Chapter 10: Covid Crisis: Fallout, Recovery and Renaissance

Key Takeaways

The reality is that mobility did decline as people accepted the lockdowns. State legitimacy is ensured by containing the virus. A lot of what Carney is saying here is a summary of what is relatively uncontroversial. He discusses the framework for the common good. Is that it is possible to calculate that value of a given person? The solidarity of citizens is important to note here, because the view was that no one should die in this pandemic regardless of age (or rather that folks did not want to contract this virus).

Other topics:

Perceived fairness of healthcare: you cannot have one set of rules for the rich and another for general citizens.

Value of a senior versus other citizens.

The young will have to pay twice in increased taxes and the depression of the moment.

Kids with internet had an advantage in home schooling.

Value creation and destruction increased under Covid.

R0 as the metric is a useful anchor just as the 1.5 degree Celsius increase to evade the most harmful effects of climate change.

Managing R0 was the core activity of this pandemic as far as governments were concerned.

Carney rationally described how the government that is presented ought to appear competent.

Local businesses will be emphasized over global for years to come.

There will be future black swans, no kidding.

We have continued to move towards market society however, in this Covid crisis, we have “acted like Rawlsians and communitarian rather than utilitarians and libertarians.” (260, Value(s)).

Covid and Climate Change

Carney predicts that the pandemic’s post active phase will see an increase the societal confidence in science, demands for stakeholder capitalism

Carney then draws a parallel between Covid and climate change. Using science to inform decision making for example. Having targets. How no country can isolate for each other in a pandemic or a climate crisis.

Leadership means being a custodian to the long-term. It’s not about you, says Carney.

There is a so what to this chapter….it falls short of saying anything about how the issuance of debt what appropriate or not. He didn’t talk about work from home or how the virus works which is a missed opportunity.

Carney seems to downplay the fact that the biggest failing of the pandemic is actually that government are operated by people who are focused inwardly in their own self interest within the architecture they have inherited. And such there is a lack of real time data to respond to the real society as it is occurring. There is a high lack information between citizen and government. The government should get out of the way for those who want that and step in for those who need help. Being able to distinguish between complex contradictory people as we all are is critical. It’s a credit card for UBI, it’s an interface to detail ones preferences voluntarily, it’s a relationship that is not simply a marketing blast….

Carney makes sweeping claims here that are sufficiently inoffensive to warrant much comment. There are no innovative sliders that he trials in this chapter, there was a lot of spicy behaviour in Covid but Carney manages to keep it very potatoe.

Surprised he doesn’t go after thie no mask wearers and other violators of lockDown. We tend to forget that these regulations were ignored by millions of people as they were ill enforced…

Citations Worth Noting for Part 1: Chapter 10

World Health Organization, ‘Coronavirus disease 2019 (COVID-19) Situation Report – 11’, 31 January 2020.

Christian von Soest and Julia Grauvogel, ‘Identity, procedures and performance: how authoritarian regimes legitimize their rule’, Contemporary Politics 23 (3) (2017), pp. 287 – 305.

Stephanie Hegarty, ‘The Chinese doctor who tried to warn others about coronavirus’, BBC, 6 February 2020.

Ruth Igielnik, ‘Most Americans say they regularly wore a mask in stores in the past month; fewer see oher doing it’, Pew Research Center, 23 June 2020.

Timothy Besley, ‘State Capacity, Reciprocity, and the Social Contract’, Econometrica 88(4) (July 2020), p. 1309 – 10.

Allan Freeman, ‘The unequal toll of Canada’s pandemic’, iPolitics, 29 May 2020.

Daniel Kahneman, Thinking, Fast and Slow (London: Allan Lane, 2011).

Timothy Besley and Nicholas Stern, ‘The Economics of Lockdown’, Fiscal Studies 41(3) October 2020), pp. 493 – 513.

This chapter discusses the discovering of COVID and all the other asks of this pandemic that we are all very familiar with. Carney was the governor of the Bank of England until February 2020. Economic and family priorities.

The Covid crisis emphasized:

Solidarity: companies, bank, society

Responsibility: for each other, employees, supplies, customers.

Sustainability: where the health consequences skew towards seniors while the economics consequences skew towards millennials and Gen Z.

Fairness: sharing the burden, providing access to care.

Dynamism: restoring the economy with massive government intervention and private sector resurgences…..

Duty of the State:

Carney goes through a review of political philosophy from Thomas Hobbes (1588 – 1679) to John Locke (1632 – 1704) to Rousseau (1712 – 1778) to suggest that in exchange for giving up certain freedoms, the state promises to deliver protection to its citizens. Much the same with central banks; that the public gives up the detailed nuanced control of the money supply in exchange the financial system delivers prosperity.

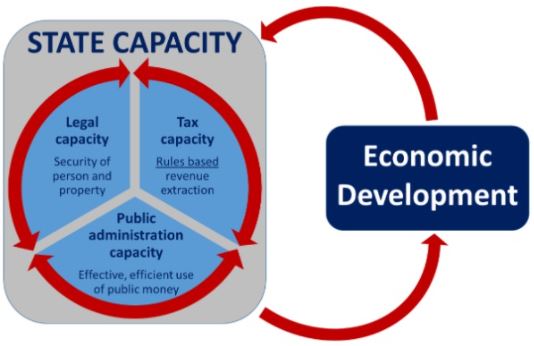

Capacity of the State must have:

1) legal capacity: ability to create regulations, enforce contracts and protect property rights: these include social distancing regulations that aimed to reduce transmission of COVID 19;

2) collective capacity delivering services;

3) fiscal capacity: power to tax and spend: state capacity has moved from 10% of GDP to 25% to 50% of GDP with corresponding services to protect citizens from COVID 19.

Other Points:

Poor compliance in democratic societies;

Stock piles were not restocked;

Bill Gates Ted Talk from 2015 was not actioned by any one actor;

Many countries didn’t have PPE and depended on China’s production initially;

No country is really prepared for this particular kind of pandemic;

South Korea had a pandemic in 2015 and Carney repeats the often mentioned success of South Korea through contact tracing and geo-targeting of users;

Governments need to be better at coordinating: there were departmental territoriality;

In simulations for pandemics this was very evident.

Cost-Benefit Analysis for Hard Choices:

There was a weighting of variables to decide whether to lockdown or otherwise.

The effects of lockdown: domestic abuse were hard to do that.

Calculating the value of a human life: is hard to do. But there is actuaries to put the intrinsic versus investment value of a life or the net present value of all future cashflows that person is predicted to generate. Life is priceless. Sometimes the calculation is about the productivity of the person in life…..

Schelling’s “The Life You Save May Be Your Own” points out that the value of a life principally the concern of the person living it. Value of a Statistical Life (VSL) became the industry standard. The example Carney provides is the a risk of death in a high-risk job might be 1 in 10,000 and employees receive $300 of danger pay, therefore the VSL is $3,000,000. There are several other methods: 1) stated-preference, 2)hedonic-wage, 3) contingent etc. And different countries use different metrics in similar circumstances. In Canada, the estimated range of a human life is $3.4M to $9.9M CAD meanwhile in the US, the estimated range of a human life is $1M to $10M USD. Healthcare looks at quality-adjusted life year (QALY) and cost-utility versus cost-benefit analysis. Schelling’s assumption about how a person can evaluate the value of their life. VSL usage is a moral choice. Wealthcare many not be measured properly according to Carney. Another model is the VSLY Value of a Statistical Life Year. The question remains: do all lives have an equal value or is it the number of life years should be treated as equal?

While it is complicated, I would have liked Carney to have explained the system of money creation in simple terms as it pertains to the pandemic. The level of government issuance of support has been massive. It is imperative folks understand how stimulus money is created.

The perception that money is created out of thin air, subject to political pressures is not true. Zeitgeist and other explanations of the money system are warped thinking. There friends and family going around saying that central banks ‘just print money’ whenever it suits them…

Here is a good explanation of how the central bank enables money creation: To support small businesses and citizens out of work: Is the government increasing tax or are they printing money during the pandemic? The stimulus money was not coming from new taxes so here the government raises through borrowing. The government issues treasury bills to three groups of savers:

(1) public sector (other parts of the government,

(2) the private sector (people and companies),

(3) foreign entities.

The government agrees to pay those savers back with interest at a future date. In the short-term the government uses that cash sucked out of the economy in exchange for the treasury bills to issue stimulus cheques back into the economy. Keynesian economics says that the more stimulus there is, the more economic activity which enables more private savings which then fuels more transactions for bonds. The government can borrow, unlike an individual, through this system as long as the economy is growing at the same or greater rate then that of the debt. The economy is growing at the same rate as debt then the debt to GDP ratio will be stable. If the debt to GDP ratio is stable, then the government can argue for continued investment in its debt securities (ie. bonds).

An additional layer of complexity is that: (4) the source which is the Mint in Canada and the Federal Reserve in the US does not print actual paper money much any more but does indeed ‘print out of thin air’: electronic money, that is credited in the treasury department’s account. In exchange, the Fed then holds treasury bills. The key consequence of issuing too much money with this source (4) is inflation whereby more money in circulation is chasing the same limited number of goods available thus driving the price upward of the individual goods. The 10 year Treasury Note then starts to go up and inflation creeps in. In this case, the Fed needs to increase interest rates to counteract/dampen the purchasing of the demand side…..

The fines for violating COVID rules have an earned media dynamic: we know that the virus is spread through gatherings where one ore more participants has the virus. When someone gets an ‘arbitrary fine’ it effectively markets better than other forms of advertising such as digital. The injustice of the fine is earned media.

There are Canadians under the false impression that government at the federal, provincial and municipal level are not allowed to make rules that ‘violate’ the Charter of Rights and Freedoms. Well, a constitution has to be enforced, my friend…

This time will be different which was Carney’s number one lie in finance seems to be fillable here to say, why would you think that in a future pandemic in say 2055, that our children will be able to respond better then this time?

Just are Carney fails to explain how the central bank manages the money supply, he too here fails to give a basic description of the “obvious’ nature of the COVID 19 virus. Its unique gestation period in which it sheds without the host having any symptoms for T+7 days is very novel unlike other viruses that are initially extremely aggressive, for example, ebola or SARS.

The threat of future pandemics is very real until it isn’t at all. If COVID had the immune effects of HIV then the response would have been more severe in North America. However COVID can be contracted and the likelihood of death is 1 – 5% based on comorbidities. We’ve literally spent the last year talking about this virus. The next virus if it were HIV but airborne, the human race would be in full black plaque mode. Freedom loving + scientific illiteracy are a potent weapon.

Lack of understanding the characteristics of the virus.

In ability to connect barriers that create friction such as laws, walls and masks have the underlying same logic; they do not prevent all the negatives from happening but laws, walls and masks make the unwanted thing from happening, obviously.

Citations Worth Noting for Part 1: Chapter 9:

John Locke, A Third Concerning Toleration, in Ian Shapiro (ed.), Two Treaties of Government and A Letter Concerning Toleration, 1689.

Jean-Jacques Rousseau, The Social Contract.

Thomas Piketty, Capital in the Twenty-First Century (Cambridge, Mass.: Harvard University Press, 2014).

Derek Thompson, ‘What’s Behind South Korea’s COVID-19 Exceptionalism?’, Atlantic, 6 May 2020.

A.E. Hofflander, ‘The Human Life Value: An Historical Perspective’, Journal of Risk and Insurance 33(1) (1966).

Cass Sunstein, The Cost-Benefit Revolution (Cambridge, Mass.: MIT Press, 2018): OECD (2012).

Chapter 8 Creating a Simpler, Safer, Fairer Financial System

Key Takeaway

The Problem with Humans versus Objects – Determinism:

Carney makes the classic case that value measurement losses sight of intrinsic or objective reality and then there is a burst of the bubble and wealthy people lose their shirts. This touches on the central thesis of Random Walk Down Wall Street. Many economists have this instinct to try to explain reality by convincing themselves and then others that people are perfectly rational actors. Carney points out that this rational actors theory is wacky: adding that economists envy physicists and engineers, economists love neat equations and want a deterministic model of reality but that’s just too bad, economist! Determinism, meaning that any input will have a predetermined outcome in the model, doesn’t work when the subject of your experiment has agency/choice. Try telling a toddler that they are rational! Lol.

Sir Isaac Newton said it best: “I can calculate the motions of celestial bodies, but not the madness of people. ” Now, fun fact, Newton wrote that having lost a huge investment by speculating in the famous South Sea Company which basically involved misleading investors into thinking that the British empire had opened up South America to trade when in reality, they were actually capped at 1 ship per port per year in South America….But of course, human being aren’t going to let facts get in the way of investment momentum that drives prices up! Get on the train, folks! And again, because humans are awesome, we will #$ck with you’re predictions whether you like it or not.

Case in point, not everything that is going up is a bubble. Value that is disconnected from fundamentals of accounting are more likely to be a bubble says Carney but there are no guarantees. The investment could be a castle in the sky or just a really good investment…

2008 – 2016 UK:

The lost decade in the UK where there was political fragmentation of the economy is from 2008 to 2016, according to Carney. The real household income did not grow in the UK for that decade (technically 8 years…but whatever). There was a decline of trust in experts. Finance lost its integrity, prudence and became more protectionist. It came crashing down on the poorest in the financial crisis as discussed in the previous chapter. The G20 had to make radical adjustments and reforms. Value was disconnected on the way up and re-calibrated on the way down.

No, I’m not gonna put Thug Life shades (sunglasses) on Queen Elizabeth II. I have some modicum of decency left in me. I thought about though…

When Queen Elizabeth II asked:

“Why did no one notice the credit crisis?” The answer: signed by 33 distinguished economists said ‘it was the failure of the collective imagination of many bright people in the UK and internationally to understand the risk of the system as a whole.’

So another factor is certainly, the lack of systems thinking! What I do may not have a positive / negative impact on me, but it could have a positive / negative impact on others.

The decline in the trust for experts comes from experts being:

too academic and therefore disconnected to practical reality…

simply creating bearers for others to understand their view point and choosing to capture value instead of communicating valuably.

Unable to see the credit crisis coming…

Lack of systems thinking / solidarity / or, in other words, the reliance on the invisible hand / free market as infinitely wise.

The fault lines were:

too much debt;

excessive reliance on markets for liquidity;

Complexity in derivative markets;

Huge regulatory risk,

Misaligned banks and imitators.

Getting Global Support for Reforms:G20 finance ministers backstopped the entire system.

G8 treasury leaders. They didn’t think that the system would self equilibrate as a solution. As such, they created a new plan with the FSB (financial stability board). It is the United Nations for finance. Mario Draghi had an immediate impact on the financial system as the chair. The FSB developed over 100 reforms. And Mark Carney succeeded Draghi as chair of the G20.

Chairing the G20 Finance Stability Board comes with several important lessons:

You must have a clear vision; you need political backing. FSB has the power to recommend reforms, however the national legislatures must put these reforms in place…

You must get the best people you can around the table. Bureaucracy is not helpful here. The group is composed of central bankers, regulators, finance ministers….

You must build consensus that entrenches ownership. Dany Rodrik sees an intractable problem here: a trilema of economics, democracy and sovereignty…We have a seeding or pooling influence. No country is obligated to implement these reforms however it is in everyone, globally that these reforms be implemented at the national level. Commercial banks were happy that “heads they win tails we lose” with the bail out but there were positive reforms made via FSB.

Mark Carney’s Three Lies of Finance:

Financial crises happen frequently, if you hear someone say any of these lies, then take note:

“This time, it’s different”

“Markets always clear”

“Markets are always moral”

“This time, it’s different”: what’s happening today is fundamentally different from all prior human history….Nope, don’t believe this lie. Usually, a new innovation is compelling because of its initial success, complexity and opacity. Solving the stagflation of the 1979s and 80s with new monetary stability that were democratic, effective, evident remits, strong governance….The Great Moderation from the 1990s to 2008s also paralleled, technological growth, non-financial consumption, such that it was easy to become complacent. And people assumed housing prices can only go up. This optimism is known at the business cycle. Carney refers to this as the Minsky moment: where lending is abruptly pulled back when financial experts realize there is a correct brewing and thus causes the economic downturn to more severe. In 2008, “Minsky went mainstream.” (186, Value(s)).

“Markets always clear”: at the right price, excess supply and demand will clear (ie. the supply will meet demand). Labour markets are efficient and clear? Sorry, nope they are rigid and sticky. If money is efficient, then they will reach equilibrium? Sorry, nope markets are incredibly ineffective in reality. Markets do not always clear because life is not a textbook. You can’t describe the real world because people are too complex for any mental or predictive model. Synthetic credit risk; the risk was spread all up. Panic ensues with risk being pooled. The real world is far more complex, we cannot anticipate all of human activity at any given time. Calculating every scenario is impossible, Newtonian physics doesn’t quite work in every scenario and physics doesn’t even involve tricky human beings.

Keynes in General Theory shows that when having his students rank the prettiness of faces in exchange for a prize, it’s more important to calculate what the average opinion believes the average opinion is. Keynes noted that this is what happens in markets where everyone else was thinking, the derivative of the derivative of what other people will do matters more (subjective utility). Keynesian saw the instability is on spontaneous preferences, the full consequences are only based on animal spirits. The belief that markets are always right was what enabled the last bubble and the next bubble. Markets are populated by people however, fickle people.

Cass Sunstein argues that 1) preferences in public differ to what is in our heads, 2) social obligations impact our acceptance of new things. For example, if 1000 people protest something, then we will be more amenable to that something as well. Read: Robert Schiller’s Narrative Economics. Critical mass opinion happens in finance as well. The Minsky cycle works on average and average opinion. How do markets become more differentiated? There is a spontaneous urge to make a decision rather than a complex weighted calculation of the mathematical benefits x the probabilities of a given consequence of the decision…

“Markets are moral”: FICC (fixed income, currencies and commodities markets) have a lot of fraud in them even though they determine the cost of resources, food, housing, government debt prices etc. The commodity squeezes in rye in 1868, cocoa in 2010, and ‘wash trades’ in Manhattan Electrical Supply on 1930 and the Tera Exchange in 2014 show a recurring phenomenon. There have been a lot of squeezes. Planted rumours to drive up a cost happens frequently wherever traders are bored or desperate. Tweaking LIBOR and FX involved manipulating these foreign exchange benchmarks rates for the interest across firms at the expense of retail and corporate clients in the billions. Technology evolves and laws are passed. Engineers of the subprime crisis were clubby and colluded online, globe bank misconduct costs were $320 Billion for $5Trillion of assets. People were colluding online and few were held to account. And there was no rush to take the blame. Trust in the UK went from 90% (1980) of UK citizens thinking banks were well run versus 20% (in 2008). Financial firms help the real economy. The FICC markets, markets are ever more important to people. FICC markets can go wrong with poor regulation. Carney argues you need Hard infrastructure (regulations, foreign exchange benchmark objectivity) and Soft infrastructure like corporate culture, informal codes and policy handbooks. Light banks. Central banks participate in fire insurance. Mistrust between companies and hesitate to invest in firms. FICC infrastructure is key, soft codes of infrastructure, weak banks. Relies on informality.

Carney argues that the solutions are the following:

Trust: G20’s Financial Stability Board helps by acknowledging that the market is amoral and will not always clear by instilling greater trust, less complexity.

Smarter: Ensure traders remain pro-market (shouldn’t be a problem) but support smarter regulation.

Avoid Lies: Ensure financial professionals avoid the attractiveness of the 3 lies.

Realistic: Recognize that regulation will not bust the cycles since innovation is always happening but ensure that regulators be understanding. Implement policy that make real markets more robust with market infrastructure that creates the best markets for innovation.

Transparency: In 2008, Over the Counter derivative trades were largely unregulated, bilaterally settled (closed door) and unreported, but now 90% of new single currency interest rate derivatives are centrally cleared in the US i.e there is transparency.

Systems Thinking: Ensure financial professionals recognize the importance of protecting the system as a whole.

Risks in Emerging Markets are a danger for another financial crisis where the lie that markets always clear continues. China’s economic success contains a lot of shadow banking (SIVs, mortgage brokers, finance companies, hedge funds and private asset pools), there are lots of repo financing, major borrowers and banks with significant opacity. There is now a worrying amount of debt in China that could leave Ray Dalio reevaluating his career choices once again. There could be a major margin call / run on Chinese assets, with first mover. There will be mismatches of markets. There could be a rush to get out of the Chinese market: this is the risk of being trapped when the assumption that markets will always clear (buyers and sellers will find each other) is exposed as wrong. Cyber to crypto crises could also trigger another financial crisis.

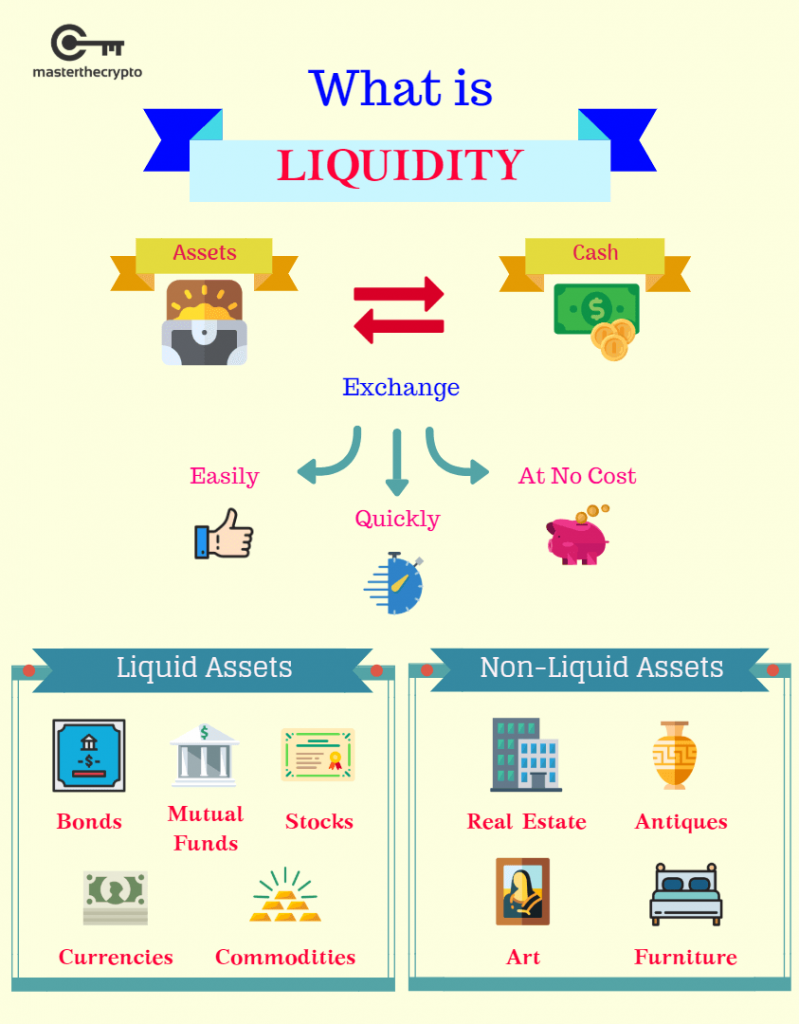

Risks in Illiquid Assets treated as if They Are Liquid:

New risk is the global assets under management of $50 trillion in 2010 to $90 trillion in 2021. But $30 trillion is promised to be liquid when it is illiquid assets. Carney’s addressed this problem of not having consistency between liquidity of funds’ asset versus their redemption terms while he was governor of the Bank of England with the help of the FCA (Financial Conduct Authority):

1) liquidity of funds’ assets should be valued as either a) the price discount needed to do a quick sale of a vertical slice of those assets OR b) a time period needed to sell the asset without a price discount.

2) Investors who redeem get a price for their investment that mirrors the discount required to sell a proportion of a funds’ within the special redemption notice period;

3) the “redemption notice period mirror the time needed to sell the required proportion of a funds’ assets without discounts beyond those caputed in the price received by redeeming investors.” (196, Value(s)).

During the 2008 crisis:

Liquidity disappeared with cash-powered banks refusing to lend;

There was a ‘run on repo’ which increased the haircuts on collateral to de-risk counterparties which were shadow banks that then collapsed;

In Europe, the debt crisis compounded these problems driving up nationalist sentiments…

There is now the liquidity coverage ratio and net stable funding ratios…but there are weaknesses with US repo market troubles in 2019- 2020. The Fed’s open market operates calmed down…Carney doesn’t know where the next bubble will burst but he has a few ideas.

Bagegot’s principal of being the lender of last resort thus preventing short-term liquidity shortages from causing wide spread insolvency.

Bank of England presentation by Mark Carney…

Central banks have challenges:

Figuring out if the firm is solvent when the market is against that firm’s assets and the market can be wrong longer than that firm can stay liquid;

What constitutes good collateral, can always lend government bonds and in the 2008 crisis, it didn’t appear to have an impact on the functioning of the system, banks horde

The penalty rate means the firms come late because it convey weakness.

Central banks have now moved to doing transparent auctions of liquidity to many counter-parties which includes banks, broker-dealers, an central counterparties in the derivatives market. Bank of England has a contingent term repo facility….

An Anti-Fragile System – This Time is Different – What Was Done to Banks:

Public trust was harmed most by the mantra of too-big-to-fail banks.

Banks didn’t pass lending out enough which amplified inequality.

Privatization of profits while socializing the losses harmed trust.

Public paid $15 trillion in bailouts, government guarantees against bank debts and special central bank liquidity projects…..

G20 FSB brought in standards to create an anti-fragile system:

Banks are less complex.

Banks have a ‘living will’ and are reorganized so they have a firewall between the banking that continues to serve families and business even if their investment banking division is imploding.

Trading is less between banks thus shifting to lending to customers.

Public funding has dropped by 90% post-crisis with market discipline…

Senior leadership can be expected to bare the cost of failure.

Can’t legislate virtue but can legislate incentives around how senior leaders train staff.

Improving cyber penetration attack resilience.

Looking for risks across the economy, thinking system level about where the next crisis is least likely to be and make sure that is focused.

Macroprudential policy: addressing systematic risks….cyclical risk when the financial system loosens up, debt grows and complacency sets in, the Minsky effect is severe…

Macroprudential policy: addressing systematic risks…structural risks when there is a wbe of exposures to derivatives risk, which means the need to have liquidity buffers, restrictions on mortgage lending, shutting down the shadow banking approach.

Bank of England serves the purposes “To promote the people of the United Kingdom”

Restoring Morality to Markets:

Oscillating regulation, light touch versus total regulation.

Aligning compensation with values;

Increasing senior management accountability;

Renewing the vocation of finance.

Longer-Term Horizons Focus the Mind: Bonuses in the UK are now managed with compensation by delayed by 7 years. If there is misconduct then bonuses can be clawed back, according to Carney. Business mission statements tend.

FICC Markets now have new guidelines:

have clear, proportionate and consistently applied standards of market practice;

are transparent enough to allow users to verify that those standards are consistently applied;

provide open access (either directly or through an open competitive and well-regulated system of intermediation);

Allow market participants to compete on the basis of merit; and

Provide confidence that participants will behave with integrity.

Effective markets are those which also:

Allow en users to undertake investment, funding, risk transfer and other transactions in a predictable way;

Are underpinned by robust trading and post-trade infrastructure enabling participants to source available liquidity;

Enable market participants to form, discover and trade at competitive prices; and

Ensure proper allocation of capital and risk.

Drawing on the Magna Carta:

Having the right principles is essential. Keep pace with the innovation. Senior Managers Regime (SMR) individual accountability. Values need to be exercised like a muscle. SMR makes sure senior leadership is accountable even if many of them were involves in the 2008 financial crisis. Employees must be connected to their communities.

Mark Carney can look to Mario Draghi for inspiration since, Draghi is now the Prime Minister of Italy (as of 2021). Central Bankers can cross into the political sphere. Currently Draghi is trying to get bank mergers to happen in order to clean themselves up. So like Carney, using the power of politics to effect change is sometimes valuable where as a central banker, you cannot effect change. Analogies, and history does not have predictive power, Italy is very different from Canada, however it is instructive that getting into a position of power may not be a high hurdle for Carney. Finance catteacts people with no socience training, because they are looking for absolutes. These folks lean deterministic.

A bit odd that the Senior Managers Regime (SMR) doesn’t really connect because the people who self-select to work in banking are frequently math. The problem is that the people with the experience made decisions in the financial crisis that seem to benefit themselves disproportionately company to the general public. It is similar to having doctors make decisions for hospitals, there is a conflict of interest in being in control and regulating oneself.

Perhaps the bad behaviour is in Crypto…

Great economic shocks cause institutions to recalibrate and reform. It isn’t the individual actors that drive such change but rather macro externalities where no one internally can be blamed that cause reform.

Citations Worth Noting for Part 1: Chapter 8:

Carmen M. Reinhart and Kenneth S. Rogoff, This Time is Different: Either Centuries of Financial Folly (Princeton: Princeton University Press, 2009)

Raghuram Rajan, Fault Lines: How Hidden Fractures Still Threaten the World Economy (Princeton: Princeton University Press, 2010).

Hyman P. Minsky, ‘The Financial Instability Hypothesis’, Levy Economics Institute Working Paper No. 74 (May 1992).

Kenneth J. Arrow and Gerard Debreu, ‘Existence of an equilibrium for a competitive economy’, Econometrica 22(3) (1954).

Gilian Tet, Fool’s Gold (London: Little, Brown, 2009) which shows that derivatives were distributed throughout 100s of balance sheets through the pooling and distribution of that risk. Similar in essence to a decentralized ledger.

John Maynard Keynes, The General Theory of Employment, Interest and Money (London: Palgrave Macmillan, 1936).

Wlater Bagehot, Lombard Street: A Description of the Money Market (Cambridge: Cambridge University Press, 2011).

Financial Stability Board, ‘Strengthening Governance Frameworks to Mitigate Misconduct Risk: A Toolkit for Firms and Supervisors’ (April 2018).

First of all, we tell stories to keep the wolves from the door, mortality, according to Ken Burns. Life is short. There is no solution to learning other than to go and do, which is the best way to learn. There are no rules about films. Ken Burns has been doing it for 46 years, and he does not believe in formulas in documentary films, there is no formula. The only formula is Doing + Learning = Growing.

The Renaissance of Documentary from the 1980s to Present

There are so many documentaries that have emerged in the last few decade that has put the genre on the map. And notice that there is no orthodoxy. Errol Morris, Michael Moore, Al Gore and Werner Hertzog all doing their own things in this genre. Again, no formula. Ken Burns does not do his own narration and / or ask questions on camera.

The Brooklyn Bridge

He felt that biography of Washington Roebling for the Brooklyn Bridge was important. It was emotional. You have to have faith in yourself. That project was Ken Burn’s first in 1981. He had a shoestring budget to make it happen. And a Ken Burns documentary takes especially long, hence he left New York to finish the film and moved to New Hampshire where the cost of living was much more reasonable.

Know Your Creative Goals

Is this what you want to do?

No one is going to give me the budget, you have to beg, borrow and steal!

Transcend: film-making is industrial anxiety, there are 100s of things that can go wrong. You need to welcome the unanticipated problems. You need to have patience.

Be a Jack of All Trades

Writer, sound designer, fundraiser, marketing, and you will give your spiritual life to be a good film maker. Don’t let it be one single skill that you possess: be well-rounded, inquisitive.

Documentary filmmaking is highly collaborative. You need a good cinematographer and a good writer. A film project cannot be a one person program. You have to make your own career path, what are you willing to do for your art go commercial or go public funding, it will still be your art.

Research Everything, Even While You Build the Story

Your model / filter of past is going to be challenged. The opposite view is possible. The Vietnam War ($30M budget) humiliated Ken Burns with new facts. Conventional wisdom is harmful to truth. You have to tell the true story of the Vietnam War which is more nuanced then Ken Burns realized in the outset…same with his audience. That particularly documentary being probably the most important since the Civil War.

The Drama of the Truth

How far can you go with art before you mess with the truth? What have I done in the service of cinema in order to tell the truth? Inclusion and exclusion are both part of the story. There has to be a human act of faith in selecting what is included.

There is no such thing as objectivity. There are a completely different realities and you then have to average things out, according to Burns. Human experience is human experiences (plural) and as you gather them you can more clearly understand that moment. You need to take a certain license, however. The truth is you have may be challenged by a lack of evidence whether it be photographic or otherwise.

The TED Radio Hour: Manipulation

Manipulation is Part of Art

Contradiction is very common in reality. Be manipulative in your story telling. You shouldn’t see manipulation as evil. You need to be manipulative. How do you get along? Manipulation gets the shooting done. If you aren’t manipulative then you are deceiving yourself first and everyone else second.

The Civil War Script

Proposal script for the Civil War had certain sections pre-written before production. You need to write a treatment of your story. You then need to lay out the parameters.

Money is the most governing thing: money is very important.

government,

individual funders,

corporate funding.

You could also develop a bankable story. You need to make the audience no longer understand. Ken Burns’ team writes a lot of proposals.

You have to be realistic budget: how much does it cost for the sound people, editing, you have to pay yourself. Push through: the made a good food, Ken Burns is fundraising and being told 1500 times and 15 times told yes. So Ken Burns is a sales guy in effect.

Structuring the Document Narrative

You want to know how it can be told. We are under the powers of story telling.

Archival information is critical to historical documentary: you need to follow leads.

You shouldn’t look at the great men of history; look at the bottom up and the top down. You should look for the home movies, for example in Vietnam. For example, in The Vietnam War documentary a solider sends home videos back home from the front and the towns people.

Shaping Nonfiction Characters

Liberate the characters of the heroes and villains model. Abe Lincoln, he attacked the US constitution. The Civil War is morally complex.

Layered Characters Drive Narrative

It’s most effective if your audience thinks the character should make other decisions than the ones they make.

Many light bulbs drawn on colorful sticky notes.

Visualize Your Story Boards

He had the episode of using the post it; then they do these different modes in the story.

Balance Larger Themes with Individuals

Good writing is easier building blocks for a better story, you have to have good writing to back the rest of the experience.

Narration is based on 3rd person in Ken Burns films. Ken Burns did not invent narration in documentary film. Do not be afraid of narratives. The word and imagine together are more powerful than the sum of their parts.

The 3rd Person Narrative

Words are not set in stone. There will be many drafts. and then you do a blind session. Does the structure makes sense. Then you do a blind assemblies of the voice over and then the visuals.

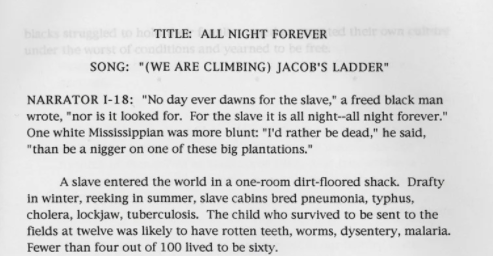

Using caveats which is “may have been” qualifications. Slavery was abhorrent, but the statistics are abstract. 4 out 100 lived passed the age of 60. Born in a shed, most children died before age 12, if they did survive they would work in the fields.

Ken Burns Loves Still Photos

Trust the audience to be more engaged. I will invest those limitations. Ken Burns is an effect is not about giving people a slideshow. The psychological response to a picture.

Imaginative Symbolism

Word and Image is (1 + 1 = 3): Mirror illustration, have the words and the picture talk to each other. We look for the obvious but try to find the dissonant and different because you will find new meaning in it

Jack Johnson Unforgivable Blackness. These past moments rhyme perfectly, for Ken Burns, with what is going on right now in the US.

Selective Interview Subjects: Burns interviewed 1,000 interviewees and got only 100 interviews. Some people don’t want to have stumbling, some people clam up.

Be Honest and Persistent: being completely transparent.

Conducting an Interview

Stay Open to Possibilities: you don’t know what is going to

Conducting an Interview: be very nervous in the interview, be humble. If it doesn’t work, then take the blame and or say we moved in another direction. Ken Burns asks the subject to insert the question into their answer so that editing-wise his voice never has to appear in any of the films. You want to break down the wall and get them to drop their barriers.

Honour your interview subject: you should conduct an interview like you planned to meet him.

Stories Greater Than Facts: The facts aren’t as important as the story about the curiosities. About the stories in the war.

Ken Burns, does not treat his interviewees as transactional. Use your own imagination to effect emotional connection to the audience.

Ken Burns uses live cinematography that are still shots. The magic hour is the sun setting light.

Steal Shots: Sometimes you have to steal the shot if you can’t get access to the a certain area.

Lighting an Interview: make sure that you have eye line, don’t include anything other than the subject. Focus in on the face of the person.

Shoot Interviews with A Light Crew…just easier.

Music is the Quickest to Feeling Art: music should not be an afterthought. Start to use particular themes in the key moments of the film. Get most favoured nation deals for the music. Ashokan Funeralwas actually write in the 1980s but the instruments were of that area.

Editing Process: Trust your editors….Ken Burns actually doesn’t edit his own films these days.

Blind Assembly: worked on the narration, then you just hear a radio play. So you can then start to add the picture.

Messy Full Research Document: The first assembly, it should be very messy. There should be a daunting task to make the film to make it an actual film. Take it piece by piece.

Authenticity: You need to make sure that you convince the audience that this is another new thing, not a summary of someone else’s story.

Private Viewing: You need to follow up with the historical advisors. And then have a lot of bodies there to review the film before launch. Take very particular negative feedback and fix it, don’t give them scripts for the film or they will read that rather than watch the film.

Editing: A Process

It is the principles: You want to be able to edit your answer on how was your day. Tell a story. Not all 1,440 minutes of it.

Tempo In Art: You need to triage the quality of the film, it’s not about imposing yourself. Documentary film making is absolutely a tempo on the screen on musical notation, a film must be rhythmic.

The Vietnam War Introductory: The blind assembly is key, you have the dramatic structure. Scratch narration (use your own voice) until you have the best voice in town Peter Coyote..

It’s the personal story and intimacy of the character that people remember.

The Recording and Using Voice Over: the most important narrator has to be confident. Peter Coyote has to inhabit the non-journalist voice. You do not want to have the dramatic voice be done by a celebrity unless the content is able to flip the audience over so that they are in the scene, and can’t recognize the voiceover as a result. You want the front row lens in.

Rank the Quality of Performance in Real-Time: Give the narrator the script and then circle the narration runs that you liked in rank order.

Never Record the Voice Over to the Pictures: record to the words.

Sound Design: there is a lot of video footage without sound so Ken Burns has to create that. There are 175 recorded sounds in the Tet Offensive sequence of The Vietnam War.

The Artist’s Responsibility: it is the artists responsibility to lead the audience to hell but also to led them out.

Allow Moral Dissonance to Occur: interesting people populated most people. You should not self-select away. It’s not one thing or the other. There are strong divisions in the United States because it is such a vast country.

Decide Your Outlet: Distribution is needed. You want the most number of the people. Ken Burns learned that you give the film to PBS and it gets scale.

Evangelize the Film / Aspiration to Action

Allow the audience to assign their own meaning. You want the audience to have a conversation with you and they are continuing a conversation that they are having that conversation with you.

You need to go out there, nothing happens unless you start. You need to make the phone call to make sure you find that support. You need to jump over the chasm from aspiration to action. Don’t let your mind crush the idea, do something to get started.

This publication is dedicated to finance, politics and history