The following is a quick summary of Words That Work by Luntz published in 2007.This summary is not an endorsement of Luntz or his partisanship. Professor Nerdster is intellectually free to explore ideas regardless of source. Being intellectually free is a precursor to problem solving, join the club.

Narrow the Gap Between What You Say and What Your Listener Hears

The fact is that people will misinterpret what you were saying and intentionally or accidentally project what they understand into your words. Just as in 1984, when Winston Smith is exposed to the one thing he fears the most….rats, listeners will shape whatever they are perceiving in their own unique way. So through a career of listening to what people say and focus groups Dr. Frank Luntz has come up with some overarching principles around what words work and which ones do not in the US. So in effect this book is actually about persuasion. However, it’s also to narrow the gap between what you say and what your readers or listeners interpret. Because it’s truly not what you say, it’s what people here.

Note there is partisanship in Frank Luntz’ thinking. Dr. Frank ‘s published a new article called American lexicon which laid out a pro-business right wing agenda in terminology that would be appealing to centrist voters. Luntz-Speak. And then Luntzy Award. Harsh and ideological people have railed against Luntz for years.

Luntz is always trying to get the support of centrists. He also seeks to listen then find language that works.

Manipulation is neither good or bad. It’s all manipulation. Artists know this well. Any parent, we know it.

Luntz’ 10 Rules

Listen to the public, emotional and rational and day to day interaction. It is what people say:

Simplicity: Use simple words: average American doesn’t know the difference between deficit and debt: MI3 is better than Mission Impossible 3

Brevity: Never say 4 words when you can say it in three. Simple beats complex.

Credibility: is as important as philosophy. Set expectations lower and the best expectations. So, expectations can sink a campaign.

Consistency: Do not have a bunch of different talking points and new campaign ideas during your campaign season. Repeat yourself, repeat your message, focus on the same lines over and over again to get your message through because people don’t really remember. You will get confused if you have a bunch of different tag lines.

Novelty: We like truly new and different things. Brand new ideas that take on an old idea, have mass appeal.

Sound and Texture of Language: Think Different. i’m lovin it. Are effective because of how they sound.

Go for the inspirational.

Visualize: don’t tell, show! Draw pictures in people’s minds. Ask people to imagine.

Ask a Question: Ask the participant a rhetorical question.

Context: You have to provide context: you need to have relevance.

The target, everyone can immediately remember, you never leave home without it: American Express.

Visual impact is the most important and striking power; speaking in front of your national flag, for example.

Language Is Often Used to Obscure

Beltway or insiders language is not appropriate for the general public: inside baseball is a big communication mistake.

For example, using terms like cloture. There is a reason that few senators make it to the presidency? They speak the language of the insider. How can you even talk about filibusters? The general public doesn’t care.

It’s about getting things done it’s not about the procedural rules of the subcommittee in which cloture and filibusters are used. All the technical deadlock components that impact the legislative process don’t interest people, it frustrates the people’s will which is sometimes in conflict. People really just want you to get things done.

Language is frequently used as a tool to obscure rather than to enlighten… to control and it has illustrates the influence of closed off group in mind: the inside-baseball crowd.

The Sequence of Information Matters

The order of presentation really matters if you have a background presentation and then some theory and then have the actual presenter talk can actually be more effective than having the presenter talk turkey and then provide the background this is what Luntz found out during the Ross Perot campaign in 1992.

Using analogies like sports or war is a very male centric way of describing politics it is genuinely harmful.

Women appreciate being listened to more than having the right questions asked. Luntz says women typically respond better to storytelling, anecdotes and metaphors whereas men respond better to economics rational engineering: I’m pretty sure this is already out of date….

If you talk about a government program then the hostility is significant but if you describe welfare as assistance to the poor you’re going to get a very positive reaction. Lee Atwater called them Welfare Queens. Assistance to the poor was supportive.

Focus on results not the means for example crime reduction is way more popular than law-enforcement. Also note that crime reduction could have many variable inputs in achieving the outcome beyond the law-enforcement interventions and as such it’s more catchall and more popular as a term.

Be The Message

If you are known by your first name that’s a very strong compelling case that you have a brand. No kidding. Building your own brand is very challenging. Living by your values is very compelling.

John Kerry talked about his work in the Vietnam War. The key is you have to show, don’t tell. George W. Bush never fought in any war but he used tough language that suggested he was tough on the topic. So it’s better to act, use wording that resonates with the general public.

Giuliani was someone who campaigned on his working class background, his work ethic and the ‘why’ behind all of his positions. He always provided that context.

And this is the case too with John McCain who was a maverick but basically was right wing however journalists got great news stories from him and he was entertaining.

When John McCain and George Bush were appearing on competing talk shows Jay Leno and David Letterman. George Bush just sat there and took all the criticism and giggled where as John McCain made a strong effort to try to be funny. Journalist thought John McCain had done a better job but in the truth of it, George W. Bush was more compelling by being folky and more authentic.

Words that work language alignment, product and derive, you should try to establish personalization. We buy the product that we have a brand association with. Language of Cheerios is compelling.

How our language is said, really matters.

The Words That We Remember

Memorable movie lines. Fiction is more Powerful for revealing truth than truth.

“Bring it on” as if Bush was inviting violence when he was describing the threat of terrorism and the implied US response. That was a mistake.

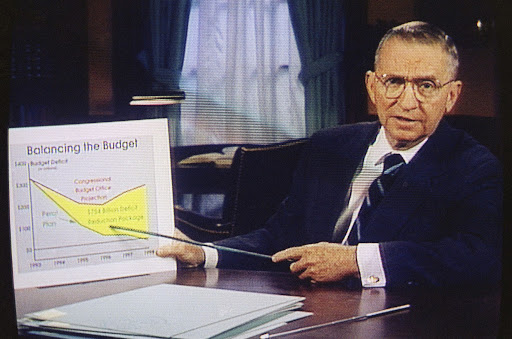

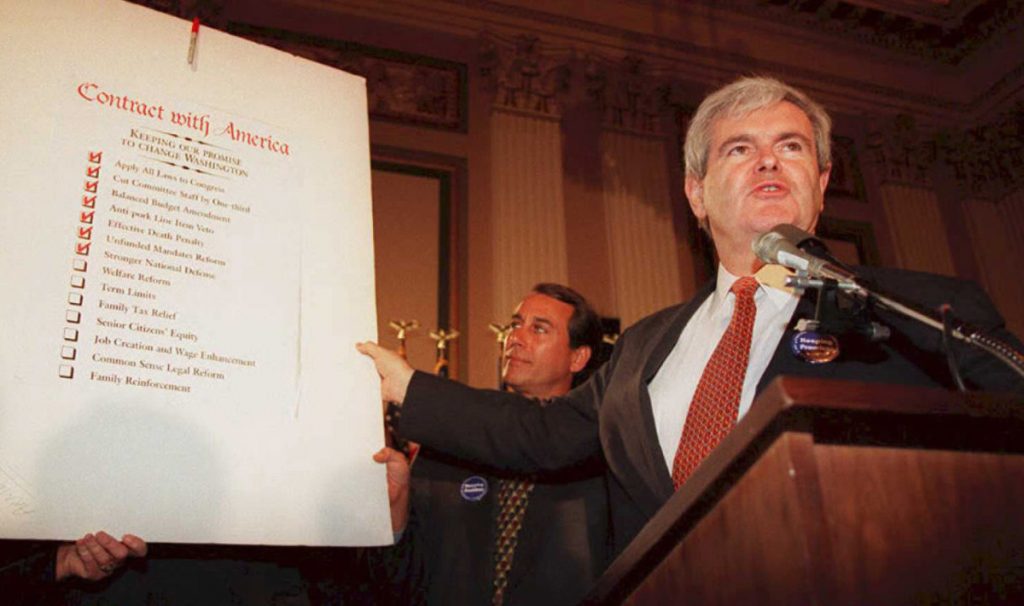

Contract with America

Most effective campaigning is about being sensitive to word choice, using focus groups to tease out what works and what does not. For example, the Contract with America. The ‘contract’ was more effective than the ‘covenant’ or the ‘new deal’.

So the Contract with America was put into the TV guide, The first of the 10 items were important and the last of the 10 items was important because they figured that’s what people would read if they had to skim the list quickly. And it was contractual in the sense that it had the word contract in it but it didn’t obligate the legislators to not seek reelection if they fail to achieve that goal.

The 10 point list was easy and eye-catching. The Democrats felt that it was a mistake to provide concrete guarantees that they could then easily break down and attack. But folks were really cynical and tired of triangulation.

There’s a big difference between not giving and denying when it comes to healthcare. Newt Gingrich felt that the Republican Party should have define itself as the compassionate party. The other aspect of this that was interesting was that Franklin’s claims using the word promise as a politician is an absolutely horrendous mistake never promise anything. Never use the word promise.

There was a debate as to whether decreasing future spending on Medicare was considered a cut the public felt that it was not considered a cut.

Eisenhower came up with the sound bites, the ’30 second’ spot.

Retirement security is way more effective than Social Security. Everyone wants to be secure in their retirement.

It was successful politically liters find ways to get you to imagine. Sympathy, passion. You need to appeal to something far greater.

Federal civil servants are viewed as having no accountability. Is there an enforcement clause in the Contract with America?

Customers are actually looking for simple answers to complex problems they wanna lose weight they want a solution for that. They want to have a ruthlessness if they are spending their money around what they’re going to get. They love to see the things are going to be specifically delivered.

More Words That Work

Imagine!

Hassle-free!

Accountable!

US culture is driven by three major things: I can do attitude, self-reliance and optimism.

Rekindle renew revise reinstate refresh these are all calls to return to a prior default. Redesign rebuild restore revitalize reform and renew.

Efficiency and being efficient are also great however they might be closet words for cuts.

Having the right to choose is also a powerful communication approach.

Patient-centred resonates because it draws an unspoken conscious link with dollar centred or insurance centred medicine. The last thing you want to be concerned about when you’re dealing with one’s loved ones care is dollars and cents. All you care about at that point is your loved one.

Casual elegance!

Independent! Independent candidates. You need to declare independence.

Peace of mind!

Certified!

All-American!

Prosperity!

Better jobs!

Spirituality!

Financial security!

Balanced Approach! For the people, no need to a new civil war.

A culture of!!!!

Straight talk express with John McCain!

Never Say…

Never say entrepreneur say small business owner;

Never say tax reform say tax simplification;

Never say foreign companies say international companies;

Never say undocumented when you mean illegal immigrants;

Never say drilling for oil say exploring for energy;

Never never deny something just do not give;

Never say global economy globalization or capitalism talk about free market economy;

Never say vouchers say school choice;

Never say outsourcing talk about taxation regulation litigation innovation education and legislation;

Never say inheritance tax or estate tax call it a death tax;

Never say crime or criminals talk about public safety;

Never say interpretation when you mean analysis;

Never say capital markets what you you mean investor public interest;

Your schools, your hospitals, your taxes. our schools, our hospitals, our taxes.

Optimism sells, pessimism dwells.

Labour Disputes

Don’t say peace of mind being rewarded compassion commitment listen to employees find common ground comprehensive contract balance instead say security being valued fairness respect responsibility keeping promises respecting employees negotiating in good faith long-term contracts fairness and common ground

Don’t say the union is biased objective union leader should not hold local employees hostage over national issues when are union strikes against a company it isn’t just hurting the company if the union chooses to strike have a legitimate right to stay open it is the unions fault not ours if that workers have to walk a picket line instead say full disclosure you have a right to hear all sides accurate local problems require local solutions no one wins in a strike we won’t do whatever we can to avoid a stroke if there is a stroke will do whatever we can refill our responsibility to a customers.

Never say corporate accountability say corporate responsibility.

Scum literally means a used condom I did not know that.

Important truths about politics; voters do not pick their candidate based on the issues or the policy. Definitely not the case in fact voters look at the attributes the personality, image and th vibe of the candidate more so. The candidate’s brand.

Nostalgia doesn’t really sell in the political arena, you should be looking forward not to a bygone era that feels remembered.

People read books? No people don’t read, people don’t read newspapers, people watch Netflix. If you want to get your ideas disseminated then you should try to get your content converted into a format that people consume. YouTube visual storytelling.

People are educated? No most people actually aren’t educated so you better simplify your messaging otherwise you’re not gonna get it and then you’ll have the educated people as gatekeepers to try to explain your policies or ideas through them.

Want a promotion? Use Imagine in sentences. Also, mirror your boss.

Based on Beeple’s artwork, modified by Professor Nerdster, free to distribute:-)

The short-summary is:

It’s the transition, stupid!

More detail:

Capitalism must solve the climate crisis, obviously, according to Carney. In this chapter, Carney is making a push to show how ESG ought to be used which aligns with his Glasgow COP26 work. This chapter is very much advocacy as he is the special envoy to the UN on climate finance.

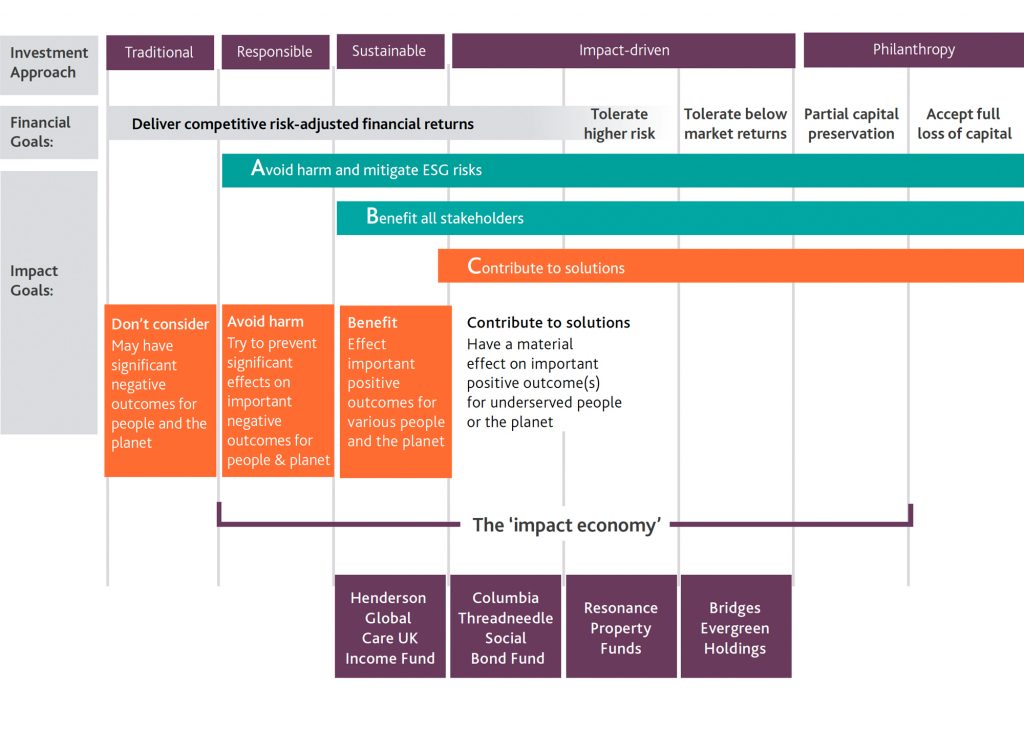

The Rise and Rise of ESG

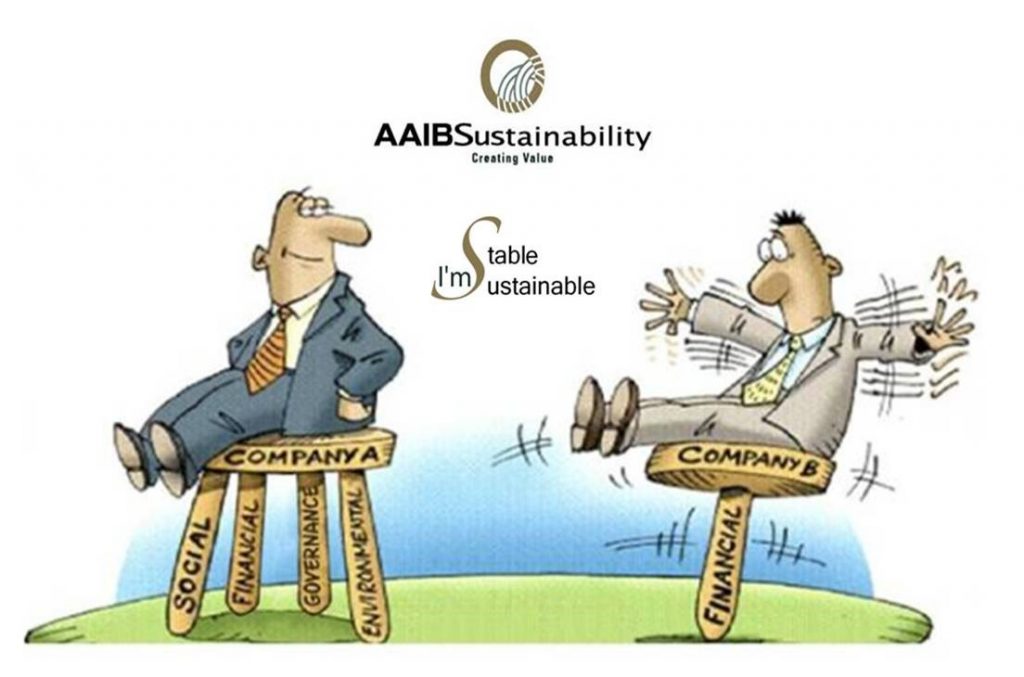

Carney lays out the trajectory for ESG. Just as GAAP (in the wake of crash of 1929) and as IFRS (following the 2008 credit crisis) imposed new standards in accounting, we now see increased pressure for companies to set out their sustainable development goals. Carney identifies a key challenge however, that there is a wide variety in methodologies in environmental, social and governance (ESG) and subjectivity is more prominent then in absolutes typical in accounting. Noting of course that accounting, too is subject to managerial influence. Hence, to shore up standardization, Carney is working on Glasgow COP26 ie. re-assert global standards for ESG. Glasgow COP26 is the next global conference, Paris 2015 was the last major conference. For Carney, the providers of capital such as pensions, banks and insurers will increasingly need more transparency, stipulate their investment horizons and clarify where they sit on the continuum of maximizing value for shareholders versus doing the same for stakeholders (who as stakeholders provide a positive feedback loop back to increased shareholder value in many instances anyway, according to Carney).

The Rise of ESG Historically:

It started with SRI (Socially Responsible Investing) in the 1960s. SRI screened for tobacco companies and apartheid in South Africa. ESG has broadened considerations:

Environmental Impacts

Climate change and Greenhouse Gas emissions

Air and water pollution

Biodiversity

Deforestation

Water scarcity

Waste management

Energy efficiency

Social Contributions

Customer satisfaction

Labour standards

Data protection and privacy

Human rights

Gender and diversity

Community Relations

Employee engagement

Governance and Management

Board composition

Whistleblower schemes

Audit committee structure

Political contributions

Bribery and corruption

Executive compensation

Lobbying

Hortense Bioy

The Surge of Interest in Separating the Good Motives from Bad Execution

Modern ESG involves analyzing and investing in purpose-driven companies. In short, ESG is about having credible strategies while avoiding those that are part of the problem (gambling, firearms, deforestation, tobacco, fossil fuels) but also supporting “bad” companies and industries that are actually part of the solution, not just green washing (fronting that they care). Sustainably managed assets totaled $30 trillion at the start of 2018 and is now already at $100 trillion in 2020 according to Morningstar’s Hortense Bioy in August 2020. In addition, the UN’s Principal for Responsible Invest (PRI) have now been more widely supported which mandated ejecting member who don’t follow ESG principles. So there are now more serious consequences for green washing / fronting that they care.

How ESG can Guide Stakeholder Value Creation

a massive amount of ink in this chapter is dedicated to the technical deployment of a more rigorous version of ESG. The details are as follows:

Carney insists on looking at finance first impact investing, that is to say, “seeking to do well by doing good” (Value(s), 421) using ESG criteria to identify common factors that assist risk management and value creation BUT ALSO delivering superior financial returns;

‘Do well by doing good’ is about positive social or environmental benefits AND accretive financial returns;

With mandatory pensions, you can’t ‘vote with your feet’ but beneficiaries on socially responsible resolutions are possible;

As the CFA (charter financial analyst exams) trains you to identify a client’s risk appetite, it should also train you to prioritize non-financial appetites ie. ESG; Again, think John Kay, who says that the purpose of living is not to breath anymore then the purpose of business is to make a profit. Breathing and profits are necessary but not the purpose…;

Carney supports attempts to evaluate wooly environmental and social outcomes as rigorously as financial returns;

As such, Carney points to the Impact Management Project’s approach as detailed here

·(From the Impact Investing Institute)

· Carney advocates a broad alignment between stakeholders and shareholders which occurs when purpose and competitive advantage of a company both depend on achieving a specific social or environmental value which Carney calls “Shared Value”;

Trade-Off versus Divine Coincidence

Some will trade a degree of financial returns to gain greater social returns while other seek divine coincidence which is what Carney is more interested in exploring in this chapter. Divine coincidence is a central bank / new Keynesian terms that suggests there is zero-tradeoff between stabilization of inflation and the stabilization of the welfare output gap. Divine coincidence approach of environmental outcomes and accretive returns that increase together. But what Carney is referring to regarding divine coincidence is more likely that doing well on ESG just so happens to mean doing well in terms of financial performance for factors obvious as well as less tangible (hard to draw causal links given complexity). Said another way, Carney’s thesis is that stakeholder values have a feedback loop that fuels the maximization of shareholder values. Carney wants explicitly calculated, reported and tracked social and environmental goods to be embedded in financial reporting…and its finally starting to happen through various international bodies: TCFD, FSB, Glasgow COP26, IFRS…..

Why ESG is so Lucrative or At Least Will Be…

Carney’s big persuasion push in this chapter is that purpose-driven companies tend to score on ESG metrics and also tend to outperform those that do not score well on ESG. Why? Possible explanations have to consider:

Superior management = superior ESG adherence = superior financial returns. Some ESG factors are more helpful financially than other ESG factors, the ones that are short-term could be overweighted and thus deliver shareholder value sooner, for example Wal-Mart has a logistics competency at its core and their carbon footprint is reduced which would align with divine coincidence;

Some ESG factors are more long-term. Some ESG factors are indirect contributors of competitiveness such as brand, social license which improve a company’s ability to attract and retain talent. For example, opposite to Wal-Mart, a company that protects endangered species but receives no direct reward might receive more or better job applicants as is the case with Patagonia for example;

The prospect of strong cashflows could explain why a ESG company trade at a premium in the case of Wal-Mart (controlling for other factors which is difficult empirically) and on social license in the case of Tesla (i.e investors and institutions bias towards cashflow metrics, managing what they can measure as Peter Drucker famously points out but social media darlings and rocket launches play into an aspiration mix that communicates both “it’s the transition, stupid!” and stock momentum)

Carney admits that ESG performance will not automatically translate into higher cash flows and that society’s values should not be determined exclusively by whether the stock market gives a company credit for helping achieve those ESG goals.

Somethings…money can’t buy but companies have massive impacts such as species loss or inequality according to Carney. The value in those cannot be captured by the firm and thus not translated into the price of the company.

As Albert Einstein said “not everything that counts can be counted, and not everything that can be counted counts.” Carney notes that there is are a lot of different methodologies to decide what should count, and determine what society believes should be counted…..

Performance….Further Arguments for ESG

Sustainable investment strategies (divine coincidence) outperform traditional strategies, according to Carney. He points to a study by Causeway Capital’s Mozaffar Khan, George Serafeim of Harvard and Aason Yoon of Northwestern University which shows that activities that enforce better and material social and environmental value get you ‘Alpha’ ie outperformance relative to the market median of 3 to 6 percent annually.

Again, Carney references Divine Coincidence here. The researchers found that this may be a function of the positive ESG sentiment such as public sentiment momentum (ie. Tesla is the top example).

Public sentiment influences the value of corporate sustainability activities therefore the price paid for corporate sustainability and the investment returns of portfolios that consider ESG data is boosted by those sentiments.

Again, Carney acknowledges that ESG does not equal Alpha automatically. The formulaic application of ESG ratings or kitemarks are not enough. Also, that as more firms use ESG… “if ESG mainstreams, then overall market performance, risk-adjusted returns, should improve, but relative performance will not.” (Value(s), 427)

Broad societal improvements to workforce diversity and inclusion across the board won’t differentiate specific companies that have helped make it happen, except during the transition to a more equal and inclusive society. “These shifts will create ‘social alpha’ , or what people would colloquially refer to as progress.” (Value(s), 427).

Fiduciary Duty

Carney is making an appeal here to the idea that CFA (chartered financial analysts turned portfolio managers) should really include calculations and inputs on ESG. Investors must weight ESG factors to fulfil their fiduciary duty to those whom the money is being managed. To do that investors need:

1) clear objectives of an investment…ie. that we knew the value that our capital is bringing in terms of ESG.

2) understanding the divine coincidence between stakeholder and shareholder value….i.e what’s good for the abstract other will have intangible benefits for the investor and the client.

Carney argues that investors must consider maximizing their client’s welfare not simply financial results…Recent polls show that owners of capital care more than simply about profit and want ESG to be a factor to some degree. 50% of those surveyed by FCDO (Foreign, Commonwealth & Development Office) were interested in sustainable investment today or in the future….33% were willing to accept LOWER returns if they knew their investment made a difference to something they cared about. In pensions, OTPP (Ontario Teacher’s Pension Plan) and UK cancer researches want to exclude things like children in cages, tobacco companies even if these firms are very profitable

Carney proposes changing the definition of what constitutes fiduciary duty.

Also notes the success of Make My Money Matter in the UK which aims to get individual investors to express their views.

FSB – TCFD

Effective in June, 2021, 1,500 firms with a market cap of $17 trillion are now reporting against TCFD (Task Force on Climate-related Financial Disclosure from the Financial Stability Board of the G20) which was launched only 3 years ago. How do we get this to be accretive is being researched and more people are moving into ESG roles to support that analysis.

The Investing Ecosystem for Stakeholder Value Creation

Carney is basically saying, we need climate disclosure. This investment ecosystem is rapidly developing, evolving and confusing according to Carney. Here are the main actors to explain what the information they need is:

Companies that receive investments and put it to work on green initiatives or social projects get a weighting;

Investors that provide that capital to those companies to support these activities, they can pursue investment strategies that are traditional or ones that systematically do take into account ESG facotrs;

Stakeholders including employees, suppliers, customers and communities are wanting more transparency;

Governments and regulators that oversee the system, set the rules and address the systemic consequences of actions that companies and investors take. It is a superior solution IF the consequences are independent of any single human actor’s will; if the consequences and punishment are autonomous and objective then those punished will not seek to punish the regulator themselves. This is particularly applicable to good parenting, autonomous punishment works much better.

Problems with Disclosure

Obviously, investors have different weighting on each ESG factor because they may care about different factors differently to others, I might like fire arms for example. Reducing exposure to tail risks and improving returns are part of solution, but companies may shift away from social license and resilience to systematic shocks as memories fade (think about how SARS memories faded in the run-up to Covid). We just don’t know when the next pandemic, climate Minsky-moment or decline in social license (catastrophic global war perhaps) will or might happen.

Carney is betting that the stakeholders are going to push investors over time as these ideas that Carney is espousing are mainstreamed.

Trying to understand if he’s late to the party: this has been tried. Companies don’t do this. Impact accounting and ESG needs to be more transparent in their investment goals.

ESG seems to be a differentiator…but there will be push-back.

Information and Disclosure:

IASB and FASB and securities regulators will likely oversee disclosures.

There is the IAS39 for valuation of financial instruments and the IAS9 for expected losses on loans.

But sustainability reporting has the following:

GRI (Global Reporting Initiative),

SASB (Sustainability Accounting Standards Board),

And as mentioned prior, the TCFD (https://www.fsb-tcfd.org/) the Task Force on Climate-Related Disclosures…is another group pushing for ESG disclosures as mandatory.

Social media to scientific analysis informs the view of public expectations…in the case of social media I hope not considering social media is not representative of public opinion.

There are competing interests per topic and opinion will vary over time but those opinions all should matter, according to Carney.

There has been a major attempt to consolidate by the big four (Deloitte, PwC, EY and KPMG) to develop a corporate reporting framework that has agreed standards with the GRI, SASB and TCFD metrics. The metrics are as follows:

1) Core metrics: 22 well-established metrics and reporting requirements, there are quantitative and obtained with some effort and time;

2) Expanded metrics: 34 metrics which are less well established which convey a wider supply chain scope. These metrics are more advanced ways of communicating sustainable value creation.

Impact Management Project (IMP): is building a framework on: What is already reflected in financial accounts (IASB);

§ Information material for enterprise value creation (SASB);

§ Information for sustainable development (GRI);

Integrated Reporting: developed in 2013 to explain the value creation incrementally of human, intellectual, manufacturer, social and natural capital.

The European Union has been leading on non-financial through something imaginatively called “Non-Financial Reporting Directive” (NFRD)

There are three major approaches to using ESG by investors

1. Ratings based Approach

2. Fundamental value where raw ESG data is analyzed in an integrated assessment;

Or

3. Impact assessments

[1] Ratings Based Approach

in this approach the investor outsources the assessments to ESG data providers how have their own methodologies for objective and subjective data and then create a comprehensive indices.

There is a lot of self-reporting and surveys can be gamed;

Ratings system data may vary and therefore data vendors will have wildly different scores;

The correlation between 6 different ESG rating companies was only 0.46 in other words only about half the time did they get close to the same rating;

The more profitable a firm the lower the ESG discrepancy so there is hope that energy and time can avoid inaccurate ESG reporting;

Governance metrics were the weakest at 0.19. In other words only about 1/5 of the time did the 6 different rating firms score similarly;

Disagreement are increasing in 2019. Berg, Koelbel and Rigobon showed that there are three primary drivers of difference in reporting: 1) measurement (what metrics are being used), 2) differences in scope (what attributes are being used), 3) weighting (the level of materiality the ratings vendor ascribes to a given attribute).

Different ESG outcomes mean ultimately different values.

Carney argues the rating approach is simply too subjective. It is not straightforward to value the outcomes that a given investor values. Improvements will come but ultimately, this is subjective.

Carney reiterates that sustained practice of a virtuous goal of value creation is essential.

[2] Fundamental Sustainable Value

in this approach, rather then ratings based approaches, investors have access to the raw tools. The data is usually publicly available data (social media, NGOs, company website, company filings) and then disseminated systematically. Examples are:

HIS Markit;

Refinitiv;

Bloomberg.

The end user determines the materiality. This approach is akin to fundamental analysis in the Equity Research field in which the expert is providing a final investment decision by analyzing company performance, building a financial model that provides a homebrewed answer to the company’s intrinsic value…..and then trading accordingly.

As part of fundamental sustainable value, there is a growing emphasis on Shared-Value. Shared-Value reinforces:

(1) creating innovative products that solve a social need,

(2) enhancing productivity in supply and value chains,

(3) investing to improve the industry cluster where the business is based…

Carney is supportive of this approach because of the complex changes and having someone at the wheel. However, companies are the leaders at conveying their ESG strategy and this is still going to lead to a lack of standardization. Carney admits that there is a significant risk that this is about branding over substance….

[3] Impact, Monetization and Value

This approach looks at the financial AND social contributions. They seek to measure social impact. This approach uses:

IFC Operating Principles,

Impact Management Project Dimensions of Impact,

And Global Impact Investing Network’s GIIN’s IRIS+ metrics,

1/3 of FTSE100 companies already do this IMV….

Impact monetization puts prices on the impacts. The calculations are sometimes easy like: how many solar panels sold minus production costs? While it’s social impact includes solar arrays installed in a house and the array is known to replace CO2 emissions by $17 therefore the monetary impact of this solar panel company is X. But some investors might place a higher value on CO2 creation averted or that the value factor of CO2 will rise which is a value judgement in and of itself. For example, Canada uses it’s carbon price path of $170CAD per ton….

The Serafiem/Cohen Impact Measurement Model asks that you compare the total environmental cost of 1,800 company. You could find 2 chemical companies with sales of $12B each but one created environmental damage of $17B and the other only $4B.

These are the same problems with having to calculate the value of Amazon.com and the actual Amazon. There are some many factors that aren’t measured.

Calculating the impact value of moving from fossil fuels to renewable power generation requires looking at the different estimates of the diminishing marginal utility of impact….

Ranges and sensitivity analysis are useful here but Carney warns that false precision could set in.

The danger in Impact, Monetization Analysis is that the analysts will become disconnected from the raw data and develop a sense of false precision that cannot be validated since it is subjectively derived.

Aggregating the nuance, it will basically create an obsession with that one number much like a stock price itself.

Securing Climate Impact

The Transition to Net Zero…Carney believes that the evidence points to a need to shift toward green solutions in order to prevent exceeding the 2 degrees Celcius consensus from the Paris agreement which will unleash a feedback loop that is irrevocable.

Since climate transition is an imperative of climate physics and chemistry, it’s obvious that this demand for change is going to go mainstream, therefore jump on the wagon. Engineers and politicians see it.

Companies are increasingly being as whether they are doing their part or whether they will be crushed and become “climate roadkill” (Value(s), 449).

25 countries already of a Net Zero plan….Carney believes that harnessing finance is critical to make this happen. Every financial decision- should take climate change into account in that decision-making.

There are ways to evaluate the providers of capital:

What percentage of companies we invest in have a net-zero transition plan in mind?

What percentage of the portfolio is net-zero aligned?

What percentage deviation from the target is a given company?

What degree of the portfolio is actually warming: how much emissions is this particular company generating? GPIF, AXA and Allianz volunteer this information

Carney works at Brookfields to try to create net-zero as an asset class….

Social Purposes of Investing:

William Blake “Know your values rather than be enslaved by those of another.” Carney concludes that we ought to measure if the impact is achieved! Carney does not believe that investor should able to put companies into ethical blind pools of ESG collateral….. Creating value for all means measuring that value. That is what this chapter has been about.

Ø Theory (8/10) versus practice (6/10). In theory, something works but in practice, operationally, that something might not work. Executives are interested in the next 2 to 5 years. As Tetlock showed in his master work Superforecasting, our predictions get very hazy past 5 years. Therefore, executives and others will continue to ignore climate physics in the short-run and point to correlative speculation when weather events are more and more extreme. It’s sad but true. Shareholders are wolves too! Carney does not address the counter-arguments sufficiently here.

Ø AMEE.co.uk in the 2000s and mid-2010s attempted to create a systematic ESG metric that is more than a value add but is mainstream, but then they pivoted to supply chain risk because of the greenwashing effect. Self reporting is one problem, there is the tacit consent challenge. The classic criticism of anyone who supports climate change initiatives is that their intentions are conspiratorial and self-interested at a proportion nearing 100%. I don’t think Mark Carney is looking to enrich himself because climate change is not in fact a serious threat, he may enrich himself somewhat because he is creating value by raising climate finance into the mainstream and it is the right thing to do.

Ø Carney says the investing ecosystem is rapidly evolving, but what is the massive sample size data on that? I’m not talking about a survey which is about as reliable as polling data about Donald Trump. “Yes of course I care about the environment!” Yes, this topic is trending because it aligns capital with solutions to climate change, but the financial sector still has a streak of strategic gambling and as such there will be a strong counter-argument / hedge against ESG as not that accretive after-all. Hard to predict the future but Carney is making an aspiration case, this is how it WILL play out which he’s betting will have a self-fulfilling impact. But as I have argued, I don’t think most people will be reading Value(s) in the way he entirely wants. It’s too lengthy, too academic and should be distilled further to connect with the audience, hence I have provided these summaries….

Ø Carney thinks the Edmonton Oilers have the greatest player in the world and that cognitive error matters because there is no I in team. And his prediction that the Oilers would go all the way to the Stanley Cup in 2020-21 was dashed in the first round by the Winnipeg Jets! Now, you could read into Carney’s enthusiasm that he a) loves the Oilers/ loyal to the team at a partisan level which is fine, b) places to much emphasis on heroes and individual leaders…it takes a village to achieve great things: you have to lead with good talent of course, but also good strategy, supporters and meeting people where they are at to move them into the light. I think Carney does tend to invite people into his ivory tower and then expect to totally persuade by telling people the way he sees the world (based on being well cited).

Ø Carney may be violating his principal that the four most dangerous words in the English language (actually five words) “this time it is different” in this chapter. With ESG, he’s saying “this time it is different”. Social license has been around and doesn’t figure that prominently in the MBA programs of the world, unfortunately. I support the aspiration but measurement is going to be your Achilles heel as well as what motivates financiers who are an exclusive group regardless of some democratization of stock trading in recent years. Few bankers will agree with John Kay that breathing is to living as profit is to business…for bankers the only thing that matters is money and right now. They discount the value of money in the future for this reason. The John Kay quote is that profit is no more important to business as breathing is important to living: necessary but not sufficient.

Ø It’s interesting that Carney believes ratings vendors will never get rid of subjectivity. It’s self-evidently true but what if the ratings firms were rated as well. And that the consequences of their poor ratings were made clearer to the end users….or is the rating process too far removed from the companies themselves while the employees are loyal to their firm and thus consulting firms ought to march in there to provide this oversight?

Ø Carney has shown it is the crisis that triggers re-evaluations and gets political and social change. Therefore, climate events are a series of relatively small crises which are correlated to Greenhouse gas emissions but there are counter-narratives that dispute the causal link of the increases in the hurricane season in part to absolve polluting sectors of the economy (most of the product components). Known as “De nile” from Al Gore’s An Inconvenient Truth.

Ø Machievelli says that presenting to the public that you are lovable is better, but it is also essential that you be ruthless and feared. Does sustainable impact investing draw both actual supporters of the environment/human stability as well as self-interested posers? Yes. The ruthless and feared VW executives figured they could game the system…they are merely the folks that got caught…..

Ø G7 Finance Minister summit in June 2021 was unprecedented as they came together to commit to a 15% corporate tax minimum in all those jurisdictions UK, Canada, France, UK, Germany, Italy, EU, Japan. But of course, where there is a will, there is a consulting firm that will help these corporations maximize their after-tax profit (PwC, Deloitte, KPMG, EY).

Ø Carbon off-setting in theory is cool. In practice, it might be a bit challenging to imagine that the “books balance” in the intended manner of having 1 ton of carbon generated and corresponding additional tree that reduced 1 ton of carbon. The key is the additional tree planted wouldn’t have otherwise been planted, for example…because it was going to be planted anyway, then a carbon off-set, in this case, could be attributed to more then one off-setting attempt.

Ø Carney is advocating more people skill up for ESG. There were Masters degrees in environmental science (a decade ago while I was at LSE) that basically created an army of advocates without any significant job and career opportunities over the last decade (perhaps the economy was also screwed up…but…my point is well known). Just as those who studied Middle-Eastern politics in the wake of the Iraq war, those who studied environmentalism found that their skill is still not really taken seriously on its own. You need to be well-rounded, have strong fundamental understanding of things like accounting, finance, marketing, sales, mathematics, engineering or another marketable skills. That talent stack would, as a whole, get you in the doorway of a desired industry. Often, environmentalists I know would ironically become lawyers defending corporations in ways that padded their ESG optics, for example. So being jaded about ESG is informed by practical experience.

Ø Carney enters the political frame by stating that what society believes should be valued is X. He makes not systematic effort to evaluate what society wants himself. Hence, he needs to consider how citizens engage their own options and preferences.

Ø Carney doesn’t necessarily call out who the polluters are…he doesn’t put pen to paper to say that fossil fuel companies are the problem and could be part of the solution. And what to do about Alberta’s transition? Carney doesn’t talk about a way to help Albertans who have driven the Canadian economy forward in terms of GDP should be compensated…and or supported in retaining economic development locally against the back drop of the Rookie Mountains. Think about how Britain settled the slavery questions in 1834 by compensating the owners of slaves? Then think about how the US settled the slavery question between 1861 – 65? Oil is like slavery in some ways as I argued a decade ago.

Ø Carney as well as other advocates struggle with the fact that profit motives are the metric for success for companies (“you can’t [unfortunately for civil servants etc] manage what you can’t measure”} – Peter Drucker, therefore the creation of value and that the capture of that value in the form of money is THE primary driver. Whether it is the only driver is another matter. But I think a critic can be forgiven for thinking that it is naïve to think that this generation of C-suite decision-makers are mostly pre-occupied with the long-term impacts of the company at which they have climbed the ‘greasy hole’ to the top of. Really lucky and foolish CEOs have been incredibly successful merely because the things that we can measure about them keep appreciating in value…they keep hitting their targets. With ESG, you asking CEOs who may actually be hindering their business but are lucky that what is being measured is working (despite their own bad decision-making which can not be untangled for company performance)…you are asking the CEOs to stake their remaining career on something that cannot be measured in profit terms…

Ø Just because you can find a poll that shows ESG factors are valued by consumers of large asset managers, doesn’t mean you aren’t leading the witness. The question is will we all buy in to the sacrifice and the benefits of the grand transition? I think that more and more people are making decisions with the environment being a variable, but we are poor systems-thinkers. Typically, you and I are going to spend our days being mindful (in the moment) which means we like the dopamine hit of doing carbon off-setting things but not if it gets in the way of amygdala. Also there is a wide spectrum of preferences. To assume that they all care about profits and or all care about ESG, why would that happen? Surely it’s a mix of incentives and motives. And even if there was a major climate catastrophe, it is not clear that polluters would stop polluting considering (they would certainly argue) that the damage has now been done (absolutism abound!), they would argue that the feedback loop of hyper temperature increases that Carney warns about is probably wrong because predicting the future even in climate physics is difficult and they would continue to burn energy to build things they were building just before said catastrophe just as post-Covid, we’re returning to offices because there are rents on that commercial real-estate and C-suite wants to get more value of the capital expenditure on the company’s income statement.

Ø IF THE INVESTOR SEES the consequence of their preferences then they will be shaped for the better. If Quebec felt the consequences of shutting down the oil sands directly then their behaviour would be modified. If the consequences of your behaviours are imposed by an autonomous system it is much better than if the consequences are imposed by other people (Ottawa, bureaucrats, etc); in that latter case, it will fell like a game: As per How to talk so little kids will listen.

Ø Michael E Porter, Goerge Serafeim and Mark Kramer, ‘Where ESG Fails’, Institutional Investor, 16 October 2019.

Ø Robert G Eccles and Svetlana Klimenko, ‘The Investor Revolution’, Harvard Business Review (May – June 2019), ‘The True Faces of Sustainable Investing: Busting Myths Around ESG Investors’, Morningstar (April 2019).

Ø UK Department for International Development, ‘Investing in a Better World: result of UK survey on Financing the SDGs’ (September 2019).

Ø Sarah Boseley, ‘Revealed: cancer scientists’ pensions invested in tobacco’, Guardian, 30 May 2016.

Ø Oliver Hart and Luigi Zingales, ‘Companies Should Maximize Shareholder Welfare Not Market value’, Journal of Law, Finance, and Accounting 2(2) (2017).

Ø ‘Dynamic Materiality: Measuring What Matters’, Truvalue Labs (January 2020).

Ø Dane Christensen, George Serafeim and Anwhere Sikochi.

Ø PwC, ‘Purpose and Impact in Sustainability Reporting’ (November 2019).

Ø ‘Fiduciary Duty in the 21st: Final Report’, United Nations Environmental Programme Finance Initiative (2019).

Carney starts out with the history of companies as a concept and asks what is the purpose of companies? It is not simply to make a profit, but rather to create value which is only partly quantified in the form of profit. For Carney, purpose requires balancing dynamism, fairness(?), solidarity (with employees and community), sustainability (across generations) and responsibility.

As John Kay put it…“Profit is no more the purpose of business than breathing is the purpose of living.” And while you need to make a profit to operate just as you need to breath, it is not the purpose of business.

Who owns the company? Shareholders do not own the companies to which they hold stock, Carney argues.

Wedgwood as the Model of a Modern Major Capitalist:

What is the company for? Carney suggests it’s more than profits. Josiah Wedgwood is the example of a capitalist that made life better for customers by democratizing.

He was born as the industrial revolution was taking off.

He tracked 5,000 changes in experimentation to understand how to make the perfect pottery.

He was an abolitionist icon (ie. against slavery).

He built a town with amenities to support his growing factory.

He was an ardent economic nationalist, admits Ricardian Carney.

Five things that change us in a crisis;

1) Triggers a revaluation of what we value…

2) Triggers a shift in what we value…

3) Triggers an improvement in reporting…

4) Triggers cause resilience…

5) Triggers embed responsibility…

1st for Carney, a crisis triggers a reevaluation of what we value. In prior chapters, Carney showed that the crisis was caused partly by:

· the underpricing in risk and the lack of supervising and off-loading responsibility to the wisdom of the market in Chapter 7’s breakdown of the Financial Crisis;

· the years of undervaluing resilience, with states failing to protect citizens despite ample warnings in Chapter 9’s breakdown during Covid;

· the tragedy of the commons where we aren’t pricing pollution as the producers problem (externality)

2nd for Carney, a crisis changes our appraisal of value and values. Who benefits from these shifts? Shareholder, stakeholders are disrupted through change….

The Covid crisis caused:

· a reappraisal of value and values

· a reset by companies

· a social reset by countries

· accelerated move to e-commerce,

· accelerated shift to e-learning

· accelerated shift to e-health

· a reorientation of supply chains from ‘just-in-time’ to ‘just-in-case’

· greater consumer caution

· widespread financial restructuring (sees a stretched)

3rd for Carney, crises are a catalyst for new reporting of systematic risk.

· 1929 Wall Street Crash (crazy speculation by everyday people using loan money) + Roosevelt’s New Deal = creation of the Securities and Exchange Commission to protect the investors and efficient markets. The SEC then also triggered the creation in 1936 of GAAP (generally accepted accounting principles) which became the global standard to ensure financial data could be reliably counted on.

· 2008 Financial Crisis = reporting for OTC derivatives, reduce the influence of shadow banking, new rules for securitization, accounting standards such as IFRS 9 was developed. IRFS includes what the expected losses are which provides more clarity.

· The Climate Crisis, Carney is (hoping?) to bring about TCFD for consistent, standardized disclosures on climate-related financial risk.

4th for Carney, crises increased resilience, they make us tougher. Global banks have a buffer 10x the size prior. Trading has been reduced 1/2, interbank leading is declined 1/3rd and cloistering of divisions within banks, with deep separation aims to prevent a systematic collapse.

Again, Carney argues the Climate Crisis has a valid target of net-zero. ¾ of the world’s coal reserves…

5th for Carney, embedding responsibility. Having purpose, Carney suggests might have prevented the financial crisis. In the aftermath, regulations, rules and compensation provide the teeth for a better future.

The Firm As A Series of Contracts versus A Purpose-Driven Entity at the Heart of an Ecosystem:

Carney goes through the history of company formation. The coordination of employees, investors, suppliers, buyers. He notes that corporations are indeed people both legally and in reality. For Carney, the company is not the sum of a bunch of contracts, however.

Shareholder & Purpose:

East India Company (the 1st publicly traded company in the UK) was incorporated with the purpose of protecting a monopoly in Asia. The concept of the shareholder was buy shares of a company with the agreement that that capital would be used to advance the purpose of the firm, a larger goal. But during the industrial revolution, in 1844, the UK government passed a law that allowed firms to be incorporated without an express purpose and it made registration much easier. By the 19th century, the focus on public purpose shifted to private purpose.

Shareholder Primacy:

Ford Motor Company challenged the idea further when in 1916, there was a $112 million surplus on their balance sheet. Shareholders wanted a dividend but Henry Ford wanted to direct those profits into creating more innovation and to democratize cars for more people. The Michigan Supreme Court sided with shareholders but the amount doled out was much smaller through managerial discretion. This case Dodge v. Ford is central to the idea that shareholders own the company to which they hold shares. The UK Companies Act in 2006 and the Delaware Supreme Court in 2015 re-asserted that the purpose of ‘directors must make stockholder welfare their sole end.’ So, in the UK and the US, it is to maximize shareholder value. But there is disagreement, Wachtell, Lipton, Rosen & Katz LLP (WLRK) says shareholder primacy is not exactly what is going on….

Carney shows through legal examples in Canada and France that shareholder aren’t even owners of the company and thus the maxim of maximizing shareholder value is flawed. It is true that shareholders do get paid after everyone else: creditors, bond holders, employees, suppliers and governments via taxation both in the UK and the US. But employees cannot diversify their risk to a company as Martin Wolf has argued so shareholders may not really be taking the most risk, aren’t really owners and certainly a poor shareholder who put their life-savings in it is taking more risk than Warren Buffett in the owning of a given share of any company. Shareholders do not have much downside risk either. So, for Carney shareholder primacy is flawed.

The Agency Problem:

The separation of ownership of shareholders and control via the management which have their own self-interest (perks, pet projects, empire building) mixed in with meeting shareholder interests, triggered the Milton Friedman doctrine that:

a) an executive is an employee of the owners of the business;

b) the executive is responsible for maximizing shareholder value;

c) shareholders (probably want) profits therefore that is the value in question;

d) as long as the firm conforms to rules of society in terms of customs and law, they are good.

Carney sees Friedman’s ideas as useful but deeply flawed. Shareholder primacy is problematic and the proof is that Friedman gives himself an out in two ways:

1) saying that money making should conform to customers and laws of their day. As Carney has shown, values are subject to their time therefore, Friedman has an out when there is disembodiment between the market and shareholder. Friedman claims any charity to employees is merely window-dressing. But Carney has shown in this book that there are times where there is deep corrosion in financial markets.

2) saying that shareholders have primacy is flawed because shareholders merely have a ownership of the shares in a limited legal way. There is strain in how the wealthy treat the poor for example.

Companies have Command and Control Dynamics so Models from an Economist is a Matter of Degrees:

For Coase in The Nature of the Firm, the firm is defined by costs difference of providing goods and services through the market. Transactions in the market hold the costs of gathering information, bargaining and enforcement. These transactions bear costs that the firm saves but the expense is the span of control, complexity and diseconomies of scale. The activities performed more efficiently in a Command and Control system within the firm with the rest completed through the market.

Stakeholder Value:

Carney argues that instead of Shareholder Value there ought to be Stakeholder Value, which also happens to be the latest trend in business school literature. Profit is essential but it is not the only thing. Many CEOs reject the notion that there is a single purpose to a firm. For Carney, a successful firm must deliver a balance of competing interests amongst stakeholders (which Carney neglects to define), but this is analogue to the individual who pursues the good life. Competitive advantage, for Carney includes, having an attractive purpose as Chapter 15 will show.

Other Thoughts from Chapter 14:

· For a better tomorrow, we need companies that are motivated by profit and empowered through purpose;

· Profit and purpose are both necessary and re-enforce each other;

· Firms should embed purpose in what they do;

· Corporate purpose reduces risks, inspires employees, provides guidance in uncertainty and attracts and drives innovation;

· Non-financial metrics should matter even if they are notoriously hard to measure;

· The challenge falls with turning a purpose into practice (actions, outputs);

· Maximizing shareholder value (short-term) is not the sole aim of corporations, full stop;

· Environmental, Social and Governance (ESG) can contribute to profits and also purpose;

· The make-up of boards and their focus on purpose is critical;

· Board-level reforms need to include purpose-oriented reform;

· Patagonia, Unilever have institutionalized purpose;

· B Corp certification reward companies that meet social and environmental metrics;

· Danone is a company that embraces a enterprise a mission designation;

· Executive level compensation needs to be connected to ESG factors and needs to be re-configured to align incentives that are longer term;

· Companies need to consider future generations;

· Companies should be engaged in improving communities;

· Reporting is Key: two-way flow of information between stakeholders, shareholders and companies;

· Good and bad ideas need to be tested and then good ideas scaled, and bad thrown away;

· There is more and more evidence that suggest that companies that perform well on ESG also tend to have better financial performance, 63% report a positive co-variation, increased ESG leads to increased financial performance, Chapter 15 will address the counter-arguments.

· Employees who know their employers purpose also have better financial performance;

· Patagonia give 1% of its revenue and they get 9000 applicants per post as a result….;

Ø Chapter’s message in a nutshell: You get more with honey then you do with vinegar, be nice and have better outcomes in good and bad times.

Ø The Covid crisis has accelerated a shift, but for how long? What is the reasonable band-width for which human’s recalibrate? Carney seems to be have a view that change is more permanent than might be believed by myself or others.

Ø “During the [Covid] crisis, we have acted as interdependent communities not independent individuals, with the values of economic dynamism and efficiency, joined by those of solidarity, fairness, responsibility and compassion.” (386, Value(s). This is not quite what is happening or happened or has it? Hard to measure? Are media stories representative of reality? How does Carney know from publications, statistical research or the people he hangs out with? People aren’t, pre-determined. There is speculation and sales in his statement; persuasive as it is.

Ø If Carney is so certain of the benefits of a crisis, then logically should triggering a crisis not be an aim of effecting change? From 9/11 to detonating a nuclear weapon in the Antarctic, causing a crisis is perhaps a logically implication of his breakdown of how the financial crisis has progressed financial technology forward. Carney seems to imply that all the Dodd-Frank legislation was a major success, whatever has been implemented deserves a thumbs up, however the process of providing new safe-guards was very contentious and as Obama points out in my blog post, it wasn’t always that great.

Ø An inverted view might be that the financial crisis brought on regulations that are a mixed bag of efficacy and punishment. Instead of weeding out the incompetent, regulations have caused a retrenchment of those most passionate about finance.

Ø Perhaps this will be addressed in Chapter 15, but how do you really objectively measure ESG performance? If the measures are game-able, they will be gamed, just a fun fact of human nature. Humans are cunning. Get used to it.

Ø Carney took the Patagonia “9,000” applications example in two funny ways. 1) that Patagonia didn’t plant this story as a PR stunt, 2) that Patagonia has those high number of applicants because of their purpose (single causation is flawed thinking or perhaps Carney is simply trying to persuade).

Ø Senator Elizabeth Warren’s 2018 proposed Accountable Capitalism Act requires directors in firms making more than $1 billion to ‘consider’ stakeholders, not simply shareholders, when making choices.

Citations Worth Noting for Part 3: Chapter 14:

v Andrea Sella, ‘Wedgwood’s Pyrometer’ Chemistry World, 19 December 2012.

v Derek Lidow, ‘How Steve Jobs Scores on Wedgwood Innovation Scale’, Forbes, 3 June 2019.

v US Securities and Exchange Commission, ‘What We Do’, 10 June 2013.

v John Kay, ‘Shareholders Think They Own the Company – They Are Wrong’, Financial Times, 11 November 2015.

v Martin Wolf, ‘Shareholders Alone Should Not Decide on AstraZeneca’, Financial Times, 9 May 2014.

v Lynn A Stout, ‘The Shareholder Value Myth’, Cornell Law Faculty Publications, Paper 771 (2013).

v John Kay, The Truth About markets: Their Genius, their Limits, their Follies (London: Penguin, 2003).

v Bank of England, HM Treasury and Financial Conduct Authority ‘Fiar and Effective Markets Review: Final Report’ (June 2015).

v Nell Derick Debevoise, ‘Why Patagonia Gets 9,000 Applications for an Opportunity to Join their Team’, Fortune, 25 February 2020.

v ‘The Business Case for Purpose’, Harvard Business Review Analytic Services Report (2015).v Marc Andreesen, ‘It’s Time to Build’, Andreessen Horowitz, 18 April 2020, https://a16z.com/2020/04/18/its-time-to-build/

One of James Carville’s Clinton ‘92 campaign slogans was “It’s the economy, stupid”. For Carney is “it’s the transition, stupid!” If you can get private financial institutions to truly back the transition then you can contribute to being a good custodian for generations to come. Carney’s work for Glasgow COP26 centres on organizing the plumbing for these financial institutions. In chapter 15, “Investing for Values” Carney explored this further. In this chapter, Carney argues that there are three technologies: 1) engineering, 2) political and 3) financial that need to be marshalled to address climate change.

Engineering Technology

Driving Scale and Innovation: There will need to be major improvements to these hard to change sectors. Very hard to outlaw fossil fuels (ie. decarbonize) which are cheap and do not have a large upfront CAPEX:

Zero-carbon economy, electricity today is 20% green and is projected to be 60% by 2060;

Energy creation needs to be moved to a 90% market share with a mix of wind and solar. To what extent do we electrify everything and do it with green electricity depends on storage and loading challenges since solar and wind are intermittent. And we need to look at power efficiency in products we use;

Global electricity has to increase 5x by 2050 and needs to be generated by renewables according to Carney;

In the UK, off-shore wind farms were expected to generate £140/MWh by 2025 back in 2013 but then in 2014, they revised the number to £107/MWh, in 2016 they revised it down to £57/MWh; In the US, $59/MWh is the cost of coal and now onshore wind-farms are at $26/MWh and solar is $37/MWh….cheaper then coal!

Electric Vehicles (EV)

Hard to reduce dependency on fossil fuels (again, the euphemism is “decarbonize”);

Use hydrogen for public transport;

Tax breaks for EV;

Build the infrastructure for electrical and hybrid vehicles;

Car companies build vehicles in 3 year cycles from planning to off the factory floor so planning for more EV now is critical, even if batteries and charging stations are a problem;

EV is not appropriate for long-haul trucks according to Carney;

Aviation and Shipping

Going to be very challenging to reduce dependence on fossil fuels (i.e. decarbonize);

Nothing is currently commercially viable according to Carney;

The cost of not using fossil fuels is $115 – $230 USD per ton in aviation and $150 – $350 USD per ton in shipping;

Industrial Sectors

Currently responsible for 32% or 17 GtCO2e annually, cement manufacturing, plastic, aluminum, chemical, fashion, furniture and home appliances. The consumption of energy is massive;

A lot of the green technology does not really exist yet;

There are four ways to reduce: use hydrogen (the product being H2O), electrifying processes, using biomass and carbon capture technology.

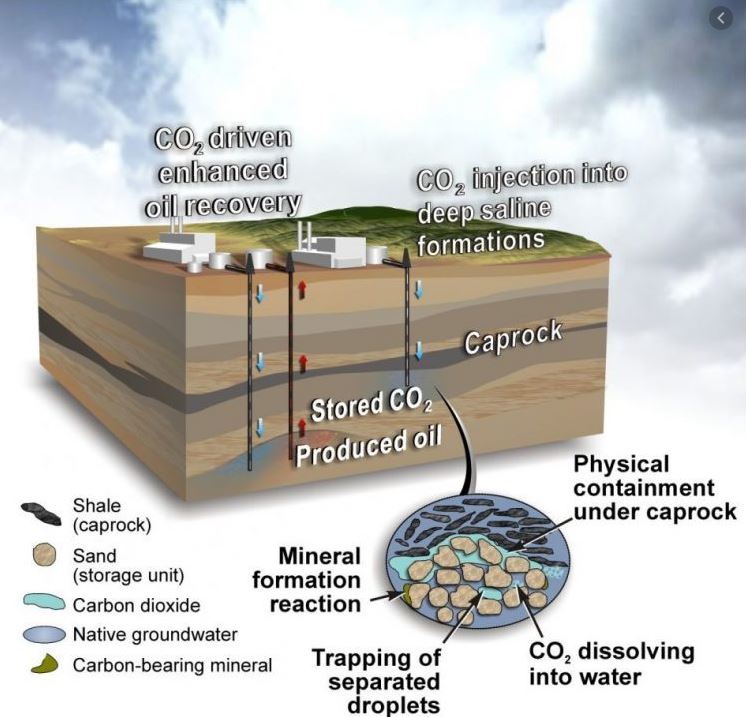

Carney places a lot of reliance on carbon capture and sequestration at the point of production which involved pumping CO2 emissions into a saline solution deep underground, which is theoretical since the cost of pumping CO2 under every factory around the world has not been fully explored or whether there would be a centralized CO2 pumping station for a given geography;

Carbon capture, use and storage (CCUS) are currently about 1% of renewable investments so this is not a hot market;

Direct air carbon capture and storage (DACCS) involves sucking CO2 out of the sky where CO2 is much more diffuse then at the point of production, and therefore the economics right now are between $40 – $400/ton if extrapolated from the small test plants currently testing this technology.

Illustration and Painting

Political Technology

Setting the Right Goals. Carney argues that we need to understand the consequences of our preferences. But he also wants to convince you that his preferences are the best and you should follow him:

SDGs He isn’t talking about new means of engagement with the polity but rather focuses on the fact that nations will fall short by the end of the century, hence the need for Sustainable Development Goals (SDGs) which are part of the UN’s collaborative framework. There are 17 goals with 169 targets as part of the SDGs.

Nationally Determined Contributions (NDCs) are determined by each country and easily fall victim of the tragedy of the commons. At the Paris COP 15, the target that was agreed to was actually 2.8 degrees Celsius above pre-industrial levels by the end of the century.

Greta Thunberg and the societal response: Carney was impressed by her. He showed her the Bank of England’s gold reserves. At the UN Climate Action Summit in September 2019….

Thunberg said “You have stolen my dreams and my childhood with your empty words and yet I’m one of the lucky ones. People are suffering. People are dying. Entire ecosystems are collapsing. We are in the beginning of a mass extinction and all you can talk about is money and fairytales of eternal economic growth. How dare you!….We will not let you get away with this. Right here, right now is where we draw the line. The world is waking up and change is coming, whether you like it or not.”

There was a Global Climate Strike in 2019 with 7.6 million people in attendance in 185 countries…the media struggled to tall a compelling narrative, but the 6th Mass Extinction is coming according to Carney.

Carney argues that revolutions happen abruptly as Cass Sunstein argues, when a tipping point is met, when it becomes socially acceptable (like wearing masks for example).

Values depend on consumer focuses.

Financial Technology to Ensure That Every Financial Decision Takes Climate Change Into Account

Carney argues that companies must take the race to net-zero seriously. For Carney, the financial system needs to take climate change into account, because that’s where the smart money is headed already. Firms can report their own climate disclosures. COP 26 in Glasgow is going to focus on the financial approach. There is money to be made in the transition. And Mark Carney argues that the smart money is turning green.

Harnessing the power of economics to effect change is the most sensible force for good, in Carney’s eyes.

Carney points out that the amount of money needed for the low-carbon shift is about $3.5 trillion in the energy sector per year and twice the rate currently invested in the energy sector….

Climate-resilient systems are needed at a cost of $90 trillion;

Carney argues that the private sector is more then money, we need their innovative drive that is incentivized towards net-zero;

Carney’s 3Rs, these are the three areas needed to make this work: reporting, risk, returns

Reporting: TCFD network: a solution by the market for the market which Carney forcefully argued didn’t work in the 2008 financial crisis….at any rate, their total assets under management is over $170 trillion which includes the largest banks, pension funds asset managers and insurers. The largest AUMs are asking to disclose their carbon footprint in line with the TCFD.

The metrics used are

Disclosure of risk, governance and strategy for climate change;

Consistent metrics across sectors;

Scenario analysis typical in financial modelling and equity research.

The disclosures cannot be static! They should be dynamic such that they reveal financial risks/opportunities. Ask the company to explain how they will reach net zero….

Regulatory Reporting

financial regulators input climate-related financial reporting in their roles.

At the Bank of England, Carney says the Prudential Supervisory Authority are a division of the bank with advice on how insurers should address climate change.

Make the TCFD reporting mandatory at the Federal/National level! IFRS and IOSOCO (which regulate securities) have to agree to make reporting standardized.

Climate change is unprecedented as they have not fully happened yet;

Climate change is massively impactful in every country and globally;

Climate change is foreseeable right now using the scientific method;

Climate change requires action today for horizons in the future that we cannot be predict accurately.

The Bank of England has stress-tested the UK financial system for various climate pathways, scenarios. Climate stress tests about engaging the developers of the model in the contingencies and factors at play.

Returns

The creation of green and transition bonds is an important catalyst. Carney believes that helping companies moving from brown to green is a consultative practice. The typical best plans are as follows:

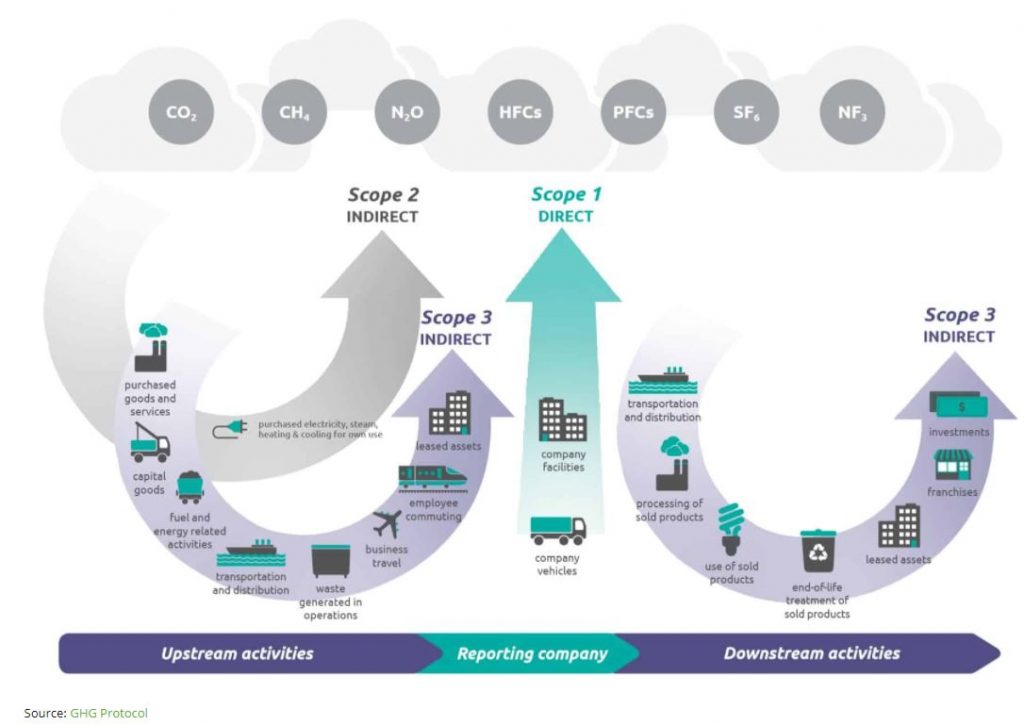

Defining a net-zero objective based on scope 1 (all direct emissions: fuel combustion etc), scope 2 (indirect emissions: electricity purchases) and scope 3 emissions (all other indirect emissions: end products).

Outlining clear milestones and metrics for senior management;

Board of Directors level governance;

Executive compensation based on meeting these metrics……

Green bonds will not be sufficient to pay for the green future. Value will be in identifying the transition. ESG are focused on the s and the g. Investor should be able to calculate the e net present value. “We need 50 shades of green.” (325, Value(s)). Needs to be able to get a sense of how serious a given company is at the senior management level. Embedding metrics in the motivation. The efficacy of transition plans.

Mark Carney says the UK should lead the climate change strategy in Glasgow….hence he is advising Boris Johnson.

Decarbonization is going to be a financially viable source of investment; if you are pulling carbon out of the process then the investment will come to you as an additional value proposition.

Buying offsets is opaque and only 98 million tons of CO2 were traded at a total market value at $295 million, there is no central market. There are no uniform carbon credits and there is a lot of friction so Carney argues for standardization…

The cost of the green tech is high for developing countries but it makes sense to provide that do developing countries as a value added services….how to capture that value once the developing country firm has that technology is not so clear.

Climate policies suffer that same challenge that central banks deal with: the temptation to lower interest rates over long-term stability of inflation. We want to prevent short-termism in finance and now on climate.

Short term costs are hard for politicians, there is a lack of credibility.

Political parties need to get broad support across the spectrum.

Specific climate polities should be looking at the economics. More transparent tracking of climate policies.

Governments should have sustainable growth committees. Carney wants to provide tools for the Bank of Canada and England decision making and targets. The idea is that market will allocate capital and then break the tragedy of the horizon.

Continued growth is not a fairy tale as Thunberg argued.

Policies should be focused on technological innovation.

Clear and consistent communications.

More likely that investment and returns will be made clear.

Policy makers and future costs of doing business need to be calculated and part of the solution.

Not clear that the private sector would want to take on the opportunity to meet net-zero BEFORE a large global catastrophe that is clearly caused by human-made climate change such that customers demand either the private sector have targets in place or the public sector enforces such practices. It will be a train-wreck to check every single companies manufacturing to ensure they have the carbon capture pipes operating properly. It is so easy to pollute. The fines must mark the cost of violating the rules far more prominent.

Ironically, what caused the financial crisis are the individual actors being disassociated with the system level. What Carney hopes is that this be flipped around with climate change. Suddenly, decisions should be made at the system level with a simple boiled down abstraction of 42 +/- 3 GigaTons of CO2 per year must be our pollution cap. However, there is another disassociation that must occur here; namely financial experts in urban centres, far away from the oil fields are talking about transition as if the oil companies are going to just love this whole ‘climate-change agenda’. The consequences of the model make short-term harm very real for the oil industry workers who enjoy their work. I don’t mean we’re wrong about climate change because oil workers might stand to lose economic opportunities due to an imposed legislative or imposed financial capital re-allocation away from fossil fuels, but slave owners in the US lost their economic future because of the threat of legislative decision-making, they were willing to go to war and die in the name of a moral wrong. So, we, including Carney, need to get serious about “Oil Country”.

Ø Carney doesn’t necessarily call out who the polluters are…he doesn’t put pen to paper to say that fossil fuel companies are the problem and could be part of the solution. And what to do about Alberta’s transition? Carney doesn’t talk about a way to help Albertans who have driven the Canadian economy forward in terms of GDP should be compensated…and or supported in retaining economic development locally against the back drop of the Rookie Mountains. Think about how Britain settled the slavery questions in 1834 by compensating the owners of slaves? Then think about how the US settled the slavery question between 1861 – 65? Oil is like slavery in some ways as I argued a decade ago.

“When Abraham Lincoln wanted to curb slavery, he was battling the entrenched interests of the Southern US states. Slavery was a moral wrong, but slavery was also central to the Southern US economy. ” – Professor Nerdster

Efforts to have a global corporate tax neglects to acknowledge that the best situation is where every other country is paying that tax but you have a loop hole.

Just because you can build something doesn’t mean you should. Do people want self-driving cars? Do people want to charge their cars? This is where regulation forces the issue.

Carney’s really skates on thin ice in this chapter because industrial processes rely mostly on energy to melt and shape the products that we enjoy, most items in your house have a carbon footprint that you never see but enjoy the fruits of, the cost to create that same product without generating CO2 is likely significant today. Bill Gates’s How to Avoid a Climate Disaster is pretty much explanation of how this complex set of problems can be solved. Many companies would not exist if it was illegal to pollute….This issue is where the rubber hits the road, unless there is total control of the means of production by some over-arching legal body, there will be an incentive to use fuel…let me think about this further. This is where manufacturing products on the moon becomes more attractive as CO2 there is additive….impractical in my life time but, you know….fun to think about.

With what power can Carney achieve having his preferences reflected in the world? What Carney and others are missing is the way to show the end user the consequence of their preferences. While people do tend to seek out like-minded people, and shun polarization, running for public office would be his best route….. What funding model do we have?

Carney seems to fail to acknowledge that what Greta Thunberg is ignoring is that the transition could be very painful and as such not materialize as she extrapolates it ought to. She is also a child, probably should be in school. The consequences of climate change are heavy in her mind, the consequences of transition aren’t thought out. Both are subjective, terribly difficult to predict and forecast…even with climate physics firmly in the corner of “2 degrees Celcius is a big deal…”