Chapter 11 The Climate Crisis

Key Takeaways

For 11,000 years, the stable Holocene era has afforded humanity the playground to thrive. Now we have created the Anthropocene which is driven by human impacts on the planet. Carney does not go into any counter-arguments to say that the impact of human activity on the planet is correlated 1% with climate change or 99%…for him the data is conclusive. In the 1850s, the Industrial Revolution drove up global temperature averages by 0.07 degrees Celsius per decade. The planet’s average temperature is up by 1 degree Celsius since the 19th century.

Other climate changes noted

- The oceans are 30% more acidic since the Industrial Revolution;

- Sea levels have risen 20 centimeters in the last 100 years;

- The 5th mass extinction has shifted to the 6th with extinctions at a rate that is a hundred times higher than an average from millions of years;

- There has been a 70% drop in mammals, fish, birds, amphibians and reptiles since 1965, assuming evolution is not at play, although how do you define evolution?;

Now, market prices of assets are being impacted. Climate change is likely creating:

- a. a feedback loop of rising sea levels,

- b. massive human migration away from rising coastal sea levels,

- c. extreme weather events that are damaging insured property,

- d. More impaired assets on the balance sheets of companies,

- e. A reduction work productivity with the lethal heatwaves,

- f. Global conflict over scares resources,

- g. collapse of coral reefs destroying the livelihood of 500 Million people and ¼ of all biodiversity,

- h. Increased regime change,

- i. Increased citizen unrest,

- j. Increased spread of disease

What is the cause?

Causes: Emissions

The UN’s Intergovernmental Panel on Climate Change (IPCC) has argued that there is a 95% chance that human activity is CAUSING the global warming / climate change. The release of GhGs (Greenhouse Gases) with the most problematic being CO2 which, during rapid industrialization and growth has meant that over 250 years, humans have burned ½ trillion tons of carbon. Trends suggest another ½ trillion could be released in the next 40 years…¾ of the warming impact of emissions is CO2, with the remainder being methane, nitrous oxide and fluorinated gases. Trees cannot carbon capture to rebalance. Temperature and CO2 emission move roughly together, therefore we know what the carbon budget ie. the amount of carbon dioxide that be released into the atmosphere before temperature thresholds are surpassed.

The planet as a system would accelerate into a dangerous feedback loop if average global temperatures go past 1.5 degrees Celsius. The IPCC predicts that if temperatures reach 2 degrees Celsius above pre-industrial levels then 1) sea levels could risk 10 centimeters, 2) ¼ of all people could experience severe heat waves, 3) coral reefs will die off almost completely… 4) permafrost could further unlock CO2 and methane accelerating the trends would blow the budget wide open.

Net Zero

Carney advocates a stabilization of temperatures at 1.5 degrees Celsius. above pre-industrial levels. To do that:

- Emissions have to fall by a minimum of 8 percent for the next 2 decades….

- We release about 42 +/- GigaTons of CO2 per year,

- Planetary budget is 420 GigaTons of CO2 remaining before we hit 1.5 degrees Celsius and 1500 GigaTons of CO2 before we hit 2 degrees Celsius..

Children born in 2021 will have to generate ⅛ the amount of CO2 emissions compared to baby boomers into order stay on carbon budget of 420 GigaTons of CO2 remaining before we hit 2 degrees Celcisu. We need to reduce excess carbon from:

- Industrial processes are 30%

- Buildings 18%

- Cars 17%

- Energy generation 17%

- Agriculture 10%

To reduce GhG, the solutions must

- Change how we create energy (fossil fuels must shift to renewables);

- Change energy usage (decarbonizing industrial processes, increased energy efficiency for buildings);

- Increase the carbon capture, use and storage (and maybe terra forming, although Carney doesn’t mention this)….

Basically, we need to convert the creation of all industrial process to electric and then shift the source of electric from fossil fuels to renewables. The first step may appear impossible considering the amount of energy needed to manufacturer most items in our homes, however that’s what has to happen. Bill Gates details the technologies needed in his book “How to Solve the Climate Crisis.”

Geography of Emissions

most pollution is from cities. By region its:

- China 28%,

- Asia – Other 16%

- USA 15%

- EU-28 10%

- India 7%,

- Russia 5%,

- Japan 4%,

- Europe – Other 3%,

- Africa 3%, Canada 2%, Australia 1%

The Consequence of Climate Change

How much do we value the future? The estimates of the costs of climate change and value of the sustainability contain many uncertainties that enable doubters. The GDP, employment and wage impacts are one way (a 25% reduction in GDP at the tipping point of 3 degree Celsius), the net present value of all future cashflows. What we really value such as the lives of species, livelihood adaptation, birth rate drop aren’t easily monetized.

How central bankers view climate change? There are two types of risk

- physical risks

- transition risks

Risk Type 1: Physical risks =

increased rate of climate and weather related events (storms, fires, floods). The underwriting risk shows that the entire livelihoods buckle as inflation adjusted losses have increased over 8x over the last few years.

- Insurers are in the front line of climate change, beach houses aren’t getting insured at the prices they were 10 years ago.

- The insurance sector is adjusting and pricing-in some climate change using various projected models, subject to re-writes like any other model…Carney feels that coupling “sophisticated forecasting, forward-looking capital regime and business models built around short-term coverage has left insurers relatively well placed to manage physical risks” (277, Value(s)).

- Carney argues that there areas of the economy that will need a public backstop because insurance companies will not insure those areas between $250 Billion and $500 Billion on the US coastal property by 2100.

- Insurers and reinsurers are expecting trouble, Lloyd’s of London has a 20cm assumption which coupled with a hurricane would cause Manhattan damage that is 30% more severe than Hurricane Sandy.

- Coastal flooding is projected to rise by 50% by the end of this century.

- Lethal heatwaves are projected to effect 1.2 billion people annually by 2050;

- The Network for Greening the Financial System (NGFS) is an 80 central bank strong group that have created representative scenarios to show climate risks may evolve affecting the real and financial economies:

- Hothouse earth shows that at 3 degrees Celsius, sea levels rise x cm and extreme weather events result in a 25% GDP loss by the end of the century.

Risk Type 2: Transitional Risk

The second category of costs of risk. The costs and opportunities are more apparent as the crsis worsens and impositions become more overarching:

There will be stranded assets

- Tropical deforestation of palm oil, soy, cattle and timber is for commercial use 70% of the time.

- Automotive industry that will, in Carney’s mind, be disrupted by electric vehicles, driverless vehicles and car-sharing services.

- Coal producers have gone bankrupt in the US.

- Demand and Supply Shocks: demand shocks affect consumption, investment, government spending and net exports in the GDP = C + I + G +(X – M). Demand shocks are short-term usually and therefore don’t effect the productivity of the economy. Supply shocks effect growth, the growth of labour supply, physical capital, human capital and natural capital and the degree of innovation in the economy. So the impact of climate change on GDP is very tough because the sample of prior shocks also contained policy adjustments …

Calculating the Impact of Climate Change on GDP

- Feedback loops amplify quickly and suddenly (ice melting off of the antartica rapidly) and the north pole, it’s dynamic and not inherently predictable even if there is no human variable in the atmosphere itself (all chemistry, geology and hard sciences):

- The relationship between GDP and temperature is not linear;

- Do physical climate events actually have a negative effect or simply impact growth (feedback loops and bad social impacts);

- The degree of adaptation and innovation to mitigate the impact of climate change could be much more significant (i.e humans turn a disaster into a strength leading to more prosperity due to new opportunities that are created).

- Factors like the mass climate refugees which could be over 200 million people, the poorest being dislocated.

- The 6th Mass Extinction: the biodiversity that provides natural capital from the Amazon to the coral reefs will be effected.

For Carney, it is a big deal that the CEO of Shell (Sir Mark Moody-Stuart) says that the probabilities of climate change’s negative impact on humanity is 75% and acknowledges that despite that uncertainty in predicting climate change, Moody-Stuart through the course of his career made larger strategic bets with much lower probabilities…

Causes Incentives

For Carney, climate change is a ‘tragedy of the horizon.’ The worst impacts are beyond the life-span of the decision-makers of today. The horizon is beyond: the business cycle, political cycle and central bank cycles.

- The horizon of central banks is 2 to 3 years.

- The horizon of financial stability is about 10 years.

- The horizon of political decision-making is about 4 years.

The benefits of mitigating greenhouse gases which stay in the atmosphere for centuries is massive, but for the people who don’t vote today, because they don’t exist yet. “Halving emissions over 30 years is easier than halving them in a decade.” (285, Value(s)) The welfare of future generations should not be discounted as heavily as the financial calculations typically demand.

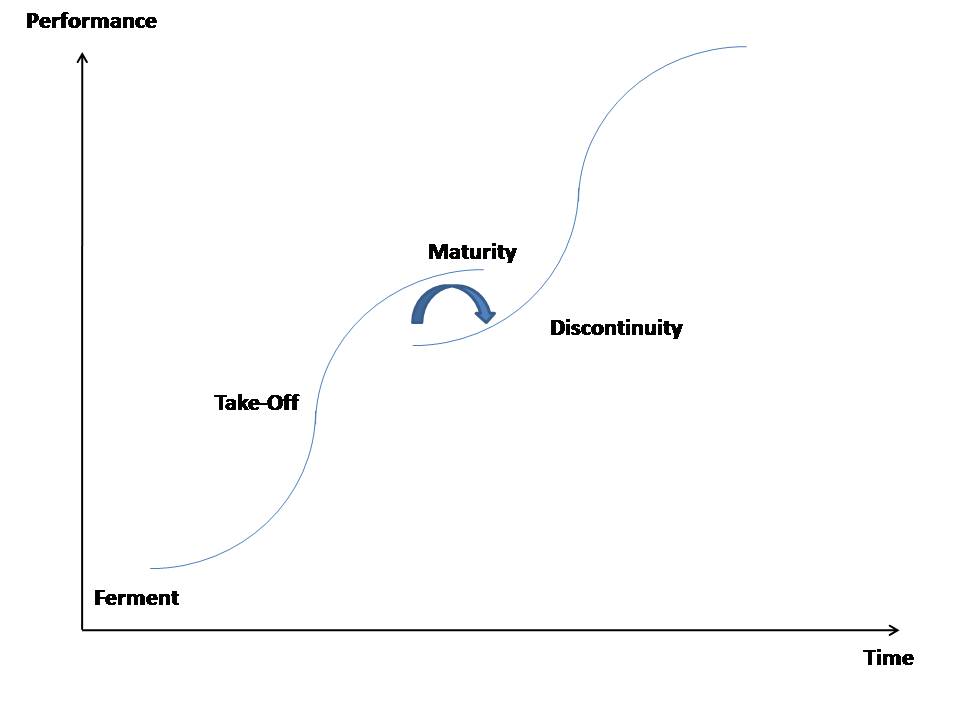

S-Curve:

The rate of adoption of new technology has three phases; 1) research and development, 2) mass adoption, 3) maturity. The rate of S-Curve over the years has been accelerating. James Watt who invested the stem and in 1769 did not see coal over take peatmoss until 120 years later in the 1900s (technically, Watt died before see that development). So, technology to tackle climate change is emerging at quicker paces. The S-Curve needs a nudge from the market as well as the public sources of capital investment.

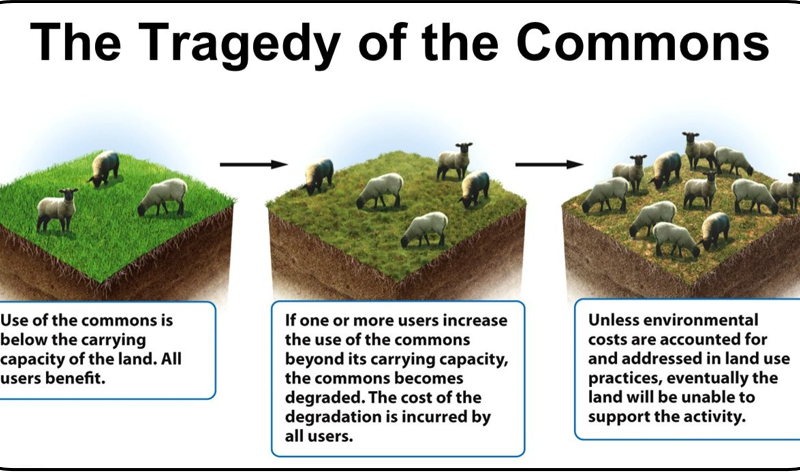

Tragedy of the Commons

The original example is the unregulated grazing rights on the common lands of Ireland and England in the 19th century there was a negative externality in which a decision is taken which then effects others who aren’t party or even benefit from that decision, is taken. We, the consumer, and we the producer don’t pay for the CO2 emitted to produce most goods. Other examples:

- 1) Overfishing to the point at which that stock of fish is depleted (Cod on East Coast of Canada);

- 2) Deforestation to the point where the forest is spoiled (Easter Island…);

- 3) Commons grazing to the point where the land was destroyed…

Three solutions to the Tragedy of the Commons:

- Pricing the externality: putting a price on carbon. This has only worked well in theory. There is a price of $15 per ton but you would need $50 to $100 per ton to meet the Paris Accord target…

- Privatization of the public spheres: Public grazing lands in the UK to privatization however this created a wealth transfer to those who had the right to charge a fee.

- Supply management by the community to cooperate or regulate the scarce resources there in. Popularized by Elinor Ostrom (1933 – 2012) as economic governance. Get political consensus with shared management.

Carney goes on to draw the analogy that COVID is like climate change, it is a global problem. But climate change has no boundaries at all. Now, there are echoes of Bretton Woods style nationalist self-interest, huge debts and new institutions to tackle climate change:

- 1992 – Rio Earth Summit; a good start..

- 1997 – COP (conference of the parties) 1 and 3 the Kyoto Protocol: Kyoto was flawed, didn’t have teeth, a more serious call to action;

- 2009 – COP15 the Copenhagen Accord flawed, advanced countries pledge financial flows to reduce emission in poorer countries;

- 2015 – COP21 the Paris Accord, more stakeholders, financial firms, turning the agreement into legislative objectives as the UK did (already a low emitter, but limited recycle programs and lots of trash in the streets)

Our political systems don’t overcome these items. True leaders are stewards of the system. Leadership is about being custodians.

Current Financial Sector

Financial markets aren’t really pricing in a carbon price transaction. There is a low urgency effort that will lead to hot house earth, according to Carney. Most financial energy numbers don’t use a price test for their carbon stress test of capital investment They usually use a static price. Their prices are well below the medium to get to zero. BP has $100 per ton in its internals. Only 4% of banks and insurers think these climate risks are being priced accurately. Only 16% used a dynamic price.

Transition Pathway Initiative (TPI) is a consortium of thirteen + five asset owners/managers that are trying to better understand the transition to low-carbon impacts investment strategies. They also launched the FTSE TPI (Climate Transition Index) to articulate who is on the right side of history in Carney’s mind. Investors are shifting capital away from hydrocarbon investments incrementally suggesting that they are pricing in a transition. In other words, the markets are responding to something akin to inevitability about a low-carbon economy. But these are strategic bets, it doesn’t mean they are certain. Moody’s “recently identified sixteen sectors with $3.7 trillion in debt with the greatest exposure to transition risk” (297, Value(s)).

- § For the Goldman Sachs, capital expenditure in oil and gas is being hindered by this transition of asset manager value in oil and gas. Major projects have been mitigated by 60% over the last five years, big oil is moving to big energy.

- § Portfolio managers are engaging and pulling down their oil and gas investment incrementally. Also, in part due to the collapse of prices.

- § Transition bonds. In the fullness of time, climate change will incentivize brown companies to raise capital for green innovation.

- § Carney argues we cannot diversify away from climate change.

- § For Carney he argues that we need financial markets to build a virtuous cycle, better pricing for investors and smoother transition.

- § Sustainable financial systems are being built and the next chapter discusses this in more detail.

Analysis of Part 2 Chapter 11:

- Sea level a big deal? Just how bad is this going over 2 degrees Celsius? It’s a prediction that seems likely and would result in actually cooking-up Earth, with accelerated feedback loop, to the point where the Antarctic ice sheet completely melts and we’d all have to learn to swim…We might even develop gills…..okay, that’s a stretch…how much of this is probable? The emotional crescendo of Al Gore’s An Inconvenient Truth was, in my view, showing major cities around the world being flooded by rising sea levels. This was the easiest and therefore, best way to illustrate the problem(s) which are myriad as Carney has tabulated in Chapter 11. But…..

- Sea level estimates are being re-evaluated: There is one issue with this description of coastal flooding…it is not so probable as once thought. Carney seems to have ignored the claim that water levels would rise 20 feet i.e. 6 meters for that reason….I wasn’t sure why his book doesn’t mention this often quoted climate catastrophe? He doesn’t address it. I mean, 6-meters-of-water! was probably the most obvious and emotionally powerful visualization as to why climate change should be a concern…. Well, it turns out that it is not as probable in the next 100 years as once thought. Read this page to get the down-low: https://en.wikipedia.org/wiki/Sea_level_rise. According to latest projections from the IPCC 6th Assessment Report (2021); the sea level is predicted to rise by 2 – 3 meters if global warming is limited to 1.5 degrees Celsius, 2 – 6 meters at 2 degree Celsius and 19 – 22 meters at 5 degrees Celsius and that’s over the next 2000 years…..Hmm…confused yet? 2000 years as in 4021?…yes….So by 2050, there “will” be 50 million people under the water line using 2010 populations as a benchmark….The prediction of mass migration (1/2 billion people) is slightly overstated….

- New research suggests that sea levels substantially lag Earth temperature changes, so the probability that sea level rising is a massive problem is much less the central / easy-to-understand threat of climate than originally thought.

- We don’t trust our audience to get a concept quickly enough therefore we skirt the concept: science is a process of contestation, not an absolute truth system. New information changes old scientific models. The mass migration narrative we thought 15 years ago is not quite the consensus view in 2021. Of course, scientific consensus can change with new research, why is that a problem? I’ve noticed that the default assumption is that the general public is incapable of understanding that nuance….and or the threat that an opponent will exploit “changing” scientific consensus to suggest “X is a hoax!”, X being whatever a partisan wants to discredit for the time being, is greater than the benefit of being honest with people. Carney talks about this with regard to Bank of Canada forecasts being both a ‘certainty’ and obviously ‘not a certainty’….

- Trust but verify | Calculate the sea level rise yourself: If you do your own calculation of the how much ice needs to melt off of land masses such as land glaciers on North America etc, Greenland and Antarctica, then doing so will help strengthen your understanding. In the case of the total ocean, there is an area of 361 million square kilometers that the new water would have to be evenly distributed on top of. There is 1.338 billion cubic kilometers of total water in the ocean that has to occupy 361 million square kilometers of Earth’s surface. The Antarctic Ice Sheet is 30 million cubic kilometers of ice, which could be added for a total of 1.368 billion kilometers. Depth = volume / length x width i.e. 30 million cubic kilometers / 361 million square kilometers is 0.083 km or 83 meters of additional water across the 361 sq km of ocean. Add 2.9 million cubic kilometers from Greenland and about 170,000 cubic km from mountain and other glacier formations…if you like but that would be a modest increase.

- 83 meters = 100% of Antarctica’s ice sheet has to melt: So take the 83 meter increase described above…that describes ALL the ice in the Antarctic melting which is more likely if human beings are idiotic (nuclear war, smog everywhere etc) or an extraterrestrial species from a Venus like home world invades and terra forms Earth to a warmer clime…. Even so, there is no where near enough ice on land to get to Waterworld levels, 83 meters = 272 feet….so don’t believe Hollywood, folks.

- Sense checking the 6 meters concept: So anyway, there are a bunch of assumptions that are required to get that original 6 meters prediction that Al Gore was shocking us with….And here is an example calculation. Basically, a small portion of Antarctic needs to melt for the 6 meter increase to occur, ie 83 meters = 100% therefore 6 meters = 13.8% of the ice sheet to drop into the ocean…but again, IPCC believes that 13.8% of 30 million cubic kms which is 4.14 million cubic kms will take a really long time to melt, the point is it will with our current policies but we’re also talking beyond 2100. So that’s assuming we do nothing which is obviously not the case. Humanity will reach a goal of carbon reduction because current companies will find a way to cost save and there are trillion dollar companies yet to be founded that charge a fee for solving climate change….probably.

- Bottom line on sea level right now: So if the IPCC report suggests that 1) ice melting will take a lot longer to have an effect than original thought, and 2) the planet has to warm by 5 degrees Celsius over a longer period of time, then the 6 meters isn’t probable (in our lifetimes or the lifetimes of most children born in the 2020s…). And by 2100, there will be multiple generations worrying about climate change so (gov’t & private) solutions will emerge ($$$$$$$).

- Magicians pivot your attention: So anyway, scientists don’t know for sure but it’s safe to say that the sea level story is no longer the central concern, hence Mark Carney does not lay into it at all in Value(s). Now, it seems plausible that he doesn’t discuss sea level much because he doesn’t want to admit that science is not static or that governor of central bank can’t accurately predict the future because then you won’t trust him or the institution to generally do what’s right… Instead of admitting the truth that science is a journey, in order to persuade us to make personal sacrifices, Carney and others have put more emphasis has been put on the fact that there will be more flooding as humans demand more single-dwelling homes in flood plains….which takes us back to the problem of personal preferences and how the consequences of those preferences are distributed.

- Smart money / market argument: Over the decade after An Inconvenient Truth (2006), most of the emphasis was on awareness coupled with government intervention. Stephane Dion in Canada led the Liberal Party to massive defeat in 2009, a campaign built on a Green Shift. Of course a myriad of variables determined that election which is why blaming the Green Shift is a political statement that Canadians “don’t really care about climate change” which obviously varies as an opinion per Canadian. Such is our complex voter preferences… However, the lesson taken there is that the idea that government and by extension the civil service and regulation are primary means of driving punitive costs to polluters has consistently been deemed suspect by a significant portion of smart-money folks.

- Obama was hands off for example because of the coalition he had backing him and the legislative strategy he needed to implement. And in his biography, his mother knew that jobs were more important then environment for poor Indonesians that she worked with for years. Now, financial institutions, which enable the allocation of scarce capital, in as optimal a manner as possible, are being marshalled (by the general investment customer base) to more seriously address climate change + the general investment. Carney does not put the most devastating case forward because it gets harder and harder to know how that would play out in a complex eco-system such as our planet. But basically, after the sea levels rise 10 cm….10 cm or 20cm? So what? We were talking about 20 feet in 2006. Some of the claim by Al Gore on ocean level has since been reevaluated (as mentioned above)….websites are disappearing that used to contain claims of 6 meter sea level rises “guarantee”. So he has to combine weather with flooding to say Hurricane Sandy would have been 30% worse than it was from an insurance perspective. I feel so bad for insurance companies having increase their rates….not!

- Reparations: Another point is that the Alberta conversation needs a better answer around some support system, although historically when a sector struggles we do not necessarily intervene, but with climate change, government is intervening to accelerate the transition. There are no easy answers there because living in minus 40 conditions in Edmonton becomes hard to fathom if the human capital with a green tech breakthrough can migrate to Silicon Valley with no dis-incentives.

- Another question is: what if the scientists are wrong, again? How much punishment should allocated to their grandchildren for the oil & gas careers that are hindered unjustly in this hypothetical? That would be absurd of course but the climate physics is rock solid until new research uncovers better techniques and models as part of the scientific method. It’s an important philosophical question: what is the consequence of getting it wrong? What commitment can Carney truly make if he is wrong? And if / when climate change is mitigated through a combination of human ingenuity and sacrifice, there will be naysayers who point of that it was never real in the first place because all the bad things that were suggested did not transpire! Such is the elephant in the room of all data science: there is not parallel version of Earth where we can control for different approaches to climate change.

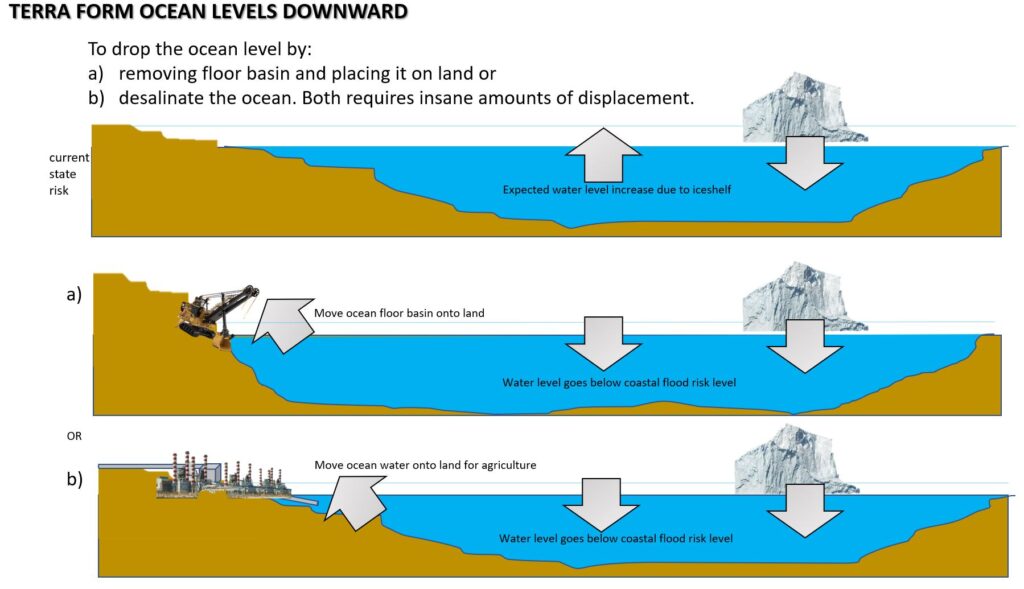

- The Yeah But…a lot of the public still can’t connect this slow moving crisis to their lives, most people see this is a transitionary problem over decades and decades, predictions have been wrong and continue to be wrong, if saving humanity was so lucrative then why haven’t we paid to terra form the planet to prevent sea level rising: there is a funding problem: no one wants to pick up the cheque, where is the global fund to pay for these changes, you are asking people to suffer for an abstraction that isn’t flawlessly defined…

- Carney fails to address the command economy advocacy imbedded in prescribing with science what every person’s carbon footprint ought to be. Here, there is no invisible hand, the government of the world is most equipped with providing each citizen with their responsibility. The counter by Carney is of course, seatbelts wouldn’t have been imposed without political and regulatory force. It is the use of that force that can spur innovation in concentrated points throughout the economy.

- Putting a price on pollution is like putting a price on negative social media comments, the state is imposing a costs for doing something that perceived as bad but has some positive value and making the recipient hopefully tougher for criticism of their instagram post of a really delicious meal.

- A general rule in life is to identify that if someone is claiming that there is a single cause to a problem, they are trying to convince you of something or sell you something. You are being persuaded into conformity of some kind, like you need to buy X to resolve the Y. A lot of people don’t actually like being talked down to…I’ve found…. The language problem of inexactness of human communication system (language) is slowly being overcome with PowerPoint, Film etc. This problem of debating cause versus correlation is best exemplified with climate change discussions. Human activity has caused climate change immediately sounds misleading because the “climate is always changing” and how does one know to what degree “human activity” is causing climate change. Humans could be contributing 1% or 99% of the factors driving climate change, but some goof will point out that volcano contribution to disrupt the argument. For example, the counter argument that human activity is not causing climate change conflates causing with contributing. If someone says human activity is not contributing to climate change then that’s a sniff test for an intellectual dilettante. To prove that humanity is contributing to changes in the environment simply apply the counterfactual of the no-humans version of Earth. In that version of Earth, on this day, you would now be outside rather than in your home or office where you are reading this article. There would be no roads, etc etc. The very fact that this is obvious, proves that humans impact Earth in a significant way. And secondly, all those human tools and technology that we have been using requires heat energy to produce. That heat energy generates CO2 amongst other gases. So if any one says that humans do not contribute to climate change, they necessarily have to deny that absent humans there would be roads, houses mysteriously populating this no-humans version of Earth. In other words, it’s absurd.

- Carney neglects to acknowledge that the research cited is subject to grants. If someone is obsessed with derivatives, then they will likely think derivatives are really important. They will have biases that warp their world to the point where their own brain notices patterns elsewhere that relate back to derivatives: this is selection bias. To not acknowledge that any human being, regardless of credentials is subject to the same confirmation and selection bias should they study climate change, is intellectually controlling. I suspect Carney knows there should be some doubt but he may not trust readers with this nuance.

- Another interesting sense from this chapter is that Carney doesn’t have an entrepreneurial spirit really, if he did he would understand that extinction is a necessarily part of evolution. If the cause is human habitat encroachments which by definition is going to continue to happen, then we should be sympathetic. However, extinction is not by definition bad. Does anyone miss Pan-American Airlines? Does anyone miss the Dodo Bird? Of course, we all miss these things or would like to see them in the wild but such is life…Dodo Birds were definitely eaten to extinction but they also did not produce enough offspring. Life is cruel and unfair.

- Measuring the acidity of the oceans: a 30% increase in acidity is significant if the acidity of the acid content is 1 -> 1.3 part per 100 but not if it is 1 0> 1.3 part per 1M….

- Carney does not mention that there is an increase in human habitats such that extreme weather events like flash flooding are on the rise…in geographies where the events are newsworthy. An analogy might be that coverage of gun violence is only newsworthy when a random citizen is the victim rather than a gang related victim.

- Carney does not address terra forming solutions accept for the socially accepted one: carbon capture which involves sucking carbon out of the air or releasing CO2 into the ground.

- Carney basically tells readers to read Bill Gate’s How to Avoid A Climate Disaster. In other words, friends help friends.

- Anyway, here are some of my wacky but fun ideas to address the most extreme consequences (such as the 6 meters ocean rise) which as I mentioned above is not that likely in the next 100 years:

- Notice how any terra forming suggestions are met with derision as they are not a complete solution, not costed and/or seemingly enable current practices? People forget that things do take a long time to implement. People also tend to want a single causal variable to solve all the underlying problems because our brains organized to address single cause circumstances…..there is rarely a single bullet, and change is incremental (we can’t cram for solutions). We tend to need a business case as well.

- If the 6 meters sea level rise is increasingly less likely, then we will continue to put off any wacky terra-forming ideas, and that’s less fun for me, but definitely not a major loss.

Citations Worth Noting for Part 2: Chapter 11:

- ‘What is Ocean Acidification’, PMEL Carbon Program.

- IPCC, Special Report: Global Warming of 1.5 degree Celsius (2018).

- Saul Griffith, Rewiring America, e-book (2020).

- Stockholm Environment Institute, ‘Framing stranded asset risks in an age of disruption’ (March 2018).

- Norman Myers, ‘Environmental Refugees: An Emergent Security Issue’, Oxford University (May 2005).

- Sandra Batten, ‘Climate Change and the Macro-Economy – A Critical Review’, Bank of England Staff Working Paper No. 706 (January 2018).

- IMF, ‘The Economics of Climate’ (December 2019).

- Ryan Avent, ‘Greed is good isn’t it?’, American Spirit, 18 April 2020.