Part 3 Reclaiming Your Values

Chapter 13 Values-based Leadership

Key Takeaways

Talking about leadership is risky for Carney as a prospective Prime Minister-in-waiting in Canada. It opens him up to any gap between preaching and practicing in the future. There have been a lot of fools in finance that preached the “Great Moderation” who were proven rather wrong in 2008…Allan Greenspan who was Carney’s idol of sorts for example. Carney’s view is that values can be reasserted by describing what is required for leadership.

This time, things are different = the five most expensive words in the English language.

Leadership Models:

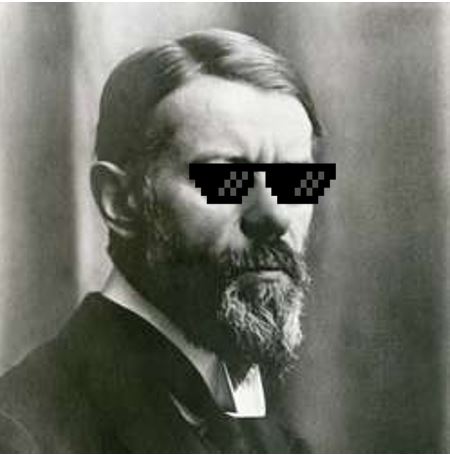

Carney walks us through the different leadership models. Max Weber (1864 – 1920), the grandfather of sociology and much of modern social science breaks leadership down into three discrete types

- Charismatic

- Traditional and

- Legal-bureaucratic

And that’s a fine framework but not really important.

Other Points on Leadership

- Authority is not leadership + institutional authority is not good enough over time without social approval from co-workers.

- No one will accuse central bankers of being charismatic, Carney jokes. They are technocratic and exhibit legal-bureaucratic leadership.

- Great Person theory ie. born with charisma and intelligence from Thomas Carlysle is bunk according to Carney.

- Carney is an advocate of behavioural theories of leaders: leadership is a process not a gift. It is usually through observation and teaching.

- Carney advocated participative leadership: encouraging experts to contribute to the decision-making. This enables tasks to connect to the group that must own the decision. If group members can see how their own actions connect to a higher purposes of the organization, employees will have more skin in the game.

- For Carney, effective leadership is situational. The right person isn’t always there for the right time. Good leaders take stock of their followers.

Transactional versus Transformational Leaders:

Transactional leaders:

use rewards and punishments. This approach is most effective when the tasks are clear, repeatable and there is no ‘vision’ required.

Transformational leaders:

Achieve goals that both the leaders and followers are motivated to achieve as described by James MacGregor Burns (1918 – 2014). Bernard Bass (1925 – 2007) and Ronald Riggio build on Burns’ ideas with four components to transformational leadership:

- Transformational leaders support intellectual stimulation that not only challenging the status quo but ask colleagues to be creative;

- Transformation leaders support individualized consideration that keep communication open and feel free to share ideas, receive direct recognition for their contributions;

- Transformational leaders have and share a clear vision for fulfill their goals.

- Transformational leaders are a role-model that colleagues should emulate and support the leader’s ideals. They need to have EQ (popularized by Daniel Goleman) and IQ.

Carney talks about Machine Learning (ML) and Artificial Intelligence (ML). Machine Learning being useful for credit cards and anti-money laundering operations and many other applications and typically good if the future is expected to behave as the past (which includes the biases of the dataset). AI being “general purpose technology with widespread applications, whose productivity benefits depends on re-engineering processes to achieve a common purpose.” (349, Value(s)). For Carney, as well as University of Toronto scholars, AI is most useful as prediction machines that are better at modelling future events then any individual human might but it has many flaws. For example, hard to untangle how an AI model came to its conclusion on a particular circumstance which is not good for auditing purposes.

Leadership and the Crisis of Trust. Consent requires values-based leadership:

- The crisis of trust is a crisis of leadership.

- People have lost trust in experts.

- Trust has declined in the government and journalism.

- Shift of trust in family and friends over CEOs and bankers. EU was seen as a bureaucratic expert-led infrastructure…therefore, not to be trusted.

- The MMR vaccine was falsely linked to autism in the Lancet which contributed to a mumps epidemic in 2005 in the UK.

- Counterfactuals (which by definition do not happen) about preventable deaths during the COVID crisis, were taken as fact.

- Focus on building critical thinking skills is increasingly important. News is increasingly acquired through social media which is driven by what can keep the user most addicted to staying social media.

- Carney notes that Michael Gove went from the people ‘have had enough of experts’ to ‘follow the science’ as a minister in the Tory government.

Better trust = Better leadership. As Carney has stated several times now in this book that trust takes ages to build, moments to destroy and a long time to rebuild. Here is how it gets created:

1) Trust through Transparency:

Helps colleagues or citizens to see how and why a decision has been made. But Carney notes that transparency is an easy default with the risk of becoming white noise, or hard to understand with out a dictionary (academic language barriers creation) etc.

2) Trust through Factfulness:

Establishing the facts is critical as US Senator Moynihan famously said “You are entitled to your own opinion, you are not entitled to your own facts.” Fact checking is a new industry and distinguishing between marketing rhetoric and facts has also been hard to parse. Carney supports Facebook’s oversight board which is made up of Nobel laureate, constitutional law experts, a former prime minister of Denmark: And the board publishes the decisions, notably the media still interprets the decisions for clicks….

3) Trust through Acknowledging the Reality of Uncertainty:

Andre Gide famous saying “Trust those who seek the truth but doubt those who say they have found it.” Carney found it annoying that the Bank of England forecasts were being treated as facts by journalists even if it was explained that forecasts are cognitive exercises multiple times. The general public want certainty in their information, seek perfection, however the reality is that there is uncertainty, that scientists don’t actually have all the answers automatically and categorically on day one about COVID, for example. Carney advocated NOT professing false certainty but supporting a probabilistic approach such as the Bank of England’s MPC (Monetary Policy Committee). Carney believes that planning for Brexit was what established him as a solid leader: “we are prepared for this.”

4) Trust through Better Communication:

Carney believes in multiple layers of explanation as a critical tool at the Bank of England. They measure their communication with Flesch scores. Talking “jobs and prices” is more approachable for the general public than “inflation and employment”…too bad speaking clearly can remove the nuance. Value(s) the book would be much shorter but not as insightful, for example.

5) Trust through Staying in Your Lane:

Be comfortable delegating expertise, no all experts are leaders and follow your remit. With the Scottish referendum, Carney was obligated to provide some information regarding financial stability and fundamentals on the sovereignty question. Carney was very careful not to tread on the political side. The UK market expect Remain would win at 4/5th 80%, Leave 1/5th There are trade-offs in monetary policy particularly inflation controls that dampen employment. For Carney, it would have been political to not disclose that preparations were made for Brexit. There is merit in explaining limits to your expertise.

6) Trust through Listening to All Sides:

Even with all the facts laid out, there can be differences of opinion, of course. Engaging the wider community is key. As the chair of the FSB, Financial Stability Board, Carney was able to drive towards consensus even if there were competing views on where financial policy should be directed. He plans to provide that at the Glasgow Climate negotiations with 195 countries…

If you take the decision, people will love their best decisions and orphan their bad ones.

What Leaders Do:

- Finding the right people

- Setting the right priorities

- Catalyze action.

First, finding the right people:

Christine Lagarde told Carney that as the head of the IMF, there was diversity geographically but that they had all had PhDs in economics from MIT. Bank of England to overhaul their hiring policy. Remote working like Stripe. Developing the right leaders, manage those who have different backgrounds, rigorous people. Create a culture of open debate, wide range of leaders so that when you have to make major decisions like in early March 2008, where Carney met other central bankers at the top of Basel, Switzerland’s BIS Tower, he was read to support the President of the ECB, Jean-Claude Trichet in providing liquidity $200 Billion in liquidity to the market…

Second, setting the right priorities:

You need to look at global and technological developments. Ambition must be for our own self-esteem, we need to be ambitious and seek to solve clients biggest problems.

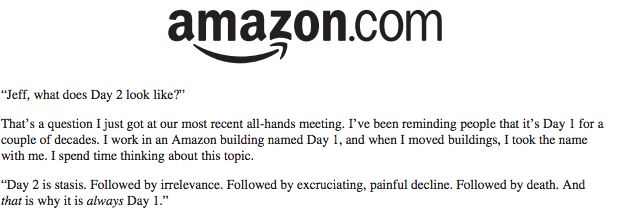

Third, catalyze action:

Amazon’s approach of building and feeding a flywheel makes sense. Keep up the momentum which allows the leaders to get out of the way. Amazon had a structured decision making: focus, how does Amazon make decisions.

Amazon Meeting Structure:

A) Defining the purpose of the meeting…is it to make a decision, to brainstorm or to be debriefed? Should include who has to be informed at the end of the meeting, try to be as inclusive as possible.

B) Ensure that everyone who needs to have read the memo before hand has read it and take the 15 minutes to read it at the start of the meeting if necessary.

C) The memo ought to be no longer than 6 pages. Simple is harder than complex in writing a six-page note. Tell a linear story in the memo, do not be repetitive.

D) If you are the decision-maker take clear decisions and ensure follow-up.

E) The BoE had a problem that they pushed this approach. They wanted to improve the communication and be more inclusive.

People want to be empowered and they were practicing leadership. So allow followers and leaders to not be mutually exclusive.

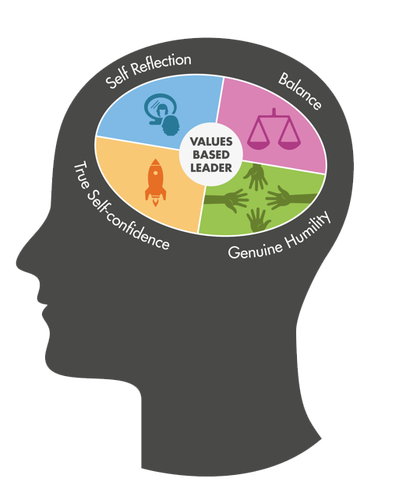

Attributes of Values-Based Leadership:

- Purpose: mission statements are helpful to bring on support. The Bank of England’s motto is “Promote the good of the people of the United Kingdom by maintaining monetary and financial stability.” The Bundesbank’s mission is “to protect the integrity of the Deutschmark.” Purpose is essential because it is strongly correlated with better performance. People want to work in a meaningful organization. You also need trust and integrity: if your stated purpose does not align with your actions then you will be in trouble as a leader. Leadership is “about acceptance of responsibility rather the assumption of power” (370, Value(s)).

- Perspective: be able to see the periphery, the poorest people’s perspective is a very important standpoint. Leaders think of the marginalized: a) during the 2008 financial crisis, working poor lost their savings, b) the climate crisis will hit the current generation of children and their grandchildren the hardest, c) COVID hit the elderly, vulnerable and essential workers most. During the financial crisis, there were concerns that allowing reckless behavior would ensure future reckless behavior. The moral question of Ben Bernanke: “do you let the man who smoked in his bed die to teach him a lesson, or do you save him and put out the fire that could have spread to his neighbours’ houses and then reprimand him?”

- Clarity: you need clarity of mind, meditation should be a daily activity for anyone who is serious about leadership according to Carney. You should seek to simplify the complicated. Speak with clarity as much as possible. Narratives / Story telling is the best way to means of connecting with audiences. Tim Geitner’s “Plan beats no plan” is coupled with Napolean “march towards the sound of gunfire.” Carney adds that “what beats a plan?…a plan that is well executed.” Macron’s zinger “make no mistake, there is no plan b because we do not have a planet b.”

- Competence: Carney put the premium on making the right call: good judgement. Strategy is important but execution is paramount. You need to be adaptive. Leaders have to know when to shut-up as well…Kennedy read The Guns of August by Barbara Tuchman which explains why European nations were too focused on supply chains leading to the First World War and used that insight to resolve the Cuban missile crisis.

- Humility: Mark Carney was the 118th governor of the Bank of England. Westminster Abbey has many historical figures, Chaucer, Newton, Darwin, Pitt the Younger, Clement Atlee. There are no central bankers and few capitalists buried at Westminster Abbey. There are no ‘economists’ except Sidney and Beatrice Webb of LSE fame. There will be many governors of the Bank of England after Carney is gone. Good leaders have an ability to learn, don’t turn to writing books. It’s important to admit that you don’t understand something. Carney was more interested in US dollar than the subprime mortgages. He didn’t imagine different possibilities. We should be building an anti-fragile system rather than trying to prevent all major financial crises. A growth attitude is essential.

- Key is to have purpose, perspective, clarity, competence. And humility.

- Humility and confidence are needed. Don’t be constantly humble.

- Real human progress is moral progress.

- Virtues grow with muscles.

Ed Brooks at Oxford also says moral leadership:

1. Humility: intellectual limits

2. Humanity: solidarity.

3. Hope: our ambitions for our future.

Analysis of Part 3: Chapter 13

- Artificial Intelligence and Machine Learning discussions are noteworthy for the fact that they are pretty lossy goosey. Carney seems to conflate the two concepts and there is a lot of evidence to suggest that AI and ML are misconstrued marketing concepts in practice with very focused use cases. And that AI has seen a surge in discussion because it is a counter-argument against the then US president who was attempting economic nationalism to re-trench labour jobs that “AI would be wiping out anyway.” Carney does not distinguish but should between General AI and Narrow AI.

- Carney spends very little time talking about how to quantify preferences and or when to lead and when to follow.

- If critical thinking skills are so important, then why is university so expensive? Why not train high schools kids for the SAT, LSAT and GMAT tests which require logical reasoning and math?

- Note that Carney points out Michael Gove’s about face regarding ‘following the science’ versus his rhetoric that the people ‘have had enough of experts’ (such as Mark Carney) in the campaign to leave the EU. First of all, follow the science has a spectrum of validity. Science is never truly settled on a topic because the pursuit of truth shows that theory can be over-turned. You can have scientists disagree vigorously precisely because there is no single scientific answer, but reasonably speaking IF the vast majority of scientists agree then it is de facto a law or settled science. Second of all, Carney shows his marketing short-comings, a catchy meme can travel far and wide, the people ‘ have had enough of experts’ was a marketing enticement to allocate votes to the Leave campaign when Carney was saying Brexit would have negative short-term financial effects.

- Carney believes in listening to the wider community, but you do see that he is less beholden to them.

- JFK questioned the advice of his team during the Cuban Missile Crisis…maybe because the Bay of Pigs was the most embarrassing military campaign ever.

Citations Worth Noting for Part 3: Chapter 13:

- Ajay Agrawal, Joshua Gans and Avi Goldfarb, ‘The Simple Economics of Machine Intelligence’, Harvard Business Review (November 2016).

- Philip V. Hodgson and Randall P. Whie, ‘Leadership, Learning, Ambiguity and Uncertainty and Their Significance to Dynamic Organizations’

- Max Weber, The Theory of Social and Economic Organization (New York: Oxford University Press, 1947).

- St Thomas University, ‘What is transactional leadership? Structure leads to results’, 25 November 2014.

- Daniel Goleman, Emotional Intelligence: Why It Can Matter More than IQ (London: Bloomsbury, 1996).

- Ronald E. Riggio, ‘Are You’re a Transformational Leader?’, Psychology Today, 24 March 2009.

- Mark Carney, Opening Statement to the House of Lords Economics Affairs Committee. 19 April 2016.

- Andre Gide, Ainsi soit-it ou Les jeux sont faits (Paris: Gallimard, 1952).

- John C. Maxwell, The 21 Irrefutable Laws of Leadership (Nashville: Thomas Nelson Publishers, 1998).