalanced?’ 2004 http://www.iigr.ca/pdf/publications/343_Should_the_Canadian_Fede.pdf

Kathy L. Brock ‘Accords and Disdord: The Politics of Asymmetrical Federalism and Intergovernmental Relations’ http://www.iigr.ca/__site/iigr/__files/gogoPage/brock%20working%20paper.pdf

Guest lecture from Marc-Andre Bachard active in the Quebec Liberal party (President)

-after the 1995 referendum, he became interested in active politics -Harper may have a tough time delivering his asymmetrical federalism because Ottawa’s civil servants wont tend towards decentralization

Liberal Party of Quebec:

-has the best electoral machine in the country -the party started before confederation -the conservative party disappeared in 1936 and became the Union Nationale until 1960 (in power), but maintained influence until 1970 -1970, the PQ received its first members elected to the NA -it has always been Liberals leaving their party and creating something else (both Union Nationale and the PQ and the ADQ) -there are two forms of political allegiance – the coulonde rouge and the coulone bleau -the values of the Liberal party are based on the idea of “the power of the individual” -the progress of the individual and of society -in the PQ, you will not find anything about the notion of the individual -since the 1960s, the Quebec Liberal party has become socially just

-the relation between the notion of the fiscal imbalance and that of asymmetry -one view is that asymmetrical federalism is a good way to keep the federation together -Cathy Brock – too much asymmetry will not be good -where is the accountability if the federal government is distributing the funds -once you begin to enter into asymmetrical arrangements, this leads to other provinces wanting the same thing -is there a relationship between fiscal imbalance and asymmetry? -there is an imbalance in the federal-provincial transfer, therefore it can be helped/fixed through asymmetry -asymmetry is the unequal treatment of unequals -fiscal imbalance is the equal treatment of unequals

-principle of equality is a continued feature of our federation remaining unified -on the other hand, some provisions of the constitution apply only to one or two provinces -certainly the provinces are NOT equal because they are not equally represented in national government institutions -does it matter that the jurisdictional equality that supports the equal provinces idea is more formal than real? -a few other questions are raised -does it matter with the assistance of resources being generated outside provincial boundaries, that some provinces will find it difficult to exercise the legislative responsibility in a manner similar to that of the other provinces -another important questions -is the economic inequality that coincides with the jurisdictional equality a serious threat to the equal provinces idea/doctrine

-jurisdictional equality -flexible federalism (asymmetry in different terms) -trying to figure out how to represent or empower local government within the institution of the federation -is there a definable limit to asymmetry?

Part II: Provincial Political Profiles

Benoit Pelletier Quebec’s Place in Canada of the Future

Luc Bernier, “Quebec at the end of the 1990s” [BROWNSEY & HOWLETT]

Fiscal Imbalance

-there is some sort of fiscal imbalance, but what is it attributed to? -is it built into the system? exam question-how does asymmetrical federalism play into the fiscal imbalance?

-parting thoughts: -Harvey Lazar (former head of the Institute of Intergovernmental Affairs) -Canadians are not fully aware of the natural of sparing between fed government and provinces -we need to educate Canadians about asymmetrical federalism and the fiscal imbalance -provincial governments and local governments have raised about 55% of total government revenues for the last 25 years -they account for 67% of total government spending -today there appears to be more support for a vertical fiscal imbalance, where the federal government has an easier time meeting its financial requirements than the provinces -almost all federations have some sort of fiscal gap -if the fed government decided the threats to Canadian security requires greater amounts for defense, security, and aid, and these amounts were added to federal expenditures, than the debate about the vertical nature of the fiscal imbalance would shift as federal surpluses would likely erode -Canadians need to be persuaded where their priorities should be -as Ottawa tends to consider further transfers for healthcare or childcare to the provinces, it reinforces the notion that the priorities are at the provincial level and it indirectly lends support to the idea that the imbalance is the fault of the federal government (self-fulfilling prophecy) -Jennifer Smith argues: to compensate for provincial imbalances, the fed government tries to maintain a balance between the constituent partners

Benoit Pelletier Quebec’s Place in Canada of the Future

Luc Bernier, “Quebec at the end of the 1990s” [BROWNSEY & HOWLETT]

Quebec

-there are many different expressions of nationalism within Quebec -three dominate forms of Quebec nationalism: 1) anti-stateism 2) agriculturalism 3) religious/clerical attachment -three periods of this nationalism: 1) Anti-government nationalism of Maurice Duplessis and his Union Nationale -a union of the conservatives and action nationale 2) The state based nationalism of “the province building era” of 1960-1980 3) A market based nationalism 1980s-today

Duplessis

-known as “Le Chef” -Charismatic leadership led to a conservative ideology of the time -the state revolved around Duplessis -Conrad Black wrote a biography of Duplessis and almost “rehabilitated” the tarnished image of Duplessis -it is argued that from 1897-1936, under Liberal premiership, the reign of Duplessis was not that different -ruled with support from rural Quebec -1897, 77% of Quebec’s population was rural -by 1951, only 33% of population was rural -the electoral map was largely in a rural context -with the demographic shift, the electoral map didn’t change much -during the Duplessis period, there was an anti-communist and anti-labour feeling in the province -economy was very prosperous -Duplessis tried to support conditions for substantial investment in foreign capital in Quebec -he did this by establishing close ties with the business community -he had support from mainstream media -both French and English media -also had close ties with the Catholic Church -he relied on the relationship with the church to preach class harmony over militants -he quashed labour unrest during 3 occasions -1949 aspects strike (Trudeau was a lawyer involved) -1952 in Louisville -1957 Murdochville -to maintain low taxes, he resisted demands for increased expenditures on health, education and social services -the clergy was heavily involved in the distribution of these services -this contributed to the Quiet Revolution when these expenditures were increased -roads and highways were the largest expenditures in Quebec (attributed to the transformation between rural to urban) -contracts were awarded in highly partisan ways

Jean Lesage

-Jean Lesage became PM in 1960 -Rene Levesque was part of this -this is the beginning of what is looked back on as the “Quiet Revolution” -he wanted a “catching up of priorities” for Quebec -a cultural affairs ministry was created -the civil service was expanded -a report was created to determine if there should be a ministry of education (it was subsequently created in 1964) -a federal/provincial relations department was created in 1961 -the SGF was created (aimed at supporting entrepreneurial initiatives) -the caisee du depot was created in 1965, looking to support the francophone entrepreneurial class -hoping to decrease the inequity between English and French Quebeckers -the 1962 provincial election was based on nationalizing the Hydro industry -prior to this, the Montreal Lighting and Power owned all this -Rene Levesque was responsible for the nationalization

-the concept of modernization, and improving the inequality within the province (modernization and “catching up”/raportage)

-the election of Lesage was largely Montréal (English speaking) supported -on one hand, for the liberals, the minority vote is a secure base of support (from WWII tiill today…with one exception…1989) -this vote has been taken for granted by the liberals

-1962, the Liberals go to the electorate around Hydro issue, and they win -majority diminished slightly -at this time, the federal government is beginning to look at the condition of the French-Canadian position and its demographic position within Canada -the declining birthrate of the population -the economic gaps and inequities -overall, there is a Canadian concern for the diminishing role of French Canadians -a transfer of responsibility between the clergy and the middle class elite of Quebec -this is a willing transfer, because the clergy does not have the ability to support the needs of the residents of Quebec -the federal government feels a need to step into this debate -they create the Royal Commission on Bilingualism and Biculturalism -this commission (proposed by Pearson)…the RCBB’s purpose was to develop an “equal partnership” between the two founding peoples -this didn’t take into account the various other ethnic groups -as this commission was taking place, the government addressed the problem of the inequity between the English and the French

-3 approaches that arose from the RCBB 1) Inclusion -bringing more French speakers into the decision making apparatus federally -this apparatus was under a time of expansion anyways 2) Recognition -recognizing the distinctive features and characteristics of Quebec -this was the initial recognition of the recognition of a French Canada (not necessarily French Quebec, but French Canada) 3) Devolution of Powers -transfer of greater power or responsibility onto Quebec

-the flip side from a Quebec point of view (of the three points) -the issue of affirmation -independent of the fed government’s strategies that it adopts for the issue, Quebec will develop strategies of affirmation on its own -this affirmation will range from things that occurred during the Quiet Revolution, to outright sovereignty

-Quebec is still torn between the fast movement of reform and change from the 1960s, and the continued sense that it is moving too far and too fast

-in 1966 there was a provincial election, and Lesage campaigned on continued reform -communications ministry was created in the 2yrs previous to the election to deal with the French language issue -a department of immigration also began to be created -there was new electoral boundaries drawn up for the ’66 election (11 new seats were created in Montreal) -the public service grew by 42% between 1960-1966 -in the mid-sixties, two small parties emerged advocating for the breakup of Canada -RIN (more socially left) -RN (more right wing)

-1966 the Liberals lost the election -Daniel Johnson Sr. won for the Union Nationale -56 seats for Union, and 50 seats for Liberals (Liberals had 48% of the vote, and the Union had 41%) -Johnson understood the nationalist sentiment

-Johnson had to deal with the issue of language

McGill University – Provincial Politics class these notes are from in 2006 | Guest Lecture: Stephane Dion

1) Canada’s provinces have a lot of power 2) The number of “provinces” in relation to other federal states, is relatively low 3) The provinces are weak within Ottawa. Canada does not have a Senate (in terms of a Chamber of provinces) 4) Strong executives 5) Existence of a minority that is a majority in one province

McGill University – Provincial Politics class these notes are from in 2006 | Guest Lecture: Boisclair

-Boisclair guest lecture

-Québec does politics democratically -the referendum was lost by 50,000 votes, but not a single drop of blood was shed

-sovereignty must come from a referendum, not an election -Boisclair is a democrat before being a sovereigntist

-what is sovereignty? -a protection of culture -identity 1) Capacity of Québec government to vote for its own laws 2) Québec should receive all taxes 3) Québec has an international existence

-why does Québec feel like it should separate but this feeling is not the same in other provinces? -because Québec is a nation -National Assembly -National… -the Canadian constitution states the two founding nations -Québec is already a nation

-when Charest asks Harper for more control for the “nation of Québec”

-why does Québec want to be its own separate nation? -the quiet revolution provided things for Québec that weren’t available before -because they want to continue to exist as a francophone in the context of North America

-the reasons for sovereignty today are not the same as they used to be -Boisclair’s father was not treated well/properly because he was a francophone -this is not the case anymore

Provincial Profiles: British Columbia and Alberta

Michael Howlett and Keith Brownsey, “Politics in a Post-Staples Political Economy” [BROWNSEY & HOWLETT] Peter J. Smith, “From Social Credit to the Klein Revolution” [BROWNSEY & HOWLETT]

Phil Resnick. The Two British Columbias www.iigr.ca/pdf/publications/136_the_two_British_Columbia.pdf

Peter Stotland

-he began in Medicine hat -covered the Loughheed government in the late ‘80s -then covered Western issues from Ottawa -came back to Alberta for the “Kleinilution” -will give his position as an observer, standing outside the political process

-Alberta was governed by social credit from 1935-197? -then PC under lougheed from 197? Until present day

Social credit

-Manning -Harry strong -Lougheed

PC

-Lougheed -Ghetty -Ralph

-with the three leaders of the PC, you have three very different leadership styles -almost different parties, except by name -within the one party, there are different differentiations -Alberta’s provincial politics are the least ideological than anything else in Canada -it’s more about brand loyalty -when Lougheed was putting the conservative party back together, he was looking for a brand that meant credibility -he didn’t care what they called it ideologically, but it was important to know what it meant -what matters in Alberta, is what works….pragmatic management -the only government that began to dabble in ideological thoughts, it was a disaster -the “kleinilution” is nothing like a neo-con agenda…it was a new brand that was needed that was pragmatic and worked -in 1995, Klein was on a trade mission in the middle east, and Preston Manning had mentioned that he was interested in creating a provincial wing in Alberta to challenge Ralph’s lack of ideological thought -Ralph never countered this ideologicalness

-Albertans are not interested in political parties, they want pragmatism that works

-in Alberta politics, you give the people back what they will believe is there’s -do what people want from you

-politics is divided into three regions -rural -pragmatic ideas -we need roads, hospitals, necessities of life -Calgary -a force for political homogenization -a suburb city -there is a force that makes people accept and get along by going along -Edmonton -far more of a “folksy”, “artsy” type of city -the UofA is a more dominant force than UofC is in Calgary -the UofA is part of the metro-Edmonton area -Calgary is the city of money -the city of head offices -Edmonton is the city of workers (blue collar)

-4 leaders since 75 -William Aberhart -Ernest manning -Peter Lougheed -Ralph Klein

-quasi-party system, due to the near one party dominance -the liberals were strongly associated with immigration, so liberals often received the immigrant vote -Alberta in 1905 was liberal, because of the immigrants

-the emergence of social credit -because the UFA were ineffective in combating the effects of the depression -the “show me the money” party -1941 the industrial workers outnumbered the farmers -the overthrow of SC was due to the urbanization, secularization, and geographic mobility -changes in Alberta coincided with changes elsewhere -under the Mulroney regime, we saw the elimination of the NEP (National Energy Program) -there was more attention paid to agriculture -pursuit of free trade -Don Ghetty pressed for the elected senate -Ralph Klein took power of the Alberta PCs, but federally, the PCs lost power

-on federal-provincial relations, Alberta has been relatively calm

-sources of division -Medicare -cutback in shared cost programs

-more recent federal Alberta issues: -reforming fiscal arrangements -the desire for greater flexibility for personal income tax -reducing overlap and duplication -notably in energy, agriculture, economic development, labour market policy, and the environment -minority language education, petroleum industry, grain transportation,

-the three dominate issues between Alberta and federal government: -health care -environment -oil wealth / equalization

-positive net migration -endless opportunities, but these opportunities are limited by the federal government

McGill University – Provincial Politics class these notes are from in 2006 | Guest Lecturer – John Parizella

John Parizella speaking -director of Quebec Liberal Party (20yrs ago) -chief of staff to Robert Bourassa -talking on federal-provincial relations theme -he’s worked 18 provincial campaigns -2 federal elections -ran in 1985 in Mercier and lost by 1100 votes -worked with Bourassa for 9yrs…lived through Meech, Charlottetown, Bourassa’s cancer -he is a practician

-why don’t we hear of “American federalism”? -Canadian characterize our country as federal vs. provincial governments -federalism won as a concession to Quebec to allow each province the ability to handle their own issues -BNA Act -Article 91 -powers of federal government -peace, order, and good government (residual clause) -Article 92 -powers of provincial government Article 93 -education in Quebec -two kinds of periods of federal-provincial relations -periods of centralization -periods of decentralization -this has mostly come from the courts

-are we in a period of centralization or decentralization? -for the last 4 yrs, we have been in a decentralization period -the administrative powers of jurisdiction have often favored the provinces (especially Quebec) -the BNA Act looks like a centralizing constitution, but in practice, it has worked towards the provinces

-administrative arrangements -Health Care deal 2004 -Day Care deal -federal-provincial relations cannot just be looked at constitutionally, it has to be looked at from an administrative viewpoint -this is done with by the premiers or the civil service -there is a lot going on between federal and provincial government on a daily occurrence

-the process of the relationship is looked at in two ways -informal -deals with chief of staff to Mulroney on a daily basis during Meech Lake -formal -the last meeting to try and kickstart the accord…the meeting was supposed to last 3 days, but lasted a week

-diplomacy -usually associated with IR -an emerging term, because we cannot wait for a meeting with cameras, the relationship occurs everyday -domestic diplomacy -the premiers have to talk to each other, and to the fed government, and vice-versa -this has to occur with respect and with the notion of dialogue

-institutions that govern federal-provincial relations -conferences -dinners at 24 Sussex with all the premiers -or they have a formal meeting with each premier having their staff with them -they used to meet every year -but they now meet based on issues as they need it -Council of the Federation -Charest’s initiative -all 10 premiers meet and hammer out an agenda that works to build a consensus to defend the province’s jurisdiction -this can lead to a formal federal-provincial conference -gives the provinces the ability to get their act together and speak with a united voice

-what are the subject matters that dominate federal-provincial relations? -economic union -although we have free trade, there is little free trade between the provinces (it is often north-south free trade rather than east-west) -how can we ensure the economic sustainability of the federation -social union -healthcare -the provinces are responsible for deliver of service -41% of Quebec’s budget is spent on health care -education -the feds have a role in research -but managing education (building, programs, professors, K-12) all managed by provincial governments -fiscal -all premiers agree that there is more cash in Ottawa than in the provinces -political union -often constitutional -the appetite isn’t big for this type of discussion because it usually ends in failure (Meech and Charlottetown) -equalization -British Columbia, Alberta, Saskatchewan, Ontario give into equalization – Atlantic, Quebec, Manitoba receive

-the question of Quebec -perspectives -the West -always felt alienated and never quite felt comfortable in the federation (NEP) -Reform came about to advocate the West’s interests (couldn’t become a national party because of its strong western views) -Ontario -seen as the fat cat in Canada -Maritimes -receives a lot of equalization -Quebec -the tail that wags the dog -why is Quebec so complicated? -book by Andre Pratt that shows the myths around the relationship between the fed and provincial governments (he is federalist)

-three thoughts in Quebec -Trudeau vision of federalism -he came to power saying that Quebec had to play a role by expanding the presence of French beyond the borders of Quebec and to become involved in power -more centralized -renewed federalism -believed that we can change the federation to work better and respect the differences in the country -make the west feel welcome -and make Quebec feel involved -sovereignty -hard liners -Jacques Parizeau -Quebec must become a country -soft liners -Rene Levesque -need an association -sovereignty (hyphen) -the sovereigntists argue, but they do it internally, and at the right times

-governing with Quebec is tough -Quebec will work for a deal, and if they get it, they want more -Trudeau federalists don’t have a bright future (dying breed) -Quebec fed Trudeau, and Trudeau fed Quebec (they needed each other) -Trudeau’s vision needed to continue with Trudeau, because he was one of their own -he was SO unique, and one of a kind

BC

-1867 there wasn’t much discussion of British Columbia joining confederation -in 1871, a number of factors led BC to join Canada (a means of debt relief) -25 member assembly in BC -government was administered by a shifting combination of factions, and patronage oriented politics -1871-1875 the national railroad dominated the political discussions -in the 1870s, the country was hit with a depression/recession -the railway was not completed on schedule -1876 a petition was circulated which raised the idea of BC seceding from Canada because there was no railway completion -progress with railway construction in the coming years -lots of Chinese labour brought in to work on the railways -November 1885 was the last spike for building the railway -the CPR completion was a major boost to the economy and created a political environment dominated by merchants, lawyers, industrialists, and landowners -timber and mining rights were widely distributed -immigration was relatively high for that period -Vancouver developed as an important port for Canada (especially in the lumber export area) -the employment of Chinese labour was a contentious issue -this led to the establishment of labour representatives -by the turn of the century, marked by social tension and unrest as labour became increasingly organized -fishing and mining sectors had considerable strike activity -substantial anti-oriental sentiment among the workers -the province became a “hotbed” of militant unionism -laws were passed prohibiting Orientals from working in the mining area, denying them franchise, and federal action was demanded to restrict Chinese/Japanese immigration -this 20th century period, (of political instability), set the stage for the emergence of party politics in the province -factors contributing to this development -the need for political cohesion -the growing isolation of communities -the business community wanting a stable investment climate -the federal parties wanted to have solid provincial branches of their parties -as party lines solidified, Conservative leader was called upon to form the government in 1903 (Richard McBride) -this began a 12 year rule under McBride during a period of strong economic growth

-3 general platform ideas: 1) Railway development 2) Better terms from Ottawa 3) Exclusion of Asians -McBride’s government was persistent in passing anti-Oriental legislation, which was either disallowed by Ottawa or overturned by the Lieutenant Governor -although McBride encouraged a fast expansion of the provinces resources, there was legislation brought in to protect timber and water resources -there were also some measures to improve the condition of the working class, and to protect public health -new schools were built, and provincial archives, and the university of British Columbia -so by the 1912 election, the socialist party (opposition) elected 2 candidates and the Conservatives won 40

-the economy began to boom by the late 1920s -several pieces of social legislation was introduced 1) Extending minimum wage laws 2) Workman’s compensation 3) Industrial disputes Act -Premier John Oliver had through the 1920s successfully challenged the federal government over railway freight rates and liquor legislation -a plebiscite determined that the people preferred government regulation than prohibition -1920s also a period of significant construction -roads and bridges being built -all good things must come to an end

-with the depression of 1929, most provincial industries collapsed -the Conservative Premier Simon Tolmy??? Had difficulty rebuilding the economy -because of BC’s mild climate, it attracted immigration from other provinces, and had to establish relief camps to alleviate the large influx of people -the government was charged with corruption -under great stress, the Conservatives approached the Liberals (lef by Duff Petulow?) with the offer of a coalition government -but the Liberals were on track electorally, and refused the offer and waited for the 1933 election -the Liberals improved their lot and came to power with 34/47 seats -this election also marked the appearance of the CCF which attempted to unite the divided factions on the left -Petulow was running a centrist party and ran on the slogan of “Work and Wages” and presented what some referred to as the “Little New Deal” -described his approach as “practical idealism” compared to the “visionary socialism of the CFF” -the first of the radical premiers of the 1930s with a focus on progressive liberalism -rather than cut public expenditures during the depression, Petulow had the government increase purchasing power through job creation and private sector subsidies -but as federal finaicinial support for this approach didn’t materialize (even though there was a Liberal in Ottawa, PM King, and in BC) in the mid-1930s, and Petulow began advocating provincial rights -in the face of widespread strikes, high unemployment, and growing debts, Petulow increased relief efforts, raised minimum wage, limited work hours, and offered financial aid to the troubled fishing and mining industries -by the late 1930s, the economic situation began to improve -Petulow then focused on northern development in the search for oil -he also looked at annexing the Yukon

-1937-1941 Petulow embarked on “socialized capitalism” -centered on government regulation -also became obsessed with the idea of provincial rights -in response to the improved economy, the federal government closed relief camps in 1938 and the province then decided to cut off relief to the unemployed people from the Prairies (those who migrated into BC) -this resulted in demonstrations in Vancouver -property damage and injury occurred as people were aksed to evacuate -some criticized Petulow for his quarrel with Ottawa going too far -in reaction, Petulow join William Aberhart and Mitch Hepburn (Ontario) in opposing federal review of the provincial-federal distribution of powers under the Robert *** Commission -but the provincial right strategy lost favor with British Columbians after the outbreak of WWII -Petulow’s party and the electoral became dissatisfied with his leadership -he also began losing support from both the left and right as his middle ground became untenable -by Oct 1941, the Liberals were reduced to 21 seats, CCF 14 seats, and the Conservatives 12 seats -the CCF has the largest plurality of the popular vote -there was a strong sentiment for a coalition government -Petulow rejected the idea of a coalition government, because the ideological differences between them all were too important, therefore no basis for inter-party cooperation -but there was pressure from business class, and Liberal/Conservative politicians -so in December of 1941, a Liberal resolution endorsed the idea of a coalition government which forced Petulow out -John Hart became the new leader of the Liberals, and also the leader of the Liberal/Conservative coalition government

1941-1945 was dominated by national and international events and decision making -the domestic (provincial) scene was reduced in importance -the most controversial issue was the uprooting and interment of the Japanese community -the federal government removed 20,000 Japanese Canadians from the West Coast -confiscated the property of many of them -and dispersed them across the country, or deported them -this was all occurring during periods of economic prosperity

-1944 BC Federation of Labour formed -this benefited the CCF to some extent (with the growth of labour), but the presence of the communist leadership in the CCF provided political ammunition to the coalition government against the CCF -the Liberals/Conservatives were forming together in the election of 1945 to fight the CCF

-the post-war period economy was prosperous, and the CCF continued to encounter some difficulties -some was connected to international cold war tension -late 1940s, the Social Credit party was building support -in the 1949 election, the Liberal/Conservative coalition was returned with 39 seats, and the CCF reduced to 7 seats -the early 1950s, witnessed the disintegration of the Liberal/Conservative coalition and the growth of Social Credit -the catalyst for the demise, was the new hospital insurance scheme that went into effect in 1949 -the Conservatives insisted on high premiums and daily user fees -the Liberals wanted to operate the plan out of general revenue -the Liberals in the midst of all this called an election in 1952, and anticipating the breakup of the coalition, introduced a new electoral system (the preferential system) -ranking the candidates in order or preference -instead of voting with a single x, you rank your numerical preferences -the logic is…even though the Liberal and Conservatives were no longer partners, they preferred each other than the CCF, so the Libs could rank Conservatives second and vise versa -a mistaken assumption, as the supporters of each coalition party, opted for Social Credit as their second choice -a fresh, but safe private enterprise alternative to block the CCF -even the CCF supporters ranked the Social Credit second -the results were19 seats for Social Credit, 18 seats for CCF, 8 for Liberals, 4 for Conservatives -the leader of the Social Credit (W A C Bennett) formed the government -an honest man -he disavowed the original Social Credit idea (money printing) and operated with a modern Conservative approach -obsessed with the growth and development of the provinces abundant natural resources -especially sensitive to the needs of Interior communities -he used the natural wealth of the province, and his own dominate leadership style, and a good read of public opinion to provide stability for government in British Columbia -this resulted in a string of Social Credit majorities -3yr intervals (one 4yr interval) from 1953-1969 -strong share of popular vote in each instance -“progress, not politics” was the Social Credit slogan in the 19** election -the electoral system also returned to the original system -the Social Credits being approved by all classes of society, especially the middle class

-the mid 1960s saw considerable economic growth (continued growth) in the province -notably in the pulp and paper industry -the government abolished bridge and road tolls -introduced a partial medicare plan -fought with Ottawa over the reluctance to establish the Bank of British Columbia -all good parties must suffer at some point, and in the late 1960s, economic problems emerged, forcing the government to introduce an austerity program -lay offs and strikes occurred -and an increase in confrontations between government and organized labour -Ottawa finally approved the Bank of British Columbia on the condition that there would be no provincial government involvement

-1970s had the collapse of the Bennett regime -an election of the first NDP government in the province

McGill University – Provincial Politics class these notes are from in 2006 | Guest Lecturer Professor Antonia Maioni

Healthcare and Provinces in Canada

1) Jurisdictional responsibility vs. fiscal capacity -there is a myth that there is a “Medicare system” in Canada -but there are actually 10 unique systems across the country -Canada Health Act is a federal statute that sets the rules for the money that Ottawa sends the provinces -the provinces are each governed by their own individual healthcare legislation

-division of powers (1867) -healthcare is a prime example that wasn’t important in 1867, but is very important now -Section 92(7) healthcare is a provincial jurisdiction -however, the federal government has carved out a space for itself in the healthcare system -the federal government controls the money, so it plays a role -how much does the federal government spend on healthcare -the provinces say that the federal government spends 15-18% on healthcare -but the federal government believe they spend 25% -provincially, healthcare is eating up 35-45% of the provincial budget -this percentage is rising

2) Historical development of healthcare systems -provincial innovation vs. federal diffusion -the CCF in Saskatchewan, led by Tommy Douglas, came to power in 1944 on the platform of providing medical services for all citizens -he realized that the idea of healthcare for all wasn’t supported by all -doctors needed to be convinced -hospital public insurance began in 1947, in order to pay the doctors directly, but patients wouldn’t need to pay for their stay at the hospital -this program became popular in other provinces -Ontario (Conservative government) took the example from Saskatchewan and thought about also implementing hospital insurance -the Ontario premier wanted to bring the federal government in to help implement this expensive program -in 1957 the federal government passed the Hospital Insurance D S Act to help pay almost half of the cost of hospital insurance -the provinces quickly signed on -by 1961 the provinces had legislation in place in order to receive the money from the federal government -the hospital insurance program freed up money for Tommy Douglas to introduce public medical insurance in 1961 -physicians went on strike in 1962 in Saskatchewan to protest these new measures -to end the strike, the provinces conceded that doctors would be reimbursed by the provinces and would retain their autonomy as professionals (they could bill for every service, they could have their own clinics, etc) -Canada doesn’t have salary doctors….they bill for what they do -1962 the first public medical insurance program inaugurated in Saskatchewan -the question was when the domino effect would hit the rest of Canada -the federal government in 1962 was on shaky ground, so Diefenbaker called a Royal Commission on Healthcare (the Emit Hall Commission) -this commission ruled that all provinces should have similar medical systems to Saskatchewan -this report was presented in 1964 to the Pearson government -the 1960s in Canada was ideologically polarized -Alberta (Ernest Manning under Social Credit) had different ideas -Manning Care -voluntary insurance systems using private insurance -Manning was eventually trumped by the federal government’s fiscal capacity -in 1966, the federal government passed the Medical Care Act as a cost sharing program -for all provinces that set up a system similar to Saskatchewan, the federal government will reimburse for 50% of every dollar spent by the province on the health system -by 1971, every province had a medical system like Saskatchewan’s in place -for both public medical insurance and public hospital insurance

-in 1977 the federal government decided to change the way which they send money to the provinces -Established Programs Financing Act came in to place -instead of receiving the health bill from the provinces and reimbursing the provinces 50%, the federal government would provide a block sum of money to the provinces -this meant that Canada would no longer be on the hook for the rising costs of the healthcare system -all overruns would have to be covered by the provinces

-in 1984, Trudeau passed the Canada Health Act which would include 5 principles -if a province transgressed on any of these prinvicples, the health minister would cut funding to the provinces -the provinces NEED the federal funding -the five principles: 1) Public Administration -money to pay for doctors and hospitals had to go through the provincial treasury -public payment -accountability for the money 2) Universal -100% of residents of a province were covered and eligible for health insurance 3) Comprehensive -all medically necessary services had to be covered under provincial health systems -what is deemed medically necessary? 4) Portable -a citizen in Moose Jaw that moved to Montréal must be covered -their coverage is portable across the country 5) Equal Access -the most controversial -healthcare would be provided on equal terms -no cue jumping…everyone is treated the same way -according to need not financial position -1986-87 the Ontario doctors went on strike to protest -the provinces are having a tough time following all these principles but also paying for healthcare -Mulroney began cutting the lump sum of healthcare transfers -1995 Canada Health and Social Transfer -put in place by Finance Minister Martin -all money for social programs that the federal government sent to the provincial government were put together in one lump sum, and this number was reduced -so healthcare, education, welfare, any other social programs one payment -all these federal cuts to the provinces were then passed on to the hospitals (governed by health districts) -the hospitals then have to make significant cuts within their hospitals

-by 2004, federal-provincial relations were in a bad state -the public’s confidence in the public health system was lost

-although the public health model is hugely popular, the system is put under the microscope

3) Financing and basic principles

4) Future challenges -the role of the courts -“private” initiatives in provinces

Chaoulli v Québec

-the Canadian charter was applied to a Québec law that the waiting time infringed on his charter rights -the Supreme Court used the Québec charter to side with the plantiff -the court said that Québec’s ban on private insurance was infringing on individual rights when there is undue waiting time -this has opened up a can of worms…lots of questions -innovations for reform are coming from provincial governments

-Québec’s response to the Supreme Court -allow private insurance for a few services (elective surgery for hip/knee and cataract) -also puts in a waiting time guarantee -if they do not receive their service by a certain time, the patient will go to a private clinic and the public system will pay for it

-Alberta’s Third Way -considering allowing physicians to work in both the public and private health services

-British Columbia is shopping for healthcare models in Europe

Provincial Profiles: Manitoba

Kenneth J McKenzie. “Reflections on the Political Economy of Fiscal Federalism in Canada.” C.D. Howe Institute Working Paper (September 2005).www.cdhowe.org/pdf/workingpaper_4.pdf

Premiers of different administrations: 1878-1887 – Conservatives 1888-1900 – Liberals 1900-1915 – Conservatives 1915-1922 – Liberals 1922-1943 – United Farmers of Manitoba 1943-1958 – Liberal Progressives 1958-1969 – Progressive Conservatives 1969-1977 – New Democrats 1977-1981 – Progressive Conservative 1981-1988 – New Democrats 1988-1999 – Progressive Conservative (Gary Filman) 1999-2006 – New Democrats (Gary Doer)

-initially a small and primitive place (1870) -unlock the other six provinces, it lacked a representative and responsible government -12,000 people lived in Manitoba in 1870 -560 aboriginals -6,000 Metis -4,000 English/Native origin -1,500 white non-aboriginal -there was a slight French majority in the province in 1870 -owned and governed by the Hudson’s Bay Company -had the most violent entry into confederation -Louis Riel formed a provisional government that elected 12 English and 12 French delegates -went to negotiate with Ottawa, but wasn’t recognized for provincial status -within the violent clashes, 3 people (including Thomas Scott) were killed -Orange Order (militant Protestant group) -province established in 1870 and was officially bilingual -guaranteed separate schools system built in to the Manitoba Act -the fed government maintained control of Crown land and natural resources – needed fro the railway -1874 R.A. Davis became Manitoba’s first real Premier -significant immigration (mostly English speaking Ontarians, Mennonites, Icelanders, and some French Canadians) in the 1870s -after 1878 election, John Norquay became Premier (nominally a Conservative) -two main issues: -boundary disputes with Ontario -railway negotiations -by the 1888 election, party labels were still not established (although Thomas Greenway was considered a Liberal) -the English Protestants constituted a clear-cut majority at this point -they sought a makeover of the province -to build Manitoba in the image of Ontario -this brought the issue of bilingualism and separate schools to the forefront -these became the principle issues for Manitoba from 1890-1960s -1890 Manitoba abolished the use of French in the legislature and in the courts -also dismantled the separate school system -both things were established in the Manitoba Act -however the Manitoban courts upheld the decision to eliminate French -SCC ruled in favor of the Manitoba Act -but the British Privy Council upheld the Manitoban government’s decision to abolish French -Mackenzie Bowl (Conservative) ordered the government (under Greenway) to support separate schools -Greenway refused and won the 18** provincial election -Prime Minister Laurier argued that education was a provincial matter -Greenway-Laurier compromise:

-in 1899 the Conservatives were elected -Hugh John Macdonald (son of Sir John A Macdonald) -the Premier passed to Robman *** and lasted for 15 years of great economic and demographic growth -the Liberals became a threat by 1914 and under TC Norris they took the province in 1915 -the Winnipeg General Strike 1919 -the First World War increased the ranks of the labour movement -the Liberals were perceived as too urbanized and contained ‘too many lawyers’ -by 1922, the United Farmers of Manitoba were able to defeat the Liberals -they won 28 seats, with the Liberals elected 9, Conservative 7, and Labour 6 -John Bracken assumed the Premiership from 1922-1943 (the party didn’t really have a leader during the election) -by 1927, the UFM ran under the label of the Progressive Party -in 1928, Bracken created a formal entente with the Liberals, resulting in another successful election -during the depression, there was an excuse for greater economic restraint by the government -this is what Bracken implemented (greater restrictions) -Bracken continued to maintain the various coalitions to maintain power -in 1936, the coalition with the Liberal/Progressive won a narrow majority -Stuart Garson (chief Lieutenant to Bracken) won the 1945 election (with another coalition) -1948 Douglas Campbell became Premier (Coalition of Liberals/Conservatives won the 1949 election) -by 1950, the Conservatives withdrew from the coalition and displaced the CCF as the official opposition -some Tories converted to “Liberal Progressives” which caused confusion -Conservatives placed second to Campbell’s Liberal Progressives in the 1953 election -Duff ROblam (grandson of Roblan Roblam) challended the party leadership fo Progressive Conservatives

Provincial Profiles: Ontario

-almost everything has to have the support of Ontario -36% of the nation’s population resides in Ontario

-Ontario began to assume its contemporary form with the arrival of thousands of Loyalists in the 1780s -these immigrants demanded the political institutions which they had been accustomed to (Britain) -1791 Constitution Act divided the colonies into Upper and Lower Canada -also gave rise to the Tories and Reformers -Tories associated with economic elite -1837 rebellion in Upper Canada led by William Lyon Mackenzie -to resolve this crisis, Britain joined Quebec in the Act of Union in 1841 and established responsible government -the reform movement split into: -Clear Grits: -More democratic reform -Dorch Brown was leader -Moderate Reformers -John Sandfield Macdonald -John A Macdonald was inspiration of the Tories -Ontarios first post-confederation government was a coalition of … led by John Sandfield Macdonald -education bill was the foremost accomplishment -Sanfield Macdonald was defeated in 1871 and set the stage for Liberal rule under Edward Blake and then Oliver Mowet…for 24 years -Mowet’s long tenure was attributed to his ability to maintain a balance between the various interests within the province -pragmatism characterized Mowet’s government -“a model of conservative reform” -when Mowet left, the Ontario Liberals began their decent (although they lasted for another 9 years) -manufacturing condition -all pine timber cut on Crown land would be sown into lumber in Canada before being exported

-1905 Consevrative James Whitney was elected -father of “progressive conservatism” -praised with introduction of Ontario Hydro (although most praise goes to Adam Beck) -he confronted major problems -regulation 17 -restricted the use of French as a language of instruction for the first two years of school…and only then to districts with sufficient demand -a response to public opinion -later relaxed to students beyond grade 2 if they could not understand English -Whitney thought he was helping Franco-Ontarians adjust to an English speaking province -Whitney enjoyed victories from 1905-1914 -succeeded by William Hurst -served during WWI -prohibition -franchisment of women -served a full 5yr term until 1919 when the UFO party (United Farmers of Ontario) -formed in 1914 and grew between 1917-1919 -the party’s success was attributable to the agricultural concerns in rural Ontario with reductions in the rural population -also a moral decay that was perceived in the province -also exempted farmers sons from conscription in WWI -formed a coalition with the Independent Labour Party in 1917 which also felt that their needs weren’t being met by the traditional parties -the aftermath of WWI and conscription crisis produced the feeling that the traditional parties are not working (usually lasts for 5-10 years)

-the 1923 election produced a Conservative victory under Howard Ferguson -regulation 17 was repealed -sustained economic development -railway and highway expansion (in northern and rural areas of the province) -also played a role in gerrymandering the ridings in favor of his party

-George Henry succeeded Ferguson (assumed power during the great depression) -there were three dominant issues: -liquor prohibition -religious -hydro electricity -Roman Catholics were demanding corporate and separate taxes to help fund separate schools -the Conservatives were challenged by Liberals Mitch Hepburn

-Hepburn took majority of the seats in 1934 -not remembered fondly -his handling of GM strike in Oshawa was poor -he thwarted the advance of unionism and the emergence of the CIO (American Congress of …) -sent in police officers -1937 election campaign was fought around this issue -he won, despite this issue but his party was damaged -during WWII he had ongoing conflicts with Mackenzie King’s government -strained the federal-provincial relationship -this hurt the provincial party more than it hurt the federal party

-Liberals were defeated in 1943 -surprising rise of CCF/NDP -took 34 seats -the Conservatives took 38 seats -the Liberals took 16 seats -George Drew was the new Conservative leader -anti-labour -anti-French -anti-Catholic -Drew changed the name of the provincial conservatives to the Progressive Conservatives -he also introduced a 22 point program -a “radically moderate” program -emphasized economic and social security, advance labour laws, mothers allowances, old age pensions -with the strength of CCF presence, Drew’s minority government called an election in 1945 and took a majority of the province’s ridings (66 seats) and 44% of popular vote -1945 election -despite the CCF being the best organized ever, they were accused of being communist and they were damaged from this criticism